Chinese Battery Companies CATL and BYD Surpass Half of Global Market Share

Korea's Three Companies Hold 23% Amid Large Supply Contracts and Joint Factories

Current Market Share Reflects Factory Expansion Trends from 3-4 Years Ago

Korean Battery Plants Centered in North America to Complete in 2 Years

High Possibility of Reversal in Global Market Share Trends

The global market share of Chinese battery companies is soaring. China now accounts for more than half of the global market. The combined shipment volume of the three major Korean battery companies is less than half of theirs. Korean batteries, which had been thriving by leading with ternary batteries known for their high technical barriers, may be losing ground to Chinese batteries. The truth will come to light in two years.

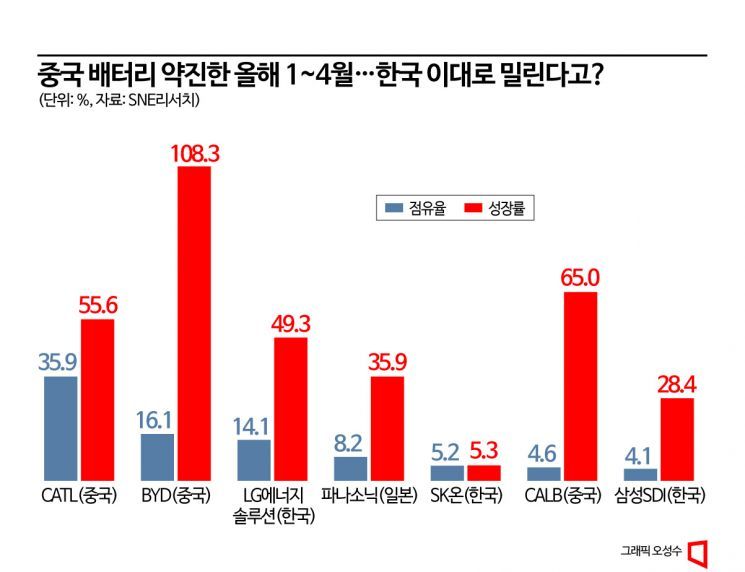

CATL (China) ranked first in electric vehicle battery usage from January to April this year. Its market share was 35.9%. The combined market share with BYD (China, 16.1%), the global second-largest company, is about 52%. Meanwhile, the combined market share of the three domestic battery companies?LG Energy Solution, SK On (a battery subsidiary of SK Innovation), and Samsung SDI?is 23.4%. The combined market share of Chinese battery companies is more than twice that of the three Korean companies. Compared to the same period last year, the market share of the three Korean companies decreased by 2.8 percentage points (SNE Research data).

Korean batteries seemed to be on a solid path recently, securing large-scale supply contracts with global automakers and establishing joint ventures over the past 2-3 years. However, their global market share, which was around 50% in 2020, has halved to the 23% range. This change is largely due to the staggered timing of factory expansions between Korean and Chinese battery companies.

The strength of Chinese batteries lies in the domestic market. The electric vehicle penetration rate in first-tier cities such as Beijing, Shanghai, Guangzhou, and Shenzhen has now reached 40%. China classifies cities from first to fifth tier based on population, housing prices, and development level. Since 2009, China has implemented the 'New Energy Vehicle Subsidy Policy.' Leveraging massive subsidies, it built an electric vehicle ecosystem. From the mid to late 2010s, local governments also began providing electric vehicle subsidies, rapidly increasing battery factory expansions. This was several years ahead of Europe and the United States. Thanks to this, Chinese battery companies have recorded triple-digit growth rates in recent years.

However, the market share gap between Korea and China is expected to narrow going forward. The current market share reflects the factory expansion trends from 3-4 years ago. It typically takes 3-4 years from confirming factory expansion to completion and full operation. Korean battery companies have been engaging in a series of joint ventures with North American automakers since 2021. Of the 11 battery factories planned by the US 'Big 3' automakers (GM, Ford, Stellantis) by 2026, nine will be built with the three Korean battery companies. Korean battery firms are collaborating not only with North American automakers but also with Hyundai Motor (Korea) and Honda (Japan).

The battery factory capacity to be completed by next year and 2025 will reach 463GWh, including LG Energy Solution's 280GWh, SK On's 164GWh, and Samsung SDI's 23GWh. Considering that the current North American production capacity of the three Korean battery companies is 26.5GWh, production capacity will increase by 1647% within two years.

Moreover, Chinese battery companies, which have only produced batteries domestically, are likely to face difficulties in establishing overseas production bases. Most of the production bases of Chinese battery companies are located within China. They are concentrated along the eastern coast, including Ningde in Fujian Province, where CATL's headquarters is located, as well as Jiangsu and Guangdong provinces. For example, CATL's production capacity last year was 318GWh, of which 14GWh was produced in Germany, and the rest was produced domestically (Samsung Securities estimate).

In the future, Chinese companies plan to expand factories mainly in Europe and Asia. Following its German factory, CATL plans to build a second European factory in Hungary with a capacity of 100GWh. It is also discussing joint factory construction with Ford and Tesla in North America. However, due to the Inflation Reduction Act (IRA), which effectively restricts advanced industry entry into countries of concern, they are facing difficulties in building local factories. BYD is constructing a battery factory in Thailand with a target operation of 100,000 electric vehicles next year and is preparing a joint factory in Uzbekistan.

Professor Lee Hogun of the Department of Automotive Engineering at Daeduk University said, "It is true that the Chinese electric vehicle market grew first, but its growth potential may be limited compared to other countries. Since the subsidy benefits for domestic battery manufacturers ended at the end of last year, their influence is expected to decrease. We need to closely monitor the market share trends after this year."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}

{kind=link}

{kind=link}