K-Battery and Equipment Also Cross Borders

Battery Companies' Overseas Investments Benefit National Interests

Equipment Localization Rate Around 90%

Top 3 Battery Companies to Invest 100 Trillion KRW in Facilities

30-40% or More of This Investment in Equipment

NCM Battery Market Lead Effect

Strengthened Equipment Ecosystem

Overseas Battery Makers Also Say "We Will Buy Korean Equipment"

"Equipment on overseas production lines? They are all domestically made."

When asked about the localization rate of equipment at local factories, most domestic battery industry officials, who are currently busy building overseas factories, respond that the equipment is mostly domestic. It is taken for granted that the equipment is domestic. In other words, when battery factories are established overseas, Korean equipment is exported abroad. This creates a twofold effect of selling both batteries and equipment. On the other hand, the localization rate of semiconductor equipment, which has represented Korea for decades, is below 30%. When building semiconductor factories overseas, equipment must be purchased from the Netherlands, Japan, and the United States. This means that overseas battery factories contribute more to the Korean economy than overseas semiconductor production lines.

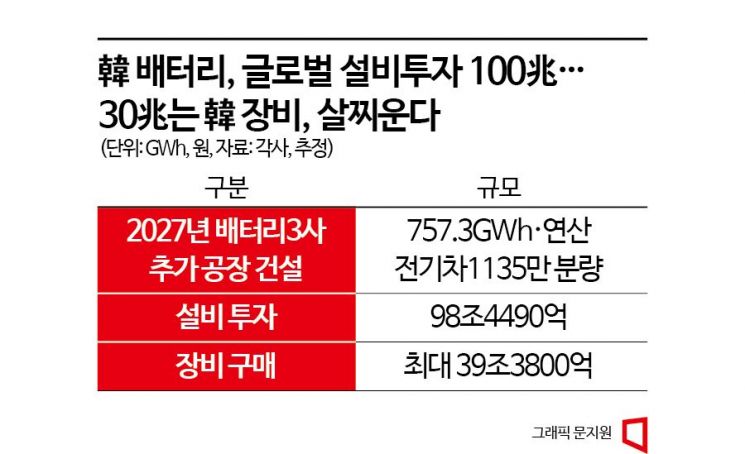

The strength of the Korean battery industry lies in the ‘materials, parts, and equipment (SoBuJang) ecosystem.’ Among materials, parts, and equipment, the localization rate of equipment, which had the least attention, is around 90%. Along with ‘K Battery,’ the equipment industry is also crossing the ocean. The scale of capital expenditure (CAPEX) for factories to be built by the three domestic battery companies?LG Energy Solution, SK On, and Samsung SDI?by 2027 is close to 100 trillion won. Of this, about 40 trillion won will be invested in equipment. The ‘order intake’ for our equipment companies will continue to overflow. Foreign companies building battery factories are also showing interest in Korean equipment. It is evaluated that the early market dominance by the three battery companies and the growth of the SoBuJang ecosystem are now bearing fruit.

The global factory capacity planned by the three domestic battery companies by 2027 is 1,109.3 GWh (gigawatt-hours) annually. Excluding currently operating factories, the additional factory capacity to be built by 2027 amounts to 757.3 GWh. Assuming an average capital expenditure of 130 billion won per 1 GWh, the total CAPEX is approximately 98.449 trillion won, nearing 100 trillion won. More than 30-40% of the CAPEX goes into equipment purchases.

In terms of amount, this is about 29.53 trillion to 39.38 trillion won. The proportion of equipment investment within CAPEX increases as the factory size grows. Construction costs decrease with economies of scale, making large-scale construction cheaper, whereas equipment costs increase proportionally with scale. Especially in the U.S., where many large-scale factories over 30 GWh are being built, the equipment proportion is expected to be higher than in China, Hungary, or Poland.

