Already Stable Delinquency Rate Management

Sufficient Provisioning for Bad Debts

Profit Growth Possible Even with Reduced Loans Next Year

[Asia Economy Reporter Minwoo Lee] There is an analysis that the delinquency rate in the banking sector has reached a level that is difficult to lower further. Despite concerns about the economy, future loan loss costs are expected to remain stable, and profits next year are projected to increase slightly.

According to the Financial Supervisory Service announcement on the 19th, the domestic banks' delinquency rate for loans overdue by more than one month in September was 0.21%, down 3 basis points (bp; 1bp=0.01%) from the previous month. Compared to 0.24% in the same period last year, it decreased by 0.02 percentage points. The decline in the delinquency rate is believed to be due to the usual cleanup of about 1.7 trillion KRW in overdue loans at the end of the quarter.

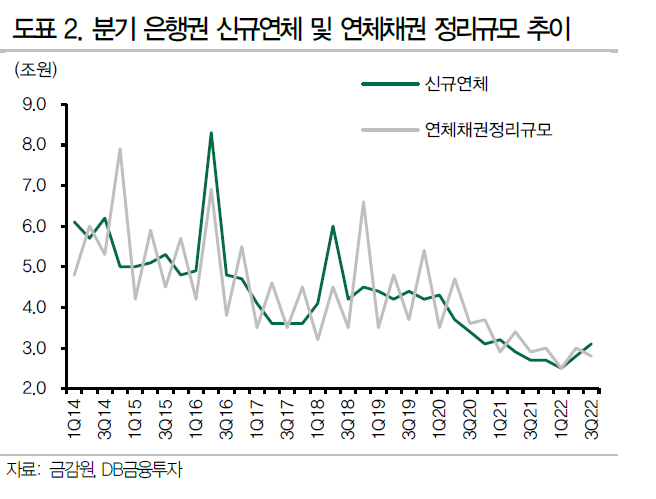

Researcher Byunggeon Lee of DB Financial Investment explained, "Compared to 2.3 trillion KRW in September 2020, 1.7 trillion KRW in September last year, and 1.6 trillion KRW in June, the cleanup scale is not large," adding, "We confirmed low delinquency rates across all sectors, including 0.33% for small and medium-sized corporations, 0.19% for individual business owners, 0.12% for mortgage loans, and 0.37% for household credit loans."

The delinquency rate is evaluated to be at a level so low that further decline is difficult. It dropped from around 0.8?1.0% in 2015 to below 0.4% after COVID-19 in 2020. The reduction in overdue loan cleanup at the end of the quarter is interpreted as reflecting a trend of decreasing new delinquencies. Researcher Lee analyzed, "Since 2020, the amount of new quarterly delinquencies has fallen to about 3 trillion KRW, and the increase in the delinquency rate excluding the cleanup of delinquent loans has decreased to less than 7bp," adding, "Through the effect of cleaning up delinquent loans, the delinquency rate has been stably maintained at the 0.2% level."

The banks' loan loss provision transfer ratio (CCR) is maintaining an average level of about 20bp. Considering that the net increase in delinquencies before cleanup was 7bp in the quarter, a significant amount is estimated to have been recognized as loan loss costs arising from net credit growth. Since banks have proactively recognized provision costs in consideration of the government's end of COVID-19 financial support, and loan growth rates are expected to slow next year, loan loss costs are anticipated to remain stable. Researcher Lee forecasted, "Despite the slowdown in loan growth rate, the deceleration in net interest margin (NIM) increase, and an uncertain non-interest income environment, bank profits are expected to increase slightly."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}