Frozen Retail Sales

Global Financial Crisis

Lower Than the Impact of COVID-19

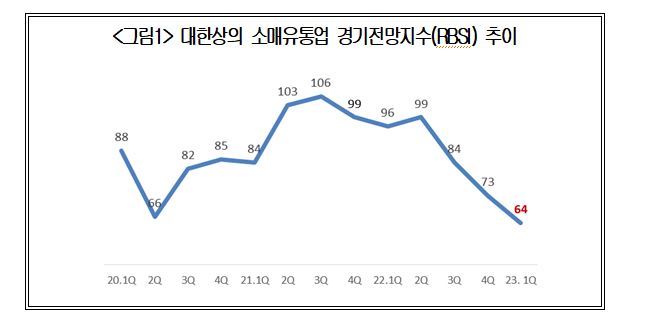

[Asia Economy Reporter Jeong Dong-hoon] The retail sector's business sentiment has sharply declined for the third consecutive quarter, signaling a consumer downturn.

The Korea Chamber of Commerce and Industry (KCCI) announced on the 15th that the 'Q1 Retail Business Sentiment Index' surveyed among 500 retail companies was recorded at '64.' This outlook is even lower than during the global financial crisis (73) and the COVID-19 shock period (66). An RBSI above 100 means 'more companies view the next quarter's retail business more positively than the previous quarter,' while below 100 indicates the opposite.

KCCI analyzed, "With domestic and international uncertainties such as high inflation, high interest rates, and asset price adjustments unlikely to be resolved in the new year, coupled with various public utility fee hikes maintaining high price levels and the inevitable continuation of a high interest rate policy to curb inflation, concerns about a difficult consumer recovery persist."

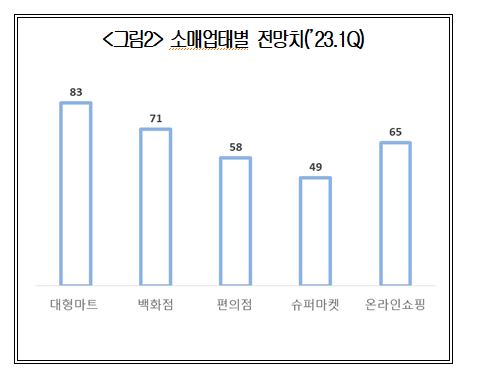

Large Discount Stores (83), Department Stores (71), Online Shopping (65), Convenience Stores (58), Supermarkets (49) in order

All sectors fell below the baseline (100), with large discount stores (83) expected to perform relatively better. Department stores (71), convenience stores (58), and supermarkets (49) showed low business expectations. Online shopping (65) is also unlikely to escape the overall downward trend despite its strong price competitiveness.

Large discount stores recorded '83,' the highest outlook among sectors. Expectations for converting mandatory closure days to weekdays and allowing online delivery positively influenced the index. Additionally, the fact that food, the main product category of large discount stores, is an essential good that consumers cannot avoid purchasing even during a recession, along with the Lunar New Year sales boost, contributed positively to rising expectations.

Department stores (71) also showed significantly lowered business expectations. Until the previous quarter, despite overall consumer sentiment contraction, department stores had higher business expectations than other sectors due to revenge spending and endemic effects. However, with growing concerns over asset value declines and economic recession, department stores, frequented by high-income customers, are also expected to underperform.

Convenience stores (58), known to be resilient during recessions, also showed low outlooks. Particularly, intense competition among convenience stores and increased labor costs due to minimum wage hikes negatively impacted the outlook. The hourly minimum wage actually rose by 5% from 9,160 KRW last year to 9,620 KRW this year. Additionally, reduced winter foot traffic appears to have contributed to the sluggish performance.

Supermarkets (49) are expected to continue their poor performance this quarter. The sustained low business expectations compared to other sectors are attributed to the recession impact and intensified competition with large discount stores, convenience stores, and online channels, making sales recovery difficult. In fact, companies are making efforts such as store closures, renovations, and strengthening delivery services to overcome poor performance.

Online shopping (65) also significantly lowered its business expectations. Concerns over the recession and a reverse base effect following the high growth before the endemic phase contributed to the index decline. Furthermore, the reopening has led to a substantial shift in demand back to offline retail, raising worries about sales decreases.

Key Strategies for the New Year ... Cost Reduction, Strengthening Online, Enhancing Promotions in order

The most prioritized strategy for the new year was cost reduction (48.2%), followed by strengthening online channels (32.0%), enhancing promotions (25.6%), store renovations (19.2%), and product development (18.4%).

Recent management difficulties cited were consumption contraction (34.6%), rising costs (25.2%), consumer price inflation (11.8%), increased product procurement costs (10.8%), and intensified market competition (10.4%), in that order.

Jang Geun-moo, Director of the KCCI Distribution and Logistics Promotion Institute, said, "Uncertainties in global financial and raw material markets remain unresolved amid economic recession and inflation. It is necessary to prepare mid- to long-term response plans along with expanding active marketing strategies to stimulate consumption in anticipation of prolonged consumer sluggishness."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}