Most of this equipment is domestically produced. SK On stated that the localization rate of equipment in new battery factories exceeds 95%. LG Energy Solution reported at the ‘K Battery Development Strategy Conference’ held in July 2021 at the Cheongju Ochang plant in Chungbuk that the localization rate of equipment over the past three years (2018?2020) was about 87%. Samsung SDI announced an equipment localization rate of 95%. As equipment orders begin in earnest, especially centered on North America where explosive growth is expected from 2025, a favorable wind is blowing not only for core materials like cathode materials but also for the equipment industry.

The situation is different for another advanced industry, semiconductors. The localization rate is around 20%. The semiconductor equipment localization rate refers to the proportion of equipment supplied to domestic semiconductor companies that is produced domestically by domestic companies. Among domestic equipment imports, 77.5% depend on three countries: the U.S., Japan, and the Netherlands. The domestic sales of the ‘world’s top five semiconductor equipment companies’?Applied Materials (U.S.), ASML (Netherlands), Lam Research (U.S.), Tokyo Electron (Japan), and KLA (U.S.)?amounted to $20.3 billion (about 25.9637 trillion won), accounting for 81.3% of the market share (data from Korea International Trade Association’s International Trade and Commerce Research Institute).

The high localization rate of battery equipment is because the three domestic battery companies secured the market early. Although lithium-ion batteries, which currently dominate, originated in Japan, large-scale mass production was first started by domestic battery companies. Since the 1990s, they began mass-producing small batteries used in laptops and mobile phones. Thanks to this, the equipment ecosystem also became robust. It was possible because there were continuous nearby demand sources such as Samsung Electronics, LG Electronics, and Hyundai Motor Company. The scale has grown even larger with the advent of the electric vehicle era.

Battery equipment companies, which have developed their technology through large-scale supply, are expanding not only domestically but also overseas. It is hard to find companies outside Korea that have a track record of supplying large-scale equipment to overseas factories mass-producing high-nickel batteries represented by NCM (nickel-cobalt-manganese). Some Chinese companies have experience supplying overseas factories, but the U.S. and Western countries are excluding Chinese companies from their supply chains. Due to this ‘China exclusion’ policy, domestic equipment companies are expected to enjoy a windfall. Last year, the U.S. Department of Commerce announced the Unverified List (UVL) of export-controlled companies, including 33 Chinese firms; among them was Haimusing, a supplier of assembly process equipment to CATL.

Domestic battery equipment companies supply products not only to the three Korean battery companies but also to European and U.S. battery cell manufacturers. Equipment demand from European companies aiming for battery mass production after 2026 is increasing, raising the possibility of additional orders. Companies such as Hana Technology, SFA, and Top Material have formed equipment consortia to supply domestic battery equipment to Northvolt, Envision AESC, Freyr, and ACC. As everyone rushes into battery mass production, Korean equipment companies with technological prowess and large-scale order achievements are celebrating. There is no rule that a company like the Dutch ASML, which dominates the semiconductor industry, cannot emerge from Korea.

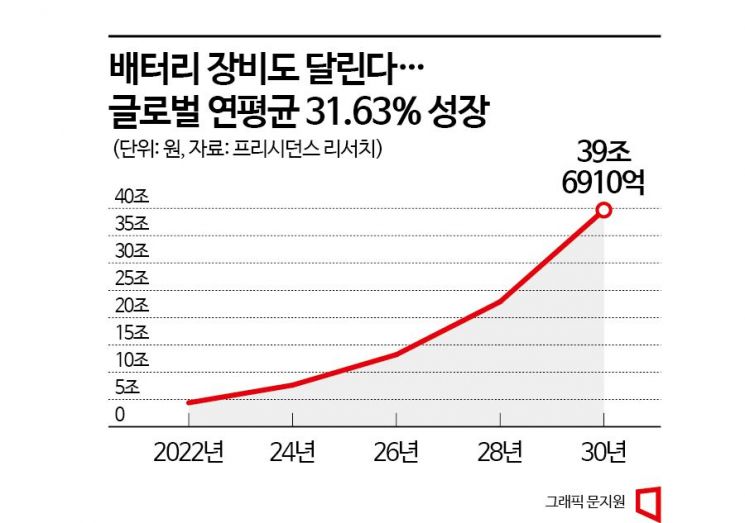

However, battery equipment technology is evaluated to need further advancement in areas such as cost reduction. The global battery equipment market is expected to grow from 7.6319 trillion won this year at an average annual rate of over 31%, reaching 39.691 trillion won by 2030 (data from market research firm Precedence Research).

