MSCI Financial Sector PBR Lags Behind China, Severely Undervalued

Sharp Decline in Securities Firms' Earnings This Year Due to High Interest Rates and Real Estate PF Defaults Concerns

Securing New Growth Engines Through Expansion of Digital Asset Management and Retirement Pension Markets

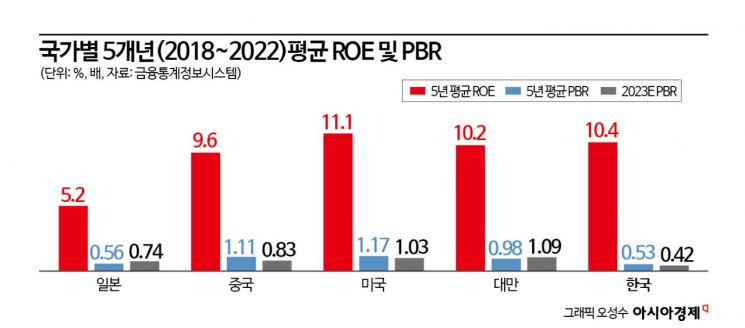

#1. The price-to-book ratio (PBR) of the Morgan Stanley Capital International (MSCI) financial sector has never fallen below 1.0 in the past decade. However, in the Asian financial sector, excluding Taiwan, South Korea, Japan, and China all recorded PBRs below 1.0. Narrowing the scope to the top investment banks (IBs) by country based on Bloomberg league tables, the 12-month forward PBR for 2023 is 1.0 for the U.S., 1.1 for Taiwan, 0.8 for China, 0.7 for Japan, and 0.4 for South Korea.

#2. According to FnGuide, there are no domestic securities firms expected to achieve operating profits exceeding 1 trillion KRW this year. Following Mirae Asset Securities, which opened the era of 1 trillion KRW operating profit in 2020, the '1 trillion club' expanded in 2021 to include Mirae Asset Securities, Samsung Securities, NH Investment & Securities, Korea Investment & Securities, and Kiwoom Securities. Last year, Meritz Securities was the only firm to reach the 1 trillion KRW mark. This year, none are expected to do so.

Bottoming PBR Despite Increases in Assets and Capital

The current position of the domestic securities industry compared to overseas markets is at the 'bottom.' For comprehensive financial investment business operators (CFIBOs) with equity capital exceeding 3 trillion KRW, assets and capital increased by 5.6 times and 2.8 times respectively in 2022 compared to 2007, and net income on a separate basis tripled. Over the past decade, average annual growth rates were 11.3% for assets and 9.5% for capital. Net income also recorded an average annual growth rate of 24.2% over the last 10 years. Especially after COVID-19, liquidity expansion and increased trading volume caused net income to surge, with CFIBOs recording approximately 6.4 trillion KRW in net income in 2021, a 56% increase from the previous year. Despite the annual growth in assets (11.3%), capital (9.5%), and net income (24.2%) over the past decade, the PBR has hit new lows.

Moreover, last year, due to the base effect from the previous year's performance, increased market volatility, and unprecedented interest rate hikes, earnings plummeted. Net income was about half of that in 2021, returning to the 2019 pre-COVID-19 level. This year remains challenging. Rapid interest rate hikes and resulting bond valuation losses, deteriorating investor sentiment leading to decreased trading volume, contraction of the real estate project financing (PF) market, and large-scale provisioning make performance deterioration inevitable.

As a result, no securities firms are expected to join the '1 trillion club' this year. Meritz Securities, which was the only firm to achieve 1 trillion KRW in operating profit last year, is projected to record 780.5 billion KRW this year, with anticipated impacts in the real estate PF sector.

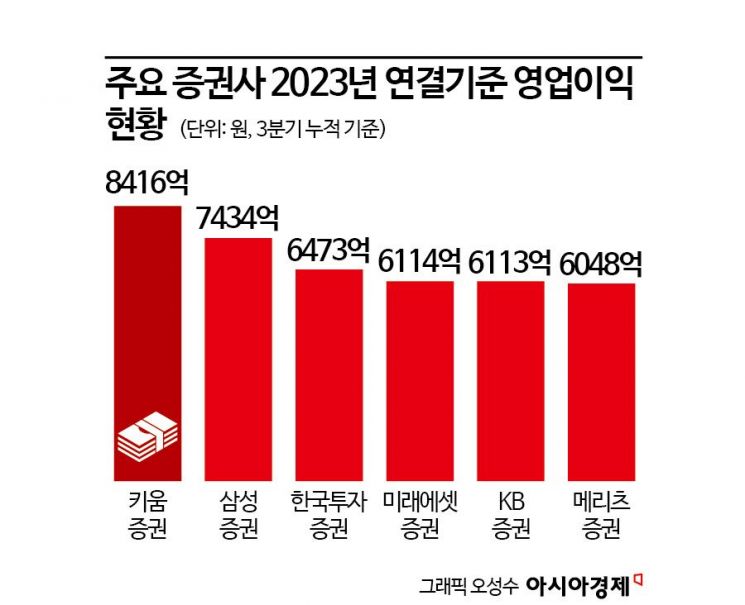

Mirae Asset Securities, which opened the era of 1 trillion KRW operating profit in the domestic securities industry, is expected to remain at 778.9 billion KRW this year. Kiwoom Securities had accumulated operating profits of 841.6 billion KRW through the third quarter, making entry into the 1 trillion club likely, but due to a large-scale bad debt from the Yeongpoong Paper lower limit price incident, a loss of around 400 billion KRW is unavoidable, and the annual operating profit is expected to be about 668.8 billion KRW. Samsung Securities, expected to have the highest operating profit this year, is projected to record 902.9 billion KRW.

