Totaling 141 Trillion Won, 570,000 People Eligible

Economic Conditions Worsen Due to High Interest Rates, High Inflation, and High Exchange Rates

More Time Needed for Crisis Response

[Asia Economy Reporter Sim Nayoung] The Financial Services Commission announced on the 27th that it will provide additional support of up to 3 years of maturity extension and up to 1 year of repayment deferral for self-employed borrowers who are currently utilizing maturity extension and repayment deferral measures in the financial sector following the COVID-19 pandemic.

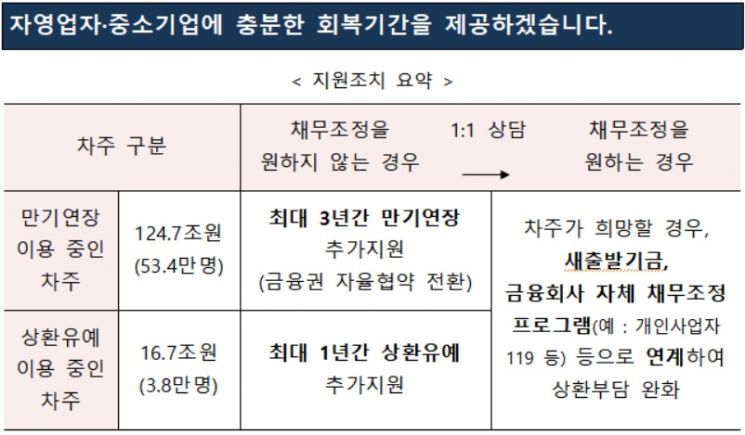

As of the end of June, the debt amount subject to these measures stands at 141 trillion KRW (124.7 trillion KRW for maturity extension, 12.1 trillion KRW for principal deferral, and 4.6 trillion KRW for interest deferral). A total of 570,000 borrowers (534,000 for maturity extension and 38,000 for principal deferral) are currently using these measures.

As the COVID-19 impact prolonged, this system has been operated for 2 years and 6 months with repeated extensions every 6 months (four extensions so far). This is the fifth extension.

Maturity Extension Extended by 3 More Years; If Still Unable to Repay, Use the New Start Fund

The support targets are small and medium-sized enterprises (SMEs) and small business owners affected by COVID-19. It applies only if there is no insolvency such as principal and interest arrears, capital erosion, or business closure. This measure was applied to individual business owners and SMEs who took out loans before March 31, 2020.

A Financial Services Commission official stated, "With the full lifting of quarantine measures, the operations of self-employed and SMEs are gradually normalizing," but added, "Due to worsening economic conditions caused by high interest rates, high inflation, and high exchange rates, it is expected that it will take some more time for a full recovery."

He continued, "If the maturity extension and repayment deferral measures end as scheduled at the end of September, there is a risk that many self-employed and SMEs will fall into default," and explained, "Since this could increase financial system risks due to the spread of financial sector insolvency, sufficient crisis response time has been granted to support the recovery of self-employed and SMEs."

Since July, the Financial Services Commission has been operating a 'Maturity Extension and Repayment Deferral Consultative Body' together with the Ministry of SMEs and Startups, the Financial Supervisory Service, and all financial sectors. The consultative body decided to convert the previously uniform maturity extension into a voluntary agreement between the financial sector and debtors, while extending the maturity extension period for borrowers up to 3 years.

The 3-year period also coincides with the application period for the New Start Fund, which provides debt relief for self-employed borrowers who have been overdue for more than 90 days. Setting the maturity extension to 3 years is intended to handle non-performing loans through the New Start Fund if insolvency occurs during the maturity extension period.

Borrowers Using Repayment Deferral Must Establish Repayment Plans by March Next Year

Borrowers currently using repayment deferral measures can additionally use up to 1 year of repayment deferral until September next year. A Financial Services Commission official said, "Instead of the previous 6-month deferral, we are supporting up to 1 year of repayment deferral so that borrowers facing ongoing liquidity difficulties can repay their loans after normal business recovery."

Borrowers using repayment deferral must consult with financial institutions by March next year to establish a repayment plan for the deferred principal and interest after the deferral period ends in September next year, as well as for future principal and interest payments. Through one-on-one consultations between financial institutions and borrowers, repayment plans will be made considering the borrower's business recovery speed and repayment scale comprehensively after the repayment deferral ends.

This measure was introduced by the Financial Services Commission in response to criticism that "providing an additional 1-year repayment deferral is a blind support for borrowers without repayment ability." The Commission stated, "To prevent the additional repayment deferral from simply buying time for borrowers without repayment ability, we have made it mandatory to prepare a normal repayment plan during the deferral period."

The Financial Services Commission also stated that if borrowers wish to adjust their debts rather than use maturity extension or repayment deferral measures, they can use the 'New Start Fund' (worth 30 trillion KRW), scheduled to launch from the 4th of next month. This fund supports not only extension of repayment periods but also adjustments such as interest rates depending on each borrower's situation.

For SMEs not eligible for the New Start Fund, debt adjustment support such as rapid financial assistance will be provided through credit risk evaluation. For companies with loans exceeding 3 billion KRW, after evaluation, the process will proceed with 'voluntary management improvement recommendations and rapid financial support' or 'workout and rehabilitation procedures' depending on the results.

Meanwhile, the Financial Services Commission plans to supply an 8.5 trillion KRW low-interest refinancing program through 14 banks from the 30th, converting high-interest business loans of self-employed and small business owners affected by COVID-19 into low-interest loans. To help SMEs reduce the burden of rising interest rates during the rate hike period, a 6 trillion KRW fixed-rate loan product with lowered interest rates will also be introduced. The so-called 'Safe Fixed-Rate Special Loan' will start on the same day through the Korea Development Bank and the Industrial Bank of Korea.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}