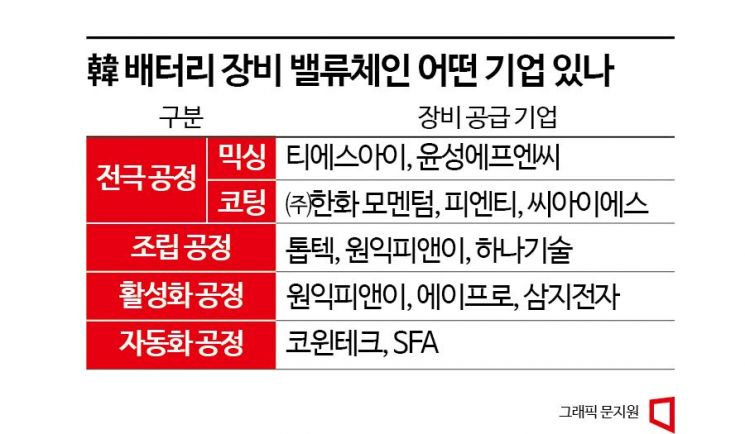

The battery process is broadly divided into four stages: electrode → assembly → activation (formation) → inspection. Our equipment companies have developed equipment tailored to each detailed battery process, such as mixing, pressing, cutting, and aging.

First, the electrode process is the manufacturing process that produces the cathode and anode, the most basic components of a battery. Process equipment that improves performance and manufacturing efficiency is required. Depending on the product type and form factor (classification by shape), the first step is the mixing process, where measured active materials (materials that generate electrical energy), conductive agents (materials that facilitate electron movement), and binders (materials that help bonding and coating) are mixed. Equipment from companies such as TSI, Yoonsung FNC, and Jeil M&S is used in the mixing process. Then, the electrode is thinly coated with copper foil and aluminum foil and dried, called the coating process. Hanwha Momentum, CIS, and PNT are companies that manufacture coating equipment.

Next, the electrode passes between two large rolls to be flattened. This removes unnecessary spaces between particles and increases energy density. Roll pressing equipment from CIS and PNT is used in this process. After flattening, the electrode is cut horizontally according to size (slitting) and then cut vertically (notching), completing the electrode process.

The completed electrode then undergoes assembly according to the form factor, such as pouch, prismatic, or cylindrical. The cathode, anode, and separator are stacked (stacking), folded (folding), or wound (winding) layer by layer, placed into a pouch or aluminum can, and electrolyte is injected. This process completes the battery form. Toptec, Wonik PNE, and Hana Technology manufacture assembly process equipment.

Activation is the process of embedding battery characteristics. In this process, the battery is charged and discharged and ‘aged’ to activate it. Aging is a process where the battery is stored for a set time at a specified temperature and humidity to sufficiently disperse the electrolyte inside the battery and optimize ion movement. Equipment from Wonik PNE, APRO, and Samji Electronics is used. Afterward, inspection equipment checks for defective cells, and packaging is done before the battery is released to the market.

The equipment investment ratio by battery process is generally about 30% for the electrode process, 17% for assembly, 29% for activation, and 24% for inspection and automation. Based on sales (2022), companies such as SFA (secondary battery division, 542.9 billion won), Wonik PNE (288.8 billion won), Phil Energy (189.7 billion won), and CIS (157.2 billion won) rank high among battery equipment companies. Equipment orders from battery companies start about one to one and a half years before factory completion. It is evaluated that the time when battery equipment orders for many U.S. factories completing in 2025 will surge is approaching.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}

{kind=link}

{kind=link}