[Asia Economy Reporter Lee Jung-yoon] The fintech industry is being reorganized into various forms such as Embedded Finance and Buy Now Pay Later (BNPL).

According to 'Fintech Industry Investment Trends and Top 10 Major Trends' published by Samjong KPMG on the 13th, global fintech industry investment, which was severely contracted due to the COVID-19 pandemic, recovered to 8,052 cases and $237.9 billion in 2021, but showed weakness last year due to the interest rate hike trend in major countries.

By investment region, North America and Europe continued to show strength, while the role of fintech expanded in Southeast Asia and Latin America after COVID-19, attracting investors' attention. In particular, despite the overall investment weakness last year, large mergers and acquisitions (M&A) occurred in countries such as Australia.

By sector, the payment sector led investments, while the fintech industry matured, showing trends of diversification and enlargement of investment sectors such as blockchain and virtual assets, wealthtech, and fundraising.

In 2021, the domestic fintech market saw active investment due to accelerated digital transformation and growth of the domestic fintech industry. However, investment was concentrated in big tech and large fintech companies, such as K Bank's 1.25 trillion KRW capital increase in May 2021 and about 1.4 trillion KRW investment attraction by Toss affiliates from 2020 to 2021.

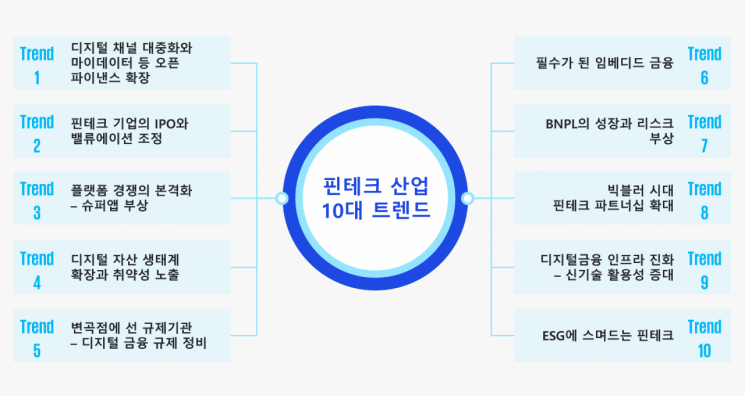

The fintech industry, which has grown by reducing inefficiencies in traditional financial businesses and creating innovative businesses in niche markets, is developing in various forms such as Embedded Finance, BNPL, and super apps along with the advancement of digital financial infrastructure.

Embedded Finance means that non-financial companies not only mediate and resell financial products of financial companies but also internalize fintech functions on their own platforms. The report forecasted that Embedded Finance utilization would be prominent in payment and insurance sectors.

Recently, demand for BNPL services has surged mainly among the MZ generation with no credit history and consumers whose income decreased due to COVID-19. Representative companies include Sweden's Klarna, the U.S.'s Affirm, and Australia's Afterpay. Affirm proved its value by listing on Nasdaq in January 2021. Moreover, Apple, Walmart, and others have entered or announced plans to enter the BNPL market, intensifying competition. However, with recent interest rate hikes in major countries and economic slowdown, concerns about the insolvency of BNPL companies have emerged, leading to discussions on the need for regulatory oversight by financial authorities.

As platform competition intensifies, super apps have also emerged. Super apps refer to apps that connect multiple services such as shopping, remittance, and investment within a single platform. Especially platforms in Southeast Asia and China are expanding into comprehensive financial platforms covering both daily life and finance, serving as core infrastructure in everyday life. The super app strategy, which has been mainstream in Asia, is also showing notable expansion in the U.S. and Europe.

Furthermore, the report emphasized, "As digital channels and the popularization of cashless transactions continue and the open banking era begins in earnest, securing and strengthening non-face-to-face platform channels for financial service providers is essential."

It also stated that it is important to seek data openness and sharing strategies to preoccupy the digital financial ecosystem, and there is a need to monitor regulatory restructuring situations such as financial systems, financial consumer and data protection, and the advancement of regulatory sandboxes.

Jae-bak Cho, Vice President and Fintech Industry Leader at Samjong KPMG, said, "To provide financial services that customers are willing to pay for, it is time to consider a specialized business strategy unique to the company, as well as B2B and B2B2C service models that can create synergy not only in B2C but also in linking with existing financial businesses and expanding non-financial sectors." He emphasized, "To respond quickly to changes in financial consumers' preferences, companies should actively consider differentiation and partnerships to provide innovative customer experiences based on their own business."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}