Samsung Electronics Q1 Preliminary Results

Sales Up 11%, Operating Profit Up 931%

Semiconductor Expected to Return to Profit After 5 Quarters

DRAM and NAND Price Increase... Effect of Rising HBM Demand

DS Division Operating Profit Forecasted at 3 Trillion in Q2

Galaxy S24 Captures US Market

February Sales Surge

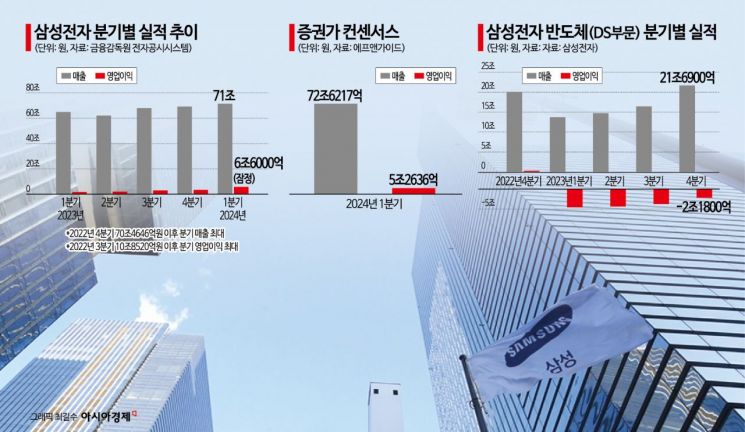

Samsung Electronics recorded an operating profit exceeding 6 trillion won in the first quarter of 2024. The semiconductor (DS) division, the company's core business, is highly likely to have returned to profitability for the first time in five quarters since the fourth quarter of 2022, resulting in an 'earnings surprise' that surpassed market expectations. Sales also recovered to the 70 trillion won level for the first time in five quarters since the fourth quarter of 2022.

On the 5th, Samsung Electronics announced through a public disclosure that its consolidated first-quarter sales reached 71 trillion won, with an operating profit of 6.6 trillion won (provisional). Compared to the same period last year, sales increased by 11.37%, and operating profit surged by 931.25%.

Samsung Electronics' operating profit significantly exceeded market forecasts. The consensus for Samsung Electronics' first quarter, provided by financial information provider FnGuide (the average of securities firms' forecasts), was sales of 72.6217 trillion won and operating profit of 5.2636 trillion won.

Analysts attribute Samsung Electronics' surprise earnings largely to the recovery in the DS division's performance.

The DS division was hit hard by the semiconductor downturn, posting a loss of 4.58 trillion won in the first quarter of last year alone, contributing to a total loss of about 15 trillion won in 2023.

However, this year, the reduction in memory production has steadily increased prices for DRAM and NAND, while sales of high-value-added products such as high-bandwidth memory (HBM), which has emerged as a key component in artificial intelligence (AI) semiconductors, have gained momentum, leading to business stabilization. Exports also increased, with semiconductor export value in March reaching $11.7 billion, the highest in 21 months since June 2022.

Although segment-specific results were not disclosed on the day, the securities industry estimates that the DS division's operating profit ranged from 700 billion to 1 trillion won, marking a return to profitability for the first time in five quarters since the fourth quarter of 2022 (270 billion won). Considering the surprise earnings that exceeded consensus, some analysts expect the semiconductor profit to be even larger.

Kyung Kye-hyun, President of Samsung Electronics' DS division, stated at last month's shareholders' meeting, "Since January this year, we have shifted from losses to a profit trend."

Besides semiconductors, the mobile division also contributed to the strong performance. Samsung Electronics launched the Galaxy S24 equipped with AI globally for the first time at the end of January, and sales have been strong. In February, Samsung's smartphone sales reached 19.69 million units, a 13% increase from the previous month, surpassing Apple (18%) to become the world's number one. At the announcement of its fourth-quarter results last year, the company stated, "We will lead the AI smartphone market with the Galaxy AI-equipped S24 series and foldables," and "Through this, we aim to grow annual flagship shipments by double digits and achieve smartphone sales growth exceeding market growth rates."

Samsung Electronics' smartphone sales growth in the U.S., Apple's stronghold, is particularly encouraging. In February, Samsung's market share in the U.S. rose to 36%, a 16 percentage point increase from the previous month. During the same period, Apple's U.S. market share dropped from 64% to 48%, a 16 percentage point decrease.

The video display (VD) and digital appliances (DA) divisions, which posted an operating loss of 50 billion won in the fourth quarter of last year, are also analyzed to have improved profitability compared to the previous quarter due to steady premium TV sales and aggressive sales of high-value-added home appliances.

Samsung Electronics' improving earnings trend is expected to continue for the time being. The upward trend in memory prices is anticipated to further enhance performance. According to TrendForce, DRAM average selling prices (ASP) are expected to rise by 3-8% in the second quarter, while NAND prices are forecasted to increase by 13-18%.

Supported by the expansion of generative AI services, shipments of graphics processing units (GPU) and neural processing units (NPU) are surging, leading to increased demand for HBM. Samsung Electronics plans to mass-produce the industry's first 5th generation HBM3E, stacking DRAM chips up to 12 layers, in the first half of this year, and aims to increase HBM shipments up to 2.9 times compared to last year.

The securities industry expects Samsung Electronics' operating profit in the second quarter to reach about 7.5 trillion won. The DS division's operating profit is anticipated to grow to the 3 trillion won range in the second quarter.

Kim Dong-won, Head of Research at KB Securities, said, "We expect the DS division's operating profit in the second quarter to increase about threefold from the first quarter to 3.3 trillion won," adding, "Especially, the recent earthquake in Taiwan on the 3rd, which disrupted production at U.S. Micron and Taiwan's TSMC, is expected to favorably affect Samsung Electronics' price negotiations for DRAM and foundry (semiconductor contract manufacturing) in the second quarter."

There is also a forecast that the foundry business will return to profitability in the fourth quarter due to increased orders and yield improvements. Shin Seok-hwan, a researcher at Daishin Securities, said, "Although the foundry business recorded a large loss last year, this year is expected to achieve maximum orders and return to profitability in the second half," adding, "With increased supply of HBM and demand for legacy (general-purpose) products in the second half, the pace of earnings growth is expected to be steeper than anticipated."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}