Last Year, Korean Foreign Currency Bond Issuance Reached a Record $56.4 Billion

Maturing Bonds at $40.5 Billion...Careful Monitoring of Funding Situation Needed

Last year, the issuance of Korean Paper foreign currency bonds reached an all-time high. Analysts attribute this to Korean bonds benefiting from reduced demand for Chinese bonds in the Asian bond market. There are also concerns that, with many bonds maturing this year, the funding situation needs to be closely monitored.

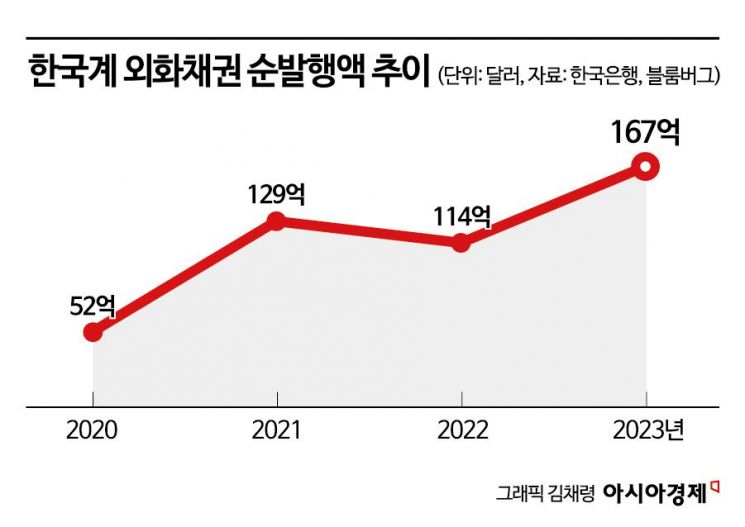

According to the Bank of Korea and Bloomberg on the 22nd, last year’s issuance of Korean Paper foreign currency bonds totaled $56.4 billion, marking a record high. The net issuance, calculated by subtracting redemptions from issuance, also reached a record $16.7 billion.

Foreign currency bonds are bonds issued overseas in foreign currencies such as US dollars and euros by residents in Korea to raise foreign currency funds. They serve as a major medium- to long-term foreign currency funding tool, helping improve the maturity structure of debt and increasing domestic foreign currency liquidity.

Despite a significant increase in issuance (supply) of Korean Paper foreign currency bonds last year, the bid-to-cover ratio more than doubled compared to the previous year, indicating strong popularity. This is analyzed as a reflection of reduced demand for Chinese foreign currency bonds due to China’s economic slowdown, which benefited Korean Paper bonds.

The Bank of Korea’s International Department explained, "Due to liquidity crises in Chinese real estate companies and other factors, demand for Chinese bonds has decreased. Some of this substitute demand appears to have flowed into Korean Paper foreign currency bonds, contributing to the strong issuance."

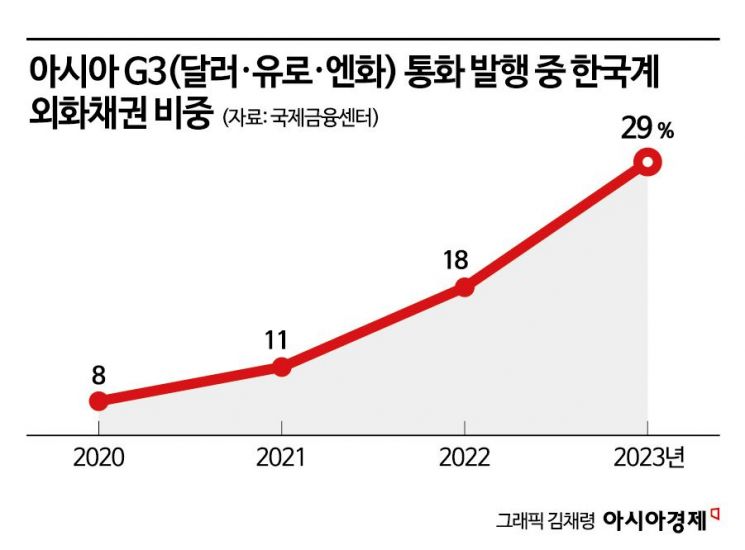

According to the International Finance Center, the share of Korean Paper bonds in G3 currency (dollar, euro, yen) denominated bond issuance by Asian countries increased from 8% in 2020 to 29% last year.

Corporate issuers led the issuance of Korean Paper foreign currency bonds. By issuer type, large corporations ($8.3 billion) and public enterprises ($6.8 billion) accounted for over 90% of last year’s net issuance of Korean Paper foreign currency bonds.

For private companies, issuance increased due to rising demand for overseas investment and operating funds. Last year, LG Energy Solution successfully completed a debut issuance of $1 billion in green bonds with 3- and 5-year maturities. GS Caltex and Doosan Enerbility each successfully refinanced $300 million of maturing bonds.

Public enterprises issued foreign currency bonds instead of won-denominated bonds to alleviate supply pressure in the domestic bond market. Meanwhile, banks’ net issuance ($2.9 billion) fell to about one-third of the 2022 level ($9.1 billion). The Bank of Korea analyzed that this was due to abundant foreign currency liquidity and limited demand for funds such as foreign currency loans.

The types of currencies used also diversified. In 2023, euro-denominated foreign currency bond issuance doubled to $6.2 billion compared to the previous year, and Swiss franc-denominated bond issuance increased from $800 million to $1.6 billion during the same period.

Foreign currency bonds also have drawbacks. While issuance increases external debt, worsening global financial conditions or rapid interest rate hikes can significantly increase repayment burdens for issuers, potentially posing latent risks to the domestic foreign exchange sector.

In particular, with $40.5 billion of maturities scheduled this year?exceeding last year’s level?close attention is warranted.

Ko Ji-sung, head of the Foreign Exchange Soundness Research Team at the Bank of Korea’s International Department, said, "Unlike banks with abundant liquidity, some companies may face sharply rising funding costs if issuance conditions deteriorate. In such cases, they may raise funds through won-denominated bond issuance or swap demand, which could impose supply and demand pressures on the domestic bond and foreign currency funding markets."

He added, "It is also important to note that a recovery in demand for Chinese foreign currency bonds and an increase in credit risk for domestic companies due to expanding domestic real estate project financing (PF) defaults could negatively affect market conditions."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}

{kind=link}