First Announcement After CPI Benchmark Change on the 14th

Decline Expected to Slow... Month-on-Month Increase Anticipated

[Asia Economy Reporter Hwang Yoon-joo] Amid growing optimism in the stock market, the KOSPI has been faltering since February. It has been hesitating to break through the 2500 mark. The direction of the KOSPI, which is taking a breather, is expected to largely depend on how the U.S. Consumer Price Index (CPI) will be released on the 14th (local time).

According to the Korea Exchange, the KOSPI index in February rose only 0.8%, from 2449.80 to 2469.73. This contrasts sharply with the 8.9% increase in January (2225.67 → 2425.08).

The KOSPI’s hesitation this month is largely due to diminished expectations for interest rate cuts. Both the U.S. January employment data (nonfarm payrolls) and the Institute for Supply Management (ISM) services index significantly exceeded expectations, weakening the outlook that the interest rate hike cycle would end in the first half of the year. Earlier, the U.S. nonfarm payrolls increased by 517,000, shocking the market. This figure is about three times the expected 187,000 and close to 1.5 times the previous month’s 260,000.

According to FedWatch, the probability of a rate hold at the March Federal Open Market Committee (FOMC) meeting has dropped to 0%. Instead, the market is betting on a rate hike. The probability of a 25bp (1bp=0.01 percentage point) rate increase surged to 90.8%, and the probability of a 50bp hike rose from 0% to 9.2%.

The probability of a rate hike at the May FOMC meeting has also changed. The outlook for a rate hold dropped from 58.9% to 18.4%. Conversely, the probability of a 25bp hike jumped significantly from 30% to 74.2%. Initially, the expectation was that after a 25bp rate hike at the March FOMC, the market would enter a rate hold phase, but this has shifted to a 50bp rate hike by May.

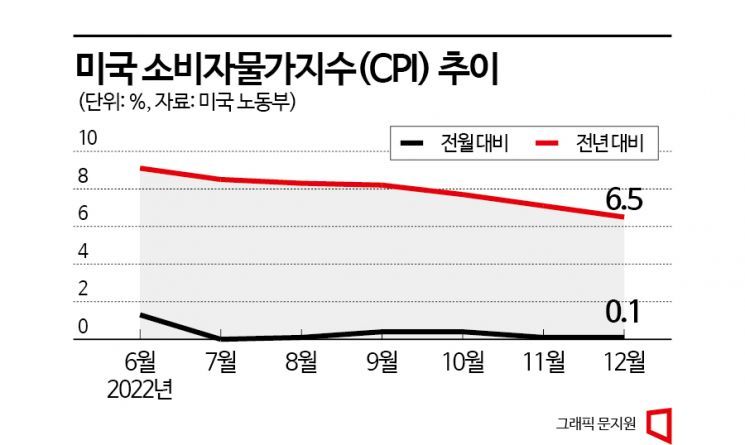

Meanwhile, the U.S. CPI to be released on the 14th (local time) is expected to be a turning point. This CPI release is the first since the benchmark was revised. Moon Hong-chul, a researcher at DS Investment & Securities, explained, "There have been changes in the weighting of items due to changes in consumer behavior over recent years," adding, "The revised CPI is expected to show reduced volatility, and the recent downward trend will appear exaggerated." He explained, "This is because the new CPI benchmark increased the weight of housing costs and lowered that of automobiles."

According to Bloomberg consensus, the January CPI and core CPI are expected to record 6.2% and 5.5% year-on-year, respectively. This is lower than December’s figures (CPI 6.5%, core CPI 5.7%), marking the fourth consecutive month of declining inflation, although the pace of decline is expected to slow significantly.

Most notably, the month-on-month CPI and core CPI are expected to rise by 0.5% and 0.4%, respectively. Market experts anticipate that the January CPI month-on-month increase could reach its highest level since June 2022, significantly rising from December’s +0.1%.

Lee Kyung-min, a researcher at Daishin Securities, analyzed, "The market still expects about a 50bp interest rate cut from the current peak," adding, "There is an expectation of a soft landing, but considering the current U.S. inflation level, which is more than twice the 2% target set by the Federal Reserve, expecting two rate cuts is still excessive."

He continued, "This week, through U.S. January real economy and inflation data, the market will once again test the balance between expectations for a soft landing and monetary policy," forecasting, "It is more likely to be a turning point where expectations for rate cuts retreat again rather than a favorable investment environment for the market."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}