Hi Investment & Securities Report

[Asia Economy Reporter Lee Myunghwan] Hanjin, a logistics company that parted ways with Coupang, posted results below expectations in the second quarter of this year. This was due to Coupang shifting some of the volume it had entrusted to Hanjin Delivery since June to its own delivery system. Securities firms predicted that if Hanjin shows a quick recovery, it could lead to a rebound in its stock price.

On the 9th, Hi Investment & Securities analyzed Hanjin, stating, "The key is the quick recovery from the decrease in Coupang volume." Along with this, they maintained a buy rating on Hanjin but lowered the target price from 40,000 won to 36,000 won.

Hanjin's consolidated sales for the second quarter of this year increased by 19.2% year-on-year to 714.9 billion won, and operating profit grew by 18.5% to 32.6 billion won. However, these results fell short of market expectations, with Hi Investment & Securities attributing the weak performance to the loss of Coupang volume in the parcel delivery segment.

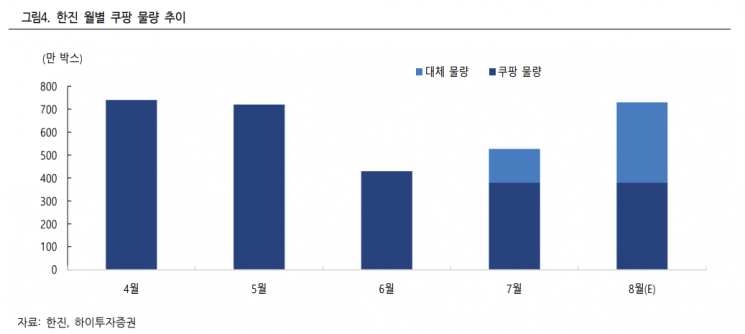

Since June, Coupang has shifted a significant portion of the parcel volume it had entrusted to Hanjin to its own delivery system. Consequently, Hanjin's volume decreased by 3.7 million boxes starting in June. The volume Hanjin delivered on behalf of Coupang was about 7.2 to 7.4 million boxes per month. Due to the loss of Coupang volume, sales declined, and additional operating costs and fixed cost burdens caused Hanjin's parcel delivery segment operating profit in the second quarter to sharply drop to 800 million won.

Hi Investment & Securities pointed out that the key for Hanjin in the second half of this year is how quickly it can replace the reduced Coupang volume in the parcel delivery segment. To compensate for the decrease, Hanjin secured 1.47 million boxes of volume from existing clients in July. Furthermore, it plans to secure 2.03 million boxes through new contracts in August. If the new volume is secured as planned, Hi Investment & Securities expects recovery to pre-Coupang departure levels. However, they analyzed that the critical factor is whether the new clients can provide a stable volume comparable to Coupang.

Nevertheless, Hi Investment & Securities expects the parcel delivery segment's performance to remain sluggish in the second half of this year. This is due to unavoidable increases in operating costs such as higher trunk haulage fees, surcharges for labor, and commission fees at collection and delivery points related to acquiring new replacement volume.

Lee Sangheon, a researcher at Hi Investment & Securities, said, "Hanjin's stock price has continued to show a sluggish trend," but added, "If the replacement of Coupang's reduced volume is achieved and a quick recovery is demonstrated, it could be a turning point for a stock price rebound."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}