Savings Banks in Emergency Due to New Start Fund and Low-Interest Refinancing

Simulation Shows "Impact Greater Than Expected"

"Let's Select Only Creditworthy Small Business Owners for Loans"

'Paradox of Good Intentions' Makes Vulnerable Groups Worse Off

[Asia Economy Reporter Song Seung-seop] The savings bank industry is on high alert ahead of the launch of various policy finance programs. There are concerns that a significant portion of customers, ranging from delinquent small business owners to normal borrowers, could be lost, leading to a greater impact than expected. Some savings banks are even suggesting reducing the small business loan sector. Criticism is emerging that government financial policies, initiated with good intentions, are creating a lending cliff that shrinks the private sector loan market.

According to the industry on the 11th, recently at A Savings Bank, the CEO held a meeting in preparation for the implementation of the 'New Start Fund' and the 'Low-Interest Refinancing Program.' At the meeting attended by executives and relevant department heads, an analysis was presented showing that if the measures currently being discussed are implemented, the losses would be enormous. One executive even voiced strong opposition, saying, "This policy makes no sense."

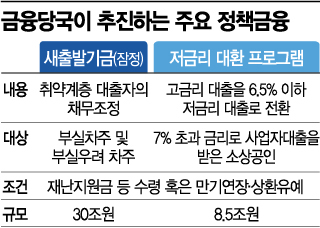

The New Start Fund and the Low-Interest Refinancing Program are key policies promoted by the Financial Services Commission. The New Start Fund targets small business owners affected by COVID-19 who are struggling to repay loans. Through the New Start Fund, they can receive debt adjustments such as principal forgiveness. The Low-Interest Refinancing Program targets small business owners who took out business loans with interest rates exceeding 7%, allowing them to switch to bank loans with interest rates below 6.5%.

The savings bank industry is concerned that these two policies will lead to major customers receiving principal forgiveness and debt adjustments or moving their loans en masse to commercial banks. As a result, there are signs of reconsidering strategies for the small business loan sector. Previously, loans were extended even to low-credit small business owners who came to the counters, but going forward, only creditworthy small business owners will be selected and lent to at medium interest rates. This policy intended to help vulnerable groups ironically raises the loan barriers for those very groups, a 'paradox of good intentions.'

Savings Bank Industry: "Small Business Owners Dependent on Government Support Must Be Selected Carefully"

At B Savings Bank, after reviewing simulation results assuming the implementation of policy finance, they decided to revise their small business loan strategy. They plan to identify small business owners who will not leave or go bankrupt and who will repay loans well. They will enhance loan verification capabilities to filter out small business owners heavily dependent on government support. A B Savings Bank official explained, "The expected loss scale is by no means small," adding, "We judged that there is a high possibility that such policy finance or systems will continue to emerge."

Savings banks are also worried that the scope of policy finance support is excessively broad. According to the 'Small Business Owner and Self-Employed New Start Fund Debt Adjustment Implementation Plan,' one criterion for borrowers at risk of default is 'those with overdue days between 10 and less than 90 days.' They believe that if the target group is too large and the conditions are easy to meet, moral hazard could occur where borrowers deliberately delay payments and then refuse to repay. Even normal borrowers have many loans with interest rates exceeding 7%, so if they leave, profit deterioration is inevitable.

A C Savings Bank official lamented, "Not only customers with maturity extensions or repayment deferrals but also those who received disaster relief funds are eligible for support, so the impact is significant," adding, "Internally, we consider that virtually all small business owners who borrowed money are included in the target group." He pointed out, "Ultimately, if delinquent customers transfer their overdue claims, it is highly likely that the savings banks' interest income and customer base will decrease in the long term, leading to profitability deterioration."

The financial authorities stated that nothing has been finalized regarding the New Start Fund and that they intend to maintain the current policy stance on confirmed matters. The Financial Services Commission explained, "The scope of borrowers eligible for the New Start Fund is currently under discussion through consultations with the existing financial sector and has not been decided yet." Regarding claims to reduce the principal forgiveness rate, they rebutted, saying, "This is a mistaken criticism arising from a lack of understanding," and added, "Principal forgiveness through the New Start Fund is only applied in very limited cases, and borrowers with sufficient income and assets cannot receive principal forgiveness."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}