Rising Yields on US Treasury Bonds Maturing This Year

Lower Than Corporate Bond Rates of MS and Johnson & Johnson

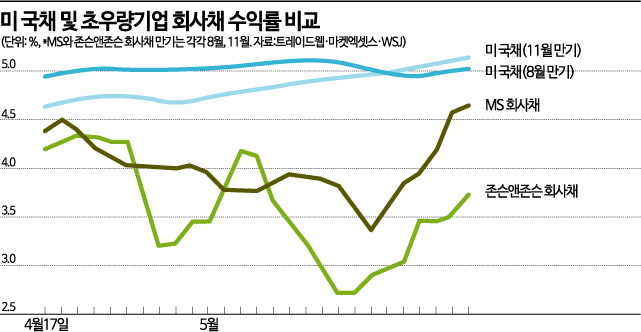

As negotiations over the U.S. debt ceiling reach an impasse, raising the likelihood of a default, investor sentiment toward U.S. Treasury bonds has weakened. The surge in U.S. Treasury yields has even led to an 'inverted yield curve' phenomenon, where Treasury yields exceed those of high-grade corporate bonds.

According to the Wall Street Journal (WSJ) on the 23rd (local time), U.S. Treasury bonds maturing in August are currently trading at a yield of 4.99%, while those maturing in November yield 5.12%. These levels are higher than the yields on corporate bonds issued by major U.S. companies. For example, Microsoft (MS) corporate bonds maturing in August yield 4.64%, and Johnson & Johnson corporate bonds maturing in November yield 3.73%. Compared to U.S. Treasuries maturing at the same time, these are 0.35 percentage points and 1.39 percentage points lower, respectively.

U.S. Treasuries typically trade at yields lower than those of 'Triple-A (AAA)' rated corporate bonds, which are considered ultra-safe. This is because the risk of default on government-issued bonds is virtually zero. As a result, investors such as governments and institutions flock to these bonds even without high yields.

However, the recent rise in yields on U.S. Treasuries maturing within the year above corporate bond yields suggests that unless Treasuries offer returns exceeding those of corporate bonds, they may not be absorbed by the bond market. For instance, the yield on U.S. Treasuries maturing on the 6th of next month has soared to an all-time high of over 6%. Moreover, the yield spread between junk bonds, which are considered non-investment grade, and U.S. Treasuries has narrowed from over 8 percentage points to about 5 percentage points.

Investors generally believe the possibility of a U.S. government default is low. However, as the 'X-day'?the day when the government's available budget runs out?approaches on the 1st of next month, the White House and the Republican Party have yet to reach an agreement on the debt ceiling. This has led investors to start preparing for the worst-case scenario. Matt Brill, head of U.S. investment-grade credit trading at asset management firm Invesco, said, "Our question is whether the borrower has the ability and willingness to repay the debt on time. The U.S. government has the ability but it is unclear if it has the willingness. Investors think it could go either way." Blake Gwinn, head of interest rate strategy at RBC Capital Markets, stated, "If the debt ceiling is breached, the Treasury can prioritize government spending to avoid default on principal and interest payments. Even if a default occurs, payment delays are likely to last only a few days."

As the default deadline approaches, U.S. companies are rushing to issue corporate bonds in preparation for potential financial market instability. According to financial data provider Dealogic, U.S. investment-grade companies have issued $112 billion (approximately 148 trillion won) in corporate bonds as of May. This is three times the issuance amount from last month and significantly higher than the $46 billion (approximately 61 trillion won) issued a year ago. Except for 2020, when ultra-low interest rates due to the COVID-19 pandemic led to $196 billion (approximately 259 trillion won) in bond issuance, this is the highest issuance volume in the past seven years. The increase reflects a proactive effort to raise funds amid spreading financial market uncertainty and the looming possibility of an economic recession, which could rapidly cool the corporate bond market and increase funding costs.

The WSJ reported, "(International credit rating agencies) Moody's and Fitch still assign the highest credit rating to the U.S., but they have noted that the brinkmanship over the debt ceiling between the White House and Republicans could potentially have a negative impact on credit. Traders concerned about a potential U.S. default are shifting from U.S. Treasuries to top-rated corporate bonds as a safe haven."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}