KB Financial Q1 Earnings Announcement on 25th... Shinhan, Hana, Woori on 26th

4 Major Financial Holdings Pre-Recognize Hong Kong ELS Compensation... Shinhan's Net Profit Likely to Surpass KB

KB, Shinhan, Hana Show Positive Growth in 'Net Interest Income'

One-Time Factors Cause Major Financial Holdings' Profit Decline... Earnings Improvement Expected to Continue

The first-quarter earnings of major financial holding companies are expected to be mixed due to negative issues such as the large-scale loss incident involving Hong Kong H-Share Index (Hang Seng China Enterprises Index·HSCEI) equity-linked securities (ELS) and the real estate project financing (PF) crisis. Although the environment surrounding their core businesses was not unfavorable amid the continued high-interest-rate situation, various financial accidents and subsequent measures adversely affected their performance.

However, overall loan growth and net interest margin (NIM) have improved, maintaining a steady flow of net interest income, and since expense management such as workforce reduction and branch closures is proceeding as planned, experts analyze that concerns about earnings will not persist.

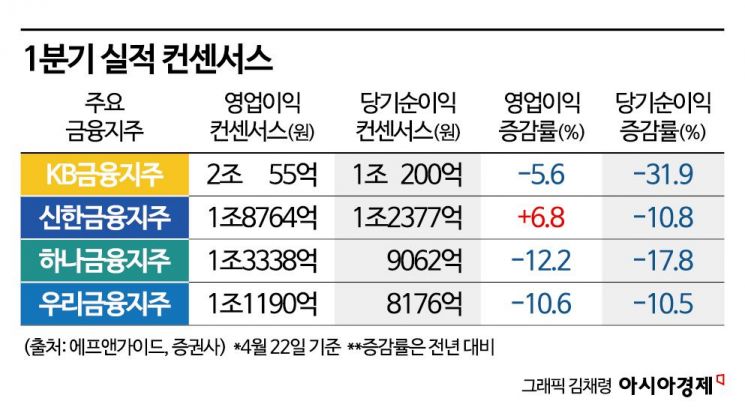

According to the financial sector on the 22nd, starting with KB Financial Group on the 25th, Shinhan Financial Group, Hana Financial Group, and Woori Financial Group will consecutively announce their first-quarter earnings for this year on the 26th. Although net income is expected to decrease due to provisions for voluntary compensation to subscribers confirmed to have losses from Hong Kong H-Share Index ELS and foreign exchange losses caused by the weak Korean won, operating profit is expected to remain solid.

Financial information analysis firm FnGuide estimated KB Financial's first-quarter operating profit consensus at 2.0055 trillion KRW, a 5.6% decrease compared to the same period last year. Net income was estimated at 1.02 trillion KRW, down 31.9%. The decline in net income reflects a preemptive recognition of approximately 900 billion KRW in ELS-related losses.

Market experts, however, analyzed that excluding the pre-recognition of ELS compensation, KB Financial is likely to achieve decent results. Junseop Jeong, a researcher at NH Investment & Securities, said, "NIM is expected to improve by 3 basis points (1bp=0.01%) compared to the previous quarter, and the loan growth rate is expected to rise by 0.8 percentage points," forecasting first-quarter net interest income of 3.38 trillion KRW, an increase of more than 21% year-on-year.

Shinhan Financial, which is highly likely to surpass KB Financial in first-quarter performance this year, has an estimated first-quarter operating profit consensus of 1.8764 trillion KRW, expected to increase by 6.8% year-on-year. The decrease rate in net income, which includes a pre-recognition of 350 billion KRW in ELS compensation, is estimated at -10.8%, less than KB Financial, with net income projected at 1.2377 trillion KRW. This means it surpasses KB Financial by 200 billion KRW in net income.

NH Investment & Securities also forecasted that Shinhan Financial's net interest income will increase by 8.7% year-on-year to 2.789 trillion KRW. This exceeds previous estimates and is attributed to a 1bp rise in NIM and a 2.3% increase in loans. Hanwha Investment & Securities projected fee income to increase by 21.2% year-on-year to 642 billion KRW.

Hana Financial is expected to have a relatively lower burden of Hong Kong ELS compensation compared to KB Financial, with a first-quarter net income consensus projected to decrease by 17.9% year-on-year to 906.2 billion KRW. Meanwhile, Woori Financial, which has the least burden with a total Hong Kong ELS sales volume of only about 44 billion KRW, has a net income consensus of 817.6 billion KRW, down 10.5%. Operating profit is estimated at 1.3338 trillion KRW for Hana Financial and 1.119 trillion KRW for Woori Financial, down 12.2% and 10.6% respectively compared to the same period last year.

NH Investment & Securities estimated Hana Financial's first-quarter net interest income at 2.507 trillion KRW, a 15.3% increase year-on-year, the second-largest growth after KB Financial. Woori Financial is expected to record net interest income of 2.189 trillion KRW, a decrease of 1.3%. Selling and administrative expenses are estimated to decrease from 103.7 billion KRW to 99.8 billion KRW for Woori Financial and from 110.8 billion KRW to 108.5 billion KRW for Hana Financial during the same period.

Kyungwan Eun, a research fellow at Shinhan Investment Corp., analyzed Hana Financial, saying, "It has relatively low ELS exposure and overhang risk," but noted, "The rise in the won-dollar exchange rate in the first quarter caused a foreign exchange translation loss of 70 billion KRW and a decline in the common equity tier 1 ratio by about 16 basis points, which are weaknesses." Ahae Jo, a researcher at Meritz Securities, evaluated, "Overall, banks' ordinary profits are expected to be at a good level," adding, "Bank loan growth rates continued with reduced pressure on household loan contraction and solid growth in corporate loans."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}