As of August, Fixed-Rate Loans Account for 24.4% of New Loans... Highest in 1 Year and 4 Months

With Benchmark Interest Rates Continuing to Rise, Borrowers Begin Turning to Fixed Rates

As the U.S. central bank, the Federal Reserve (Fed), hinted at additional interest rate hikes, attention is increasing on whether the Bank of Korea's Monetary Policy Committee will raise rates at its meeting scheduled for the 25th. The photo shows a loan counter at a commercial bank in downtown Seoul on the 19th. Photo by Kim Hyun-min kimhyun81@

As the U.S. central bank, the Federal Reserve (Fed), hinted at additional interest rate hikes, attention is increasing on whether the Bank of Korea's Monetary Policy Committee will raise rates at its meeting scheduled for the 25th. The photo shows a loan counter at a commercial bank in downtown Seoul on the 19th. Photo by Kim Hyun-min kimhyun81@

[Asia Economy Reporter Sim Nayoung] In recent months, as the United States and South Korea have alternately raised their benchmark interest rates significantly each month, the proportion of fixed-rate mortgage loans, which had been stagnant, has started to increase. Although fixed rates are somewhat higher than variable rates at the time of borrowing, borrowers are increasingly choosing fixed rates based on the calculation that as variable rates rise over time, fixed rates will ultimately be more advantageous.

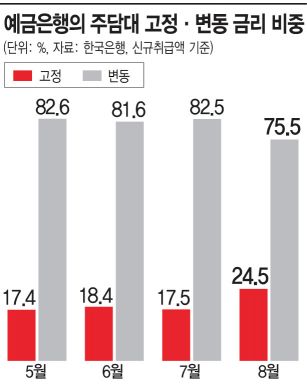

According to the Bank of Korea's Economic Statistics System on the 5th, as of August's new loan amounts, the proportion of fixed rates at deposit banks was 24.5%, and variable rates accounted for 75.5%. These are the highest and lowest levels, respectively, in one year and four months. Since February, six months ago, fixed rates have consistently been in the 10% range, while variable rates have been in the 80% range.

In June, the share of variable rates reached 82.6%, the highest since January 2014. However, the trend changed starting in August.

In July, the U.S. Federal Open Market Committee (FOMC) took a giant step (a 0.75 percentage point increase in the benchmark rate), and South Korea followed suit with a big step (a 0.5 percentage point increase), signaling that further rate hikes are expected. As a result, more and more borrowers are turning to fixed-rate loans, which apply the same rate for five years.

During periods of rising interest rates, although variable rates may seem cheaper initially, choosing fixed rates over time is a way to save on interest costs. Variable rates change every six months, reflecting increases in the COFIX rate.

For example, someone who took out a loan with a variable rate of 3.33% on October 4 last year saw the rate rise to 4.01% in April this year and currently to 5.27%. For a borrower who took out 400 million KRW on a 30-year amortization schedule, the monthly payment including principal and interest sharply increased from 1.75 million KRW → 1.9 million KRW → 2.2 million KRW during the same period.

On the other hand, a borrower who took out a loan with a fixed rate of 3.38%, which was 0.05% higher than the variable rate a year ago, has a monthly payment fixed at 1.87 million KRW for five years. Ultimately, after one year, the variable rate borrower ends up paying more interest than the fixed rate borrower.

An official from a commercial bank said, "If interest rates rise further, the burden on variable rate borrowers will increase more than now," adding, "The gap in interest costs between fixed rate borrowers and variable rate borrowers will inevitably widen."

As of October 4, commercial bank interest rates still show fixed rates (5.04?7.06%) ahead of variable rates (4.50?6.77%). Nevertheless, the decrease in the proportion choosing variable rates indicates that borrowers' concerns about rising interest rates are significant.

Meanwhile, as of August's new loans, household loan interest rates in the 4% range accounted for 55.4%, the highest since February 2013. Loans with interest rates in the 5% range also accounted for 11%.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}