[New Interest Rate Nomad]④

Investment Deposits, Stock Trading Volume, Bitcoin, and Real Estate Indicators All Declining

Massive Fund Shift to Safe Assets... 757 Trillion Won Concentrated in Time Deposits

"Switching Only to Time Deposits Is Not Enough" Prepayment Deferral and Other Financial Techniques Gaining Popularity

[Asia Economy Reporters Yu Je-hoon and Lee Min-woo] As interest rates continue to rise and concerns about an economic recession emerge due to various external factors such as the war between Russia and Ukraine, a different flow of funds compared to previous years is being detected. While funds have rapidly exited the stock and virtual asset markets, which were considered the most preferred investment options until last year, there is a trend of money flowing into safe assets such as bank deposits and bonds, which had been avoided.

Market Funds Experience ‘Ebb Tide’

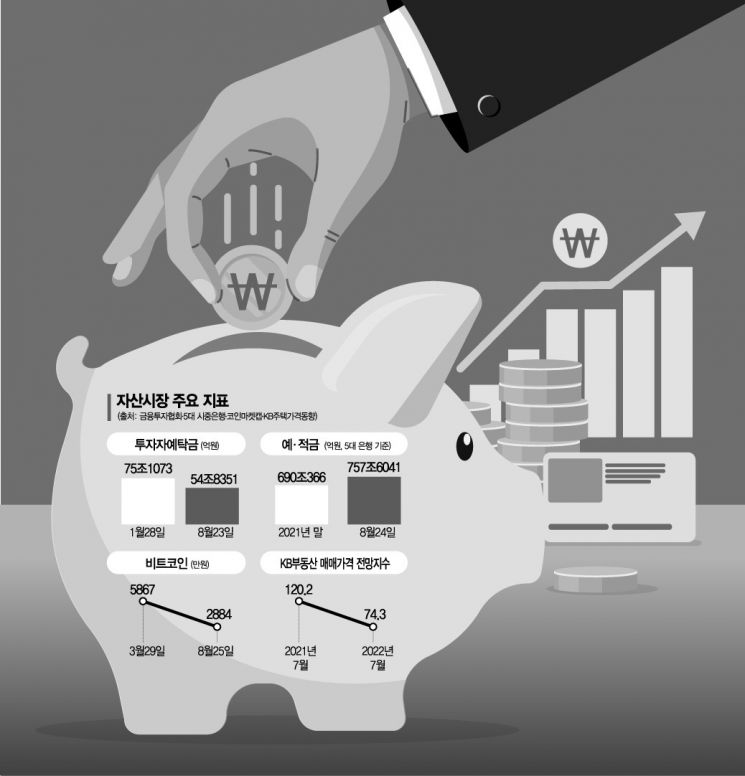

According to the Korea Financial Investment Association on the 25th, investor deposits, which serve as standby funds for stock purchases, stood at 54.8351 trillion won as of the 23rd. Compared to the record high of 75.1073 trillion won at the beginning of the year (January 28), this represents a sharp decline of about 27%. On the 20th of last month, it even dropped to 53.4922 trillion won. This is the first time since November 2020, when COVID-19 was at its peak, that investor deposits have fallen to the 53 trillion won level.

Trading volume also plummeted. According to the Korea Exchange, the trading value in the KOSPI market on the previous day was 8.1198 trillion won. Compared to the 44.4338 trillion won recorded on January 11, 2021, it has shrunk by about 82% in just one year and seven months. The KOSPI index, which hovered around the 3000 level in 2021, has dropped to the 2400 range this month.

The virtual asset market has also cooled down. According to CoinMarketCap, which tracks global virtual asset market conditions, the price of Bitcoin, the largest virtual asset by market capitalization, rose to 58.67 million won on March 29 but has been fluctuating around the 28 million won range this month. The investment assets that were most favored after COVID-19 are all showing signs of decline.

Even the real estate market has contracted amid the global interest rate hike. According to the KB Housing Price Trend monthly time series statistics, the nationwide KB Real Estate Sales Price Outlook Index was 74.3 as of last month. This is the lowest since the survey began in April 2013. After reaching an all-time high of 120.2 in July last year, it has recorded the lowest level in a year. The KB Real Estate Sales Outlook Index quantifies the outlook on apartment prices over the next three months based on surveys of real estate agencies; an index above 100 indicates a majority expect prices to rise, while below 100 indicates a majority expect prices to fall.

Safe Assets ‘High Tide’... "Simple Deposits Not Enough"

As asset markets enter a downturn one after another, market funds are flowing into safe assets. Kwon Seong-jung, head of the PB Center at Hana Bank’s Sales Division 1, explained, "Although the stock market briefly rebounded in July, it fell again, reducing expectations for the asset market, and funds are steadily moving into safe assets such as deposits and bonds. Even during low-interest periods, some customers wanted to move their funds if they could earn 4-5% returns in safe assets, and now that such a time has come, investor interest is significantly shifting."

A representative example is deposits. The balance of fixed deposits at the five major commercial banks (KB Kookmin, Shinhan, Hana, Woori, NH Nonghyup) reached 757.6041 trillion won as of the 23rd, an increase of 67.5675 trillion won compared to the end of last year. Last month, fixed deposits alone recorded 712.4491 trillion won, surpassing 700 trillion won for the first time. Meanwhile, demand deposits, which serve as standby investment funds, remained at 664.9009 trillion won, down more than 45 trillion won from the end of last year.

The attitude of financial consumers with deposits has also changed. Deposit interest rates, which were practically ‘negative’ during the ultra-low interest rate era, have surged to 3-4%, and in some cases as high as 4-5%. It has become common for customers to line up in front of financial institutions to subscribe to special promotional products.

Recently, simple switching of deposits is considered insufficient, and many people are sharing ‘smart’ financial techniques online. A representative example is ‘Seonnap Iyeon’ (Prepayment and Deferral). Seonnap Iyeon is a financial technique that uses installment savings (regular savings) together with lump-sum deposits (fixed deposits).

Looking at the principle, in the case of regular savings, if the agreed monthly payment is paid in advance, ‘prepaid days’ occur, and if paid late, ‘deferred days’ occur. The larger the deferred days, the more the maturity date is postponed, but if the sum of prepaid and deferred days equals zero, the maturity date does not change. This difference is used to maximize interest gains. For example, if a financial consumer with a lump sum of 12 million won subscribes to a fixed deposit product with a 3% annual interest rate and a one-year maturity, the interest receivable at maturity is 360,000 won. Even if this is divided and paid into a 5% one-year installment savings product, the interest at maturity remains around 325,000 won.

On the other hand, if the consumer subscribes to the same installment savings product following the common ‘6-1-5’ method?paying 6 months’ worth (6 million won) in the first month, one month’s worth (1 million won) in the seventh month, and the remaining five months’ worth (5 million won) in the last month?the maturity date is not delayed, and the interest received is 325,000 won (before tax). If the 1 million won to be paid in the seventh month and the 5 million won to be paid in the last month are each placed in a 3% fixed deposit product with 6-month and 11-month maturities, respectively, the interest earned is 15,000 won and 137,500 won, totaling 152,500 won. The total interest thus amounts to 477,500 won, which is 117,500 won more than the fixed deposit interest. However, this may not be applicable at all financial institutions, so it is necessary to carefully review the terms and conditions.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}