Dongwon Enter - Dongwon Industries Merger Increases Share Value

Raising Stake Through No-Price Capital Increase to Merge Key Subsidiaries

Controversies Over Merger Ratio and Buyout Price Persist

[Asia Economy Reporter Park So-yeon] Kim Nam-jung, Vice Chairman of Dongwon Group, has newly entered the list of stockholders with shares worth over 1 trillion won in listed companies as his share value significantly increased due to the restructuring of the governance structure.

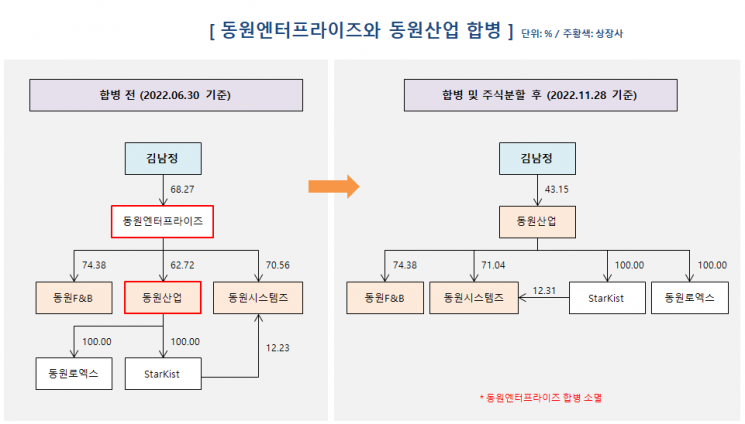

Kim Nam-jung, the largest shareholder of Dongwon Industries, holds 21,569,875 shares (43.15%) of Dongwon Industries, which were valued at a total of 1.0354 trillion won based on the closing price (48,000 won) on the 29th. This market value of Kim’s shares emerged after Dongwon Industries merged with Dongwon Enterprises, the unlisted holding company of Dongwon Group, on the 16th and was relisted.

According to the first business report (2007) of Dongwon Enterprises, which had long served as an unlisted holding company, Kim Nam-jung was the largest shareholder holding 3,612,789 shares (67.23%) of Dongwon Enterprises. Subsequently, on October 21, 2015, a bonus issue was conducted at a ratio of 1.2 new shares per share, increasing Kim’s holdings to 7,948,135 shares. Before the merger with Dongwon Industries, the number of shares increased to 7,981,904 (68.27%).

After the merger and listing of Dongwon Industries and Dongwon Enterprises on the 16th, Dongwon Enterprises, which was the largest shareholder of Dongwon Industries, was dissolved. Instead, Kim Nam-jung, the largest shareholder of Dongwon Enterprises, became the largest shareholder of Dongwon Industries, holding 4,313,975 shares (43.15%). Through this process, he entered the list of stockholders with shares worth over 1 trillion won for the first time. On the 28th, a stock split was conducted, reducing the par value from 5,000 won to 1,000 won, and the listing was completed. Kim’s number of shares increased to 21,569,875, with a total valuation of 1.0375 trillion won.

With the merger of Dongwon Enterprises and Dongwon Industries, the governance structure of Dongwon Group shifted to center around Dongwon Industries. Major companies, including Dongwon F&B and Dongwon Systems, subsidiaries of Dongwon Enterprises, as well as the grandson company StarKist (the number one canned tuna company in the U.S.) and Dongwon Loex (formerly Dongbu Express), were incorporated under Dongwon Industries.

During the restructuring process, there was controversy over the fairness of the merger ratio. It was claimed that Dongwon Group inflated the corporate value of Dongwon Enterprises and lowered that of Dongwon Industries to calculate the merger ratio excessively favoring the major shareholder, Kim Nam-jung. Initially, the merger ratio between Dongwon Industries and Dongwon Enterprises was set at 1 to 3.84, meaning one share of Dongwon Enterprises would receive 3.84 shares of Dongwon Industries. When converted to corporate value based on the per-share valuation of Dongwon Industries (248,961 won), the value was in the 900 billion won range, whereas the corporate value based on Dongwon Enterprises’ per-share valuation (191,130 won) exceeded 2 trillion won.

Namjung Kim, Vice Chairman of Dongwon Group

Namjung Kim, Vice Chairman of Dongwon Group

As the controversy escalated, Dongwon Group decided to change the merger price of Dongwon Industries from the standard market price to the net asset value basis. Dongwon Industries initially intended to apply the merger price at 248,961 won per share based on the standard market price in the merger with Dongwon Enterprises, but instead reflected a merger price of 382,140 won per share based on net asset value. The merger ratio was adjusted from 1 to 3.84 to 1 to 2.7. Before the adjustment, Kim Nam-jung’s stake in Dongwon Industries after the merger was 48.43%, but it decreased to 43.15% after the adjustment. Dongwon Group explained that the merger ratio was improved to enhance shareholder value for minority shareholders and restore company trust.

However, disputes over the fairness of the merger ratio continue. There are claims that the value of affiliate shares remains unfavorable to Dongwon Industries’ shareholders. There are also assertions that the price for the shareholders’ right to demand purchase in opposition to the merger is excessively low. An investment banking industry insider said, "Kim increased his stake in Dongwon Enterprises through bonus issues and secured a favorable merger ratio, significantly boosting the value of his holdings," adding, "A legal battle over the merger ratio and the price of the right to demand purchase in opposition to the merger is anticipated."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}