High-Interest Rate Environment Eases, Overseas Business Expansion

However, the dominant outlook is that the industry will bottom out this year and resume growth. Kim Jae-cheol, a researcher at Kiwoom Securities, said, "Although the high-interest rate trend negatively affecting securities industry performance will continue into next year, there is a possibility of interest rate cuts after the first half of next year, which will reduce the factors that caused performance deterioration," adding, "Based on the changed business structure after COVID-19, performance improvement is possible."

Increased trading volume is also expected to drive performance improvement. Considering that expectations of interest rate cuts are already priced into investor sentiment, experts believe the timing of trading volume recovery will accelerate. This is a factor that can boost retail segment performance and improve IB business segment results. Researcher Kim Jae-cheol noted, "Large-scale provisions have been made to manage the loss risks currently emerging in the securities industry, indicating meaningful risk management," and added, "We believe the securities industry has passed the bottom since last year."

Accordingly, a revaluation of the domestic securities industry is worth anticipating. There is room for upward adjustment from the current PBR level due to diversification of revenue structure, improved profit stability in key business segments, and growing overseas business.

Another positive factor is the high return on equity (ROE) compared to overseas companies. The domestic securities industry, which has recorded the largest ROE growth rate among investment banks by country and maintains an average double-digit ROE, is not only hitting record lows in PBR but also remains at the lowest PBR level compared to other countries. Even in 2021, when the highest performance and ROE were recorded, the PBR was the same as in 2020 and was evaluated lower than other countries.

Diversification of Revenue Structure... Is Sustainable Growth in Securities Industry Possible?

For domestic securities firms to escape undervaluation, sustainable growth is essential. To achieve this, it is necessary to increase the proportion of the asset management segment, which has relatively low profit volatility. The asset management segment of domestic CFIBOs recorded 814 billion KRW in earnings last year, with an average annual growth rate of only 2.7% over five years. Its revenue share was also low at 7.4% in 2022 compared to other business segments. This contrasts with major global investment banks like JP Morgan and Morgan Stanley, where asset management revenue accounts for 22.1%.

However, it is noteworthy that domestic securities firms are enhancing earnings stability based on reduced reliance on brokerage commissions and increased interest income compared to the past. Researcher Kim Jae-cheol stated, "Domestic securities firms are diversifying their revenue structures, and the growth outlook for the asset management segment is bright, so the market value of the domestic securities industry has ample room to follow the PBR level of the Japanese securities industry."

Since COVID-19, there has been a rapid shift to non-face-to-face services, the emergence of new high-net-worth individuals, and increased importance of the retirement pension market due to aging, all driving increased demand for asset management. In particular, the digital asset management market through financial platforms is expanding. The asset management segment can play a role in creating new revenue sources from the platform perspective, such as asset succession, real estate, and virtual assets.

The retirement pension market is also a future growth area. As of the first half of this year, retirement pension reserves reached 346 trillion KRW, a 16.7% (50 trillion KRW) increase from the previous year. Although the size of retirement pensions is larger in banks (179 trillion KRW) and insurance (87 trillion KRW) than in securities (79 trillion KRW), the growth rate of reserves compared to the same period last year is steeper in securities (22.0%) than in banks (14.1%) and insurance (11.7%). With the implementation of the default option system this year, there is also a 'retirement pension money move' movement within the financial sector. A representative from the Korea Financial Investment Association explained, "After product yield disclosures, the core competitiveness will be yield," adding, "Among the top 10 products with the highest default option yields (6 months) in the second quarter of this year, seven are securities firm products."

However, growth in the IB segment is expected to be slow. Hana Financial Management Research Institute forecasts, "The securities industry is expected to recover mainly through brokerage commissions due to improved investor sentiment from interest rate cuts and corporate earnings improvement expectations, but the IB segment is unlikely to see profitability improvement due to delayed real estate market recovery despite increased corporate direct financing demand."

Therefore, advice has emerged to approach with caution from a short-term trading perspective. Park Hye-jin, a researcher at Daishin Securities, explained, "The securities industry should lower earnings expectations for the fourth quarter due to concerns about overseas real estate-related defaults and increased interest rate volatility, and the negative impact may continue into the first quarter of next year," adding that trading is possible only for stocks with a large retail proportion.

Korea Ratings also expects an unfavorable environment for the securities industry due to interest rate volatility and real estate finance uncertainties. Kim Ye-il, senior analyst at Korea Ratings, said, "The main factors for securities firms' performance decline are interest rate hikes, deteriorated asset management performance, reduced IB segment fee income, valuation losses in alternative investments, and provisioning for real estate PF," expressing concern that "Although defaults have not occurred immediately due to bridge loan maturity extensions, if the real estate PF market shifts to selective maturity extensions and restructuring, defaults may surface."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}

{kind=link}

{kind=link}