Financial Services Commission and Korea Accounting Standards Board to Establish ESG Disclosure Standards

Meeting Early Next Week... Final Approval by KSSB at End of April

US SEC Halts Introduction Amid Legal Dispute Issues

It is reported that the draft disclosure standards for Environmental, Social, and Governance (ESG), scheduled to be finalized at the end of April, are highly likely to include provisions applying the 'value chain (Scope 3)'. If Scope 3 is included, the regulations are expected to be stricter than the final U.S. version excluding it. Since financial authorities have emphasized interoperability with overseas countries such as the U.S. and Europe, attention is focused on whether recent moves to introduce climate disclosure sanctions in the U.S. will influence domestic policies. The business community voices concerns, asking for consideration of the realities faced by companies.

According to the business sector on the 18th, the KSSB (Korea Sustainability Standards Board) under the Korea Accounting Standards Board plans to hold a meeting early next week to discuss the draft ESG disclosure standards (sustainability disclosure standards). The draft will be finalized and established as a public draft after approval at the end of April. The public draft is expected to be announced in June in its final form after collecting stakeholders' opinions.

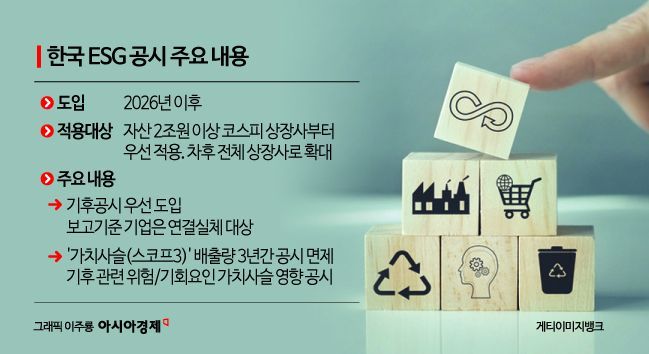

The Financial Services Commission (FSC) has been preparing related standards to enable comparison of ESG matters, which were previously voluntarily disclosed by companies, according to domestic disclosure standards. It is expected to be piloted from 2026 for KOSPI-listed companies with assets exceeding 2 trillion won. The plan is to prioritize the introduction of climate (E) disclosures, which have gained global consensus, over social (S) and governance (G) sectors.

Currently, it is estimated that the draft ESG disclosure standards are highly likely to include Scope 3 disclosures containing carbon emissions from partner companies. Until March, the inclusion of Scope 3 was strongly considered, but as concerns from the industrial sector grew, some internal opinions within the committee have emerged calling for reconsideration. Scope 3 disclosure expands the target beyond direct and indirect greenhouse gas emissions (Scope 1 and 2) to include the value chain (Scope 3). Scope 3 covers greenhouse gas emissions generated throughout the entire process, from supply chains, partners, transportation, product use, to disposal. Companies must also disclose the impact of climate-related risks and opportunities across the entire value chain. Although a three-year grace period was attached after implementation for Scope 3, the business community has raised concerns that further discussion is necessary.

This represents a stricter regulatory level than the U.S. adoption plan scheduled to take effect from January 2026. The U.S. Securities and Exchange Commission (SEC) excluded Scope 3 from the final 'Climate Disclosure Rule' adopted in March. Although Scope 3 was included in the 2022 draft, the SEC retreated following opposition from companies and Republican lawmakers citing difficulties in applying it to unlisted affiliates and the high cost burden. Global companies such as Microsoft (MS) and Samsung Electronics have independently established and are pursuing Scope 3 reduction plans.

Despite the U.S. final rule being more relaxed than the draft, it has become embroiled in legal disputes. The U.S. Chamber of Commerce, Texas Business Association, and 25 Republican-led states have filed lawsuits. Their objections include undermining the financial materiality standard for investors, increasing reporting burdens, and complicating annual and quarterly reports. Consequently, the SEC temporarily suspended the rule's application earlier this month. The U.S. Congress has also accelerated efforts to nullify the SEC's climate disclosure adoption. On the 17th (local time), THE HILL, a U.S. political media outlet, reported that Senator Joe Manchin, chairman of the Senate Energy and Natural Resources Committee, jointly introduced a resolution opposing the SEC climate disclosure rule with 32 Republican lawmakers.

Recently, division has also been detected within the European Union (EU), which plans to mandate climate disclosures including Scope 3 from the 2025 fiscal year. The EU's CSRD (Corporate Sustainability Reporting Directive) requires sustainability-related management information to be compiled this year and disclosed from next year. ESG disclosures will also be required from non-EU multinational companies with subsidiaries within the EU starting from the 2025 fiscal year. In February, the implementation plan for the Corporate Sustainability Due Diligence Directive (CSDDD), also known as the 'Supply Chain Due Diligence Act,' was rejected by the EU Council. Germany and Italy abstained, and France withdrew support demanding significant reductions. The CSDDD requires companies to conduct due diligence to understand and mitigate climate impacts.

It is expected that domestic financial authorities are also deeply considering these issues. In March, the Bank of Korea issued a report urging financial authorities to expedite the preparation of ESG disclosure standards. Kim Jae-yoon, head of the Sustainability Growth Office at the Bank of Korea, who authored the report on 'Trends in Domestic and International Climate Risk Disclosure Standards,' pointed out, "Financial authorities need to promptly establish and present climate risk disclosure standards that meet global regulatory levels so that domestic companies can smoothly respond to the strengthening of global climate risk disclosure regulations."

Kim So-young, vice chairman of the FSC, also expressed consensus at a field meeting in February, stating, "Unlike advanced countries such as the U.S. and Europe, South Korea has a high proportion of manufacturing, making carbon reduction structurally difficult," and "The unique characteristics of domestic industries need to be sufficiently reflected in the ESG disclosure standards formulation process." She added, "We plan to prepare domestic disclosure standards based on global disclosure standards interoperable with major countries such as the U.S. and EU."

A business community official said, "Although the plan is to first introduce it as an exchange disclosure with less legal burden on companies, there is no way to avoid the risk of lawsuits from shareholders based on the disclosed content in the future," and "Since concerns about corporate burdens and enormous costs have grown even in the U.S., careful consideration is needed when introducing regulations domestically."

A Korea Accounting Standards Board official explained, "The final decision by the KSSB is still pending this month, and the possibility of excluding Scope 3 is very high," adding, "Assuming Scope 3 is excluded, since the U.S. has applied much stricter standards in other regulations, it is not appropriate to say that Korea's ESG disclosure standards are stricter regulations than those of the U.S."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}