Mr. A was diagnosed with thyroid nodules at a hospital in January 2018. Since then, Mr. A has been regularly undergoing health check-ups and enrolled in a private insurance policy in February last year. However, the insurance company recently notified Mr. A of policy termination due to breach of the duty of disclosure, claiming that he failed to inform them about a re-examination related to thyroid nodules conducted in December 2022. Mr. A believed that routine health check-ups did not count as re-examinations related to the disease, but the insurer judged otherwise.

Going forward, regular examinations or follow-ups conducted while the condition persists will not be considered additional tests (re-examinations) and thus are excluded from the duty of disclosure at the time of insurance enrollment. However, failure to disclose diagnoses or suspected findings of diseases listed as disclosure obligations on the application form may constitute a breach of the duty of disclosure. The Financial Supervisory Service plans to promote this improvement by revising the 'Insurance Business Supervision Rules.'

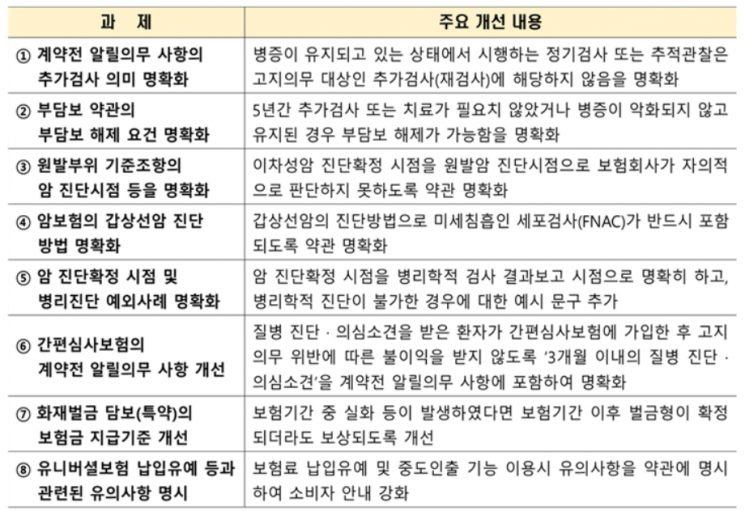

On the 2nd, the Financial Supervisory Service announced that it will improve eight insurance policy terms that are disadvantageous or difficult for consumers to understand, including the above.

The diagnostic methods for thyroid cancer in cancer insurance will also be clarified. Thyroid cancer diagnosis can be made through Fine Needle Aspiration Biopsy (FNAB) and Fine Needle Aspiration Cytology (FNAC), but some policies currently specify only FNAB as a diagnostic method. Going forward, policies will be improved to mandatorily include FNAC as a diagnostic method for thyroid cancer.

The timing of cancer diagnosis confirmation and exceptions to pathological diagnosis will also be specified. Currently, in cancer insurance, the timing of confirmed cancer diagnosis is judged based on the pathological test result report according to court precedents. In cases where pathological diagnosis is impossible due to the insured’s death or serious risk of life or physical function impairment, cancer diagnosis may be recognized without pathological testing. However, policies lacked clear explanations, making it difficult for consumers to understand. Going forward, policies will clearly define the timing of confirmed cancer diagnosis and add example clauses for exceptional cases where pathological diagnosis is impossible.

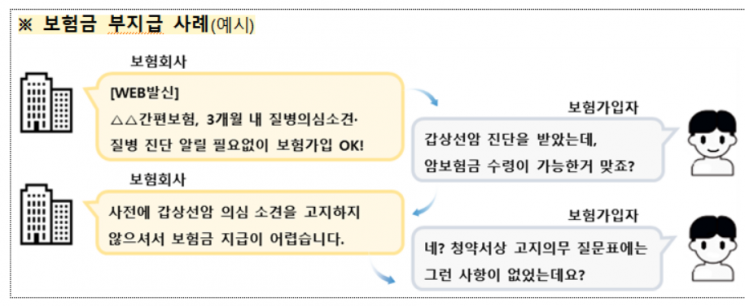

The pre-contract disclosure obligations for simplified underwriting insurance will also be improved. In some simplified underwriting insurance policies, 'diagnosis or suspected findings of disease within 3 months' are excluded from disclosure obligations, allowing patients diagnosed or suspected of disease to enroll. However, there have been many cases where insurance contracts were canceled or claims denied because the diagnosis or suspected findings were not disclosed at the time of claim. Going forward, ‘diagnosis or suspected findings of disease within 3 months’ will be mandatorily included in the disclosure obligations for simplified underwriting insurance.

The payment criteria for fire fine coverage (rider) will also be improved. Currently, the payment condition for this insurance is limited to 'cases where a fine is confirmed during the insurance period.' Because of this, even if a fire occurs during the insurance period, insurance payments were sometimes denied on the grounds that the fine was not yet confirmed. Going forward, if a fire occurs during the insurance period, payments will be made even if the fine is confirmed after the insurance period, by improving the payment criteria.

Additionally, the conditions for lifting exclusions in policies with exclusions will be clarified, and consumer precautions regarding premium payment deferrals and partial withdrawals in universal insurance will be explicitly stated in the policy terms. These improvements aim to reduce consumer misunderstandings and potential disputes related to insurance policy terms.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}