SM Stock Price Surges After HYBE Tender Offer

On Alert for Kakao's Possible Tender Offer Participation

[Asia Economy Reporter Yuri Choi] Whether Kakao will participate in the public tender offer for SM Entertainment (SM) has become an unprecedented point of interest. SM's stock price has already surpassed the tender offer price of 120,000 KRW proposed by HYBE, increasing the likelihood of failure. Although Kakao maintains that there is "no decision made" regarding the tender offer possibility, the market interprets this as a sign of potential participation.

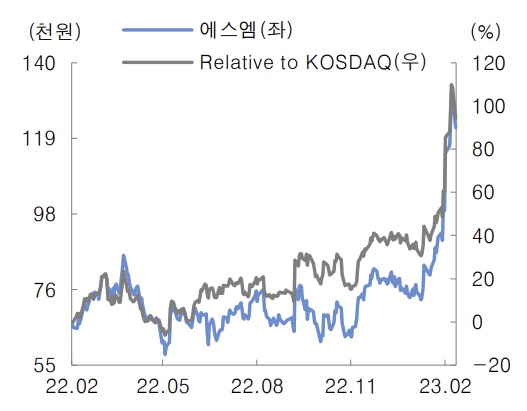

On the 20th, SM's stock price recorded 121,800 KRW. Despite a sharp 6.38% drop from the previous trading day after HYBE firmly stated it would not raise the tender offer price, the price remains above the 120,000 KRW mark. Since HYBE entered the SM acquisition battle on the 9th, the stock price has risen nearly 24%. On the 16th, it even hit a 52-week high of 133,600 KRW.

The market views HYBE's tender offer as effectively failed. HYBE had pledged to purchase up to 25% of shares from general shareholders at 120,000 KRW per share by the 1st of next month, but the stock price has exceeded that. If HYBE fails in the tender offer, Kakao will have an opportunity to acquire SM. Although the outcome of the provisional injunction filed by former SM Chief Producer Lee Soo-man to prohibit the issuance of new shares and convertible bonds is a variable, at least the path for additional share acquisition opens.

As HYBE stated, raising the tender offer price is also difficult. HYBE plans to invest about 700 billion KRW in the tender offer. Additionally, it has signed a contract to acquire 14.8% of shares from former Chief Producer Lee for 422.8 billion KRW. HYBE intends to borrow 320 billion KRW short-term from affiliates to fund this. As of the third quarter, the company’s cash and cash equivalents stood at 903 billion KRW, so there is no immediate difficulty in acquiring shares, but raising the tender offer price would be burdensome.

Park Sung-guk, a researcher at Kyobo Securities, pointed out, "Typically, bids concentrate on the last day of a tender offer, so we need to watch closely, but it is unlikely to reach the target quantity of 25%. If the tender offer price is raised above 140,000 KRW, the required funds could increase to 900 billion KRW, risking the 'winner's curse.'"

Kakao has more financial flexibility compared to HYBE. First, its affiliate Kakao Entertainment will receive 890 billion KRW on the 24th from the Saudi Arabian Public Investment Fund (PIF) and others as part of an investment. Although the investment funds are said to be split evenly between operating funds and acquisitions of other companies, they can all be used for acquiring SM. This is because the funding purpose includes a clause stating it "may vary according to the company's business strategy."

Adding to this, Kakao Piccoma, a webtoon platform affiliate, has secured 560 billion KRW from overseas sovereign wealth funds such as Anchor Equity Partners, totaling 1.46 trillion KRW in secured funds. Furthermore, Kakao holds 1.24 trillion KRW in cash and cash equivalents.

Kim Jin-gu, a researcher at Kiwoom Securities, stated, "If Kakao aims to acquire a combined 43.4% stake, including the largest shareholder's shares and tender offer shares, the maximum price it can offer is 141,000 KRW per share." This means Kakao Entertainment and Kakao Piccoma's combined funds of 1.46 trillion KRW alone can propose a price above 140,000 KRW per share.

Kakao distances itself from the possibility of a tender offer for SM. Although there have been talks about selecting an underwriter to review various M&A options including a tender offer, the official stance remains that "nothing has been decided."

However, the market interprets even this as implying the possibility of a tender offer. It is seen as cautious behavior before the provisional injunction lawsuit results are announced, but with an intention to proceed with a tender offer. If the court judges that SM is in a management rights dispute, Kakao cannot secure the 9.05% stake in SM. If Kakao confronts HYBE and former Chief Producer Lee through a tender offer, it would create a management rights dispute itself. This is why it is believed Kakao will only conduct behind-the-scenes work until the lawsuit results are out.

A securities industry official said, "Due to the provisional injunction lawsuit, they cannot make an official statement, but they are not denying it either," adding, "It is interpreted as keeping the possibility open to prevent HYBE's tender offer success."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}