[New Interest Rate Nomad] ⑤

Individual Net Purchases Surpass 10 Trillion Won This Year... Highest Since Statistics Disclosure

Principal and Interest Protection Unless Issuer Defaults

Popular Among Corporate Bonds and Specialized Credit Finance Bonds

[Asia Economy Reporters Jehoon Yoo, Minji Lee] One of the areas where idle funds in the market have recently been rapidly flowing is the bond market. The fact that principal and interest are guaranteed unless the issuing institution declares default, and that capital gains can be expected even when interest rates fall, have drawn attention. Recently, for the first time since related statistics were disclosed, the net purchase amount by individuals surpassed 10 trillion won.

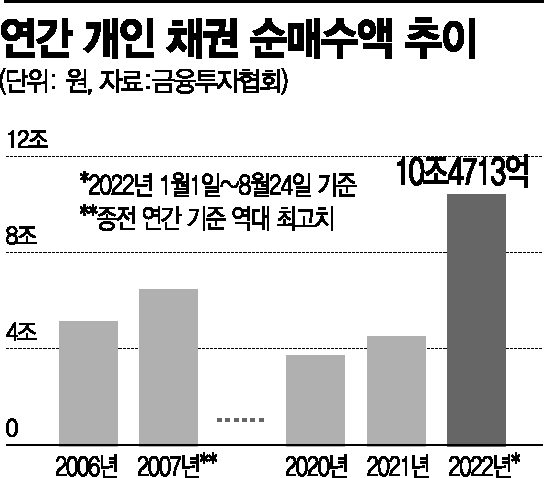

Individual Bond Net Purchases Surpass 10 Trillion Won for the First Time

According to the Korea Financial Investment Association on the 25th, the net purchase amount of bonds by individuals from the beginning of the year until the day before was recorded at 10.4713 trillion won, an increase of about 199% compared to the same period last year. This not only exceeded twice the annual net purchase amount by individuals last year (4.5675 trillion won) but also marked the first time since the Korea Financial Investment Association began disclosing related statistics in 2006 that the annual net purchase amount surpassed 10 trillion won.

By bond type, corporate bonds accounted for the largest portion at 4.7227 trillion won, followed by other financial bonds excluding bank bonds at 3.2346 trillion won. Others included government bonds (1.3049 trillion won), special bonds (653.5 billion won), and asset-backed securities (ABS, 385.9 billion won).

The net purchase amount of bonds by individuals peaked at 6.5143 trillion won in 2007 but has not shown a significant rebound since. Since 2017, the annual net purchase amount has remained in the range of 3 to 4 trillion won. The reason the bond market, which has shown a quiet yet dynamic trend, is gaining attention is due to the characteristics of bonds as safe assets. Bonds guarantee principal and interest as long as the issuing institutions such as governments, financial institutions, or general companies do not face default. Also, due to the inverse relationship between bond prices and interest rates, capital gains can be realized through sales when interest rates fall later.

The rise in bond yields is also a major cause. As of the final bid yield on the previous day, the interest rate on AA-rated 3-year corporate bonds was 4.298%, an increase of 183 basis points (1bp=0.01%) compared to the beginning of the year, which is comparable to the interest rates of deposit and savings products offered by commercial banks. According to the Bank of Korea, as of June, the weighted average interest rates of deposit banks were 2.74% for time deposits (1 year or more but less than 2 years) and 2.32% for installment savings.

Large Corporations Also Offer Interest Rates in the 4% Range... Increased Inquiries for Card and Capital Bonds

Recently, the corporate bond market has broadened the investment scope for individuals. As large corporations, which are considered low risk, offer bond interest rates higher than deposit and savings rates, investor inquiries for purchases have surged. A representative from a small to mid-sized securities firm said, "Even if banks offer special high-interest deposits, there are often limits on the amount or conditions such as having to create a card, making it difficult to fully receive the stated interest rate. Bond investment does not have such barriers. When attractive interest rate products are released to the market, large securities firms sell out within 10 minutes, and smaller firms within 30 minutes."

The corporate bond that has received the most attention in the retail bond market is undoubtedly Korea Electric Power Corporation (KEPCO, AAA rating). This is because KEPCO has issued a large volume of corporate bonds to resolve liquidity issues, resulting in high interest rates. The issuance rate for a 2-year bond issued by KEPCO in November 2020 was 1.019%, but the bond issued under the same conditions this month had an interest rate of 4.14%, about four times higher. Investment inquiries for card and capital bonds, which are mostly short-term (2-year maturity) with low coupon rates, have also increased.

The popularity of these bonds is due to the fact that although the fixed coupon payments are low and thus the taxable base is low, the capital gains at the time of sale are large, allowing profits in the mid-4% range based on bank-equivalent yields. Bonds are subject to a 15.4% tax on fixed interest, but capital gains from direct investment are not taxed. For example, the coupon rate of Mirae Asset Capital (AA) bonds issued in the first half of the year was 1.63%, and trading profits were in the 4% range, resulting in a bank-equivalent yield of 4.48%.

As the base rate hike rally is expected to continue until the end of this year, interest in bonds is expected to grow further. A representative from a large securities firm explained, "Since bond yields are influenced by the base rate set by the Bank of Korea, the current interest rate levels of corporate bonds or government bonds are unlikely to drop significantly until rates stabilize. Recently, interest in monthly interest payment bonds, which pay interest on a 1-month or 3-month basis, has also increased." A private banker (PB) at a commercial bank also said, "Recently, bond investment considering capital gains from next year's interest rate cuts has been greatly activated in the field. Recently, products such as 10-year US Treasury bonds with interest rates rising to the 3% range and tax-saving bonds with low coupon rates but no tax on capital gains have been popular, especially among high-net-worth individuals."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}