Fitch "Non-Performing Auto Loan Delinquency Rate 6.11%"

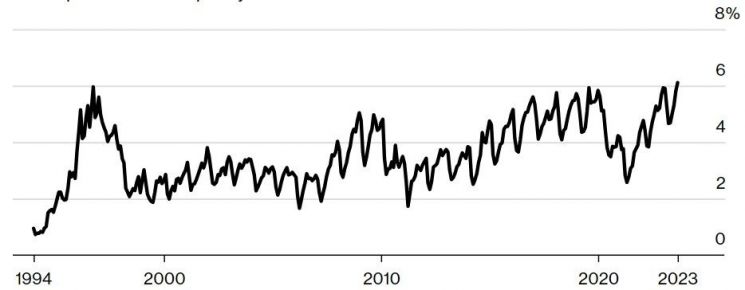

Highest Since 1994

High Interest Rates and Inflation Increase Loan Repayment Burden

As interest rates soar, more Americans are unable to repay their auto loan installments. Despite the Federal Reserve's (Fed) aggressive tightening, the economy continues to show solid growth with strong employment and consumer spending, but the difficulties faced by ordinary people are intensifying, analysts say.

According to global credit rating agency Fitch on the 23rd, the delinquency rate on subprime auto loans in the U.S. that are over 60 days past due reached 6.11% in September this year. This is the highest level in 29 years since 1994.

As interest rates have surged, the number of borrowers struggling to repay principal and interest has increased. According to financial information firm Bankrate, for borrowers with the lowest credit scores, auto loan interest rates are 14.18% for new cars and 21.38% for used cars. This is 9 percentage points and 14 percentage points higher, respectively, compared to rates applied to borrowers with the highest credit scores (5.07% for new cars, 7.09% for used cars). With inflation significantly increasing living expenses and interest rates rising sharply, borrowers’ interest burdens have grown.

Due to "carflation" (vehicle price inflation), both new and used car prices have reached record highs, increasing the amount borrowers must repay. Additionally, the suspension of student loan repayments ended at the end of August, which analysts say has contributed to the rise in auto loan delinquencies.

Josephine Korvacioli, a 28-year-old living in Denver, is struggling to repay her auto loan due to rising interest rates. With a credit score of 580, she took out a loan at a 13.58% interest rate to purchase a 2019 Honda truck. She now pays $700 monthly for auto loan principal and interest plus insurance costs. However, earning $17.50 per hour working at Costco, she finds it difficult to cover her car payments, rent, and over $20,000 in credit card debt, and now faces the risk of vehicle repossession. According to Cox Automotive, the number of repossessed vehicles due to loan defaults is expected to rise from 1.2 million last year to 1.5 million this year.

Bloomberg reported, "Many vehicle owners are struggling with unstable employment markets and persistently high inflation, leading to loan delinquencies," adding, "With the Fed signaling a prolonged period of high interest rates, this problem is likely to continue."

Margaret Lowey Peery, Senior Director of Asset-Backed Securities (ABS), said, "Pressure on subprime borrowers is intensifying," and "They are likely to be the first to show the negative effects of macroeconomic headwinds."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}

{kind=link}