[Asia Economy Reporter Lee Seon-ae] Corporate earnings warning signals are growing louder. Earnings forecasts have begun to be revised downward. This is expected to act as an additional downside factor for the domestic stock market.

According to Cape Investment & Securities on the 2nd, this year's annual operating profit forecast for the KOSPI fluctuated between 246 trillion and 256 trillion won since the beginning of the year. Since mid-June, the operating profit forecasts for the KOSPI in 2022 and 2023 have started to be revised downward. The reason for concern over this downward revision is that the semiconductor sector has begun to be downgraded. Since the semiconductor sector accounts for about 32% of the entire KOSPI, once it starts to decline, it can pull down the overall operating profit forecast for the KOSPI this year.

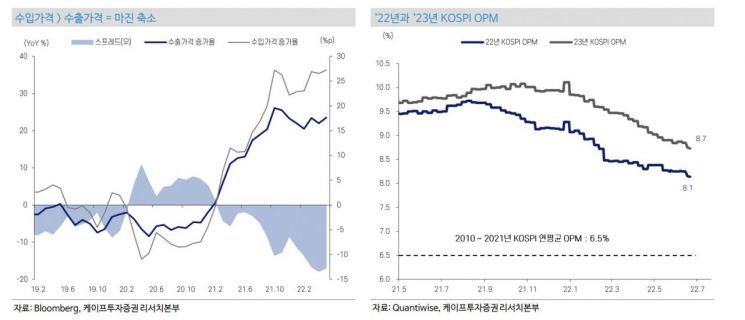

The KOSPI operating profit margin is also continuously being revised downward. Since the outbreak of the Russia-Ukraine war, the rise in energy and raw material prices has caused import prices to increase faster than export prices. The rise in crude oil and major raw material prices increases the costs for domestic manufacturing companies, resulting in a downward revision of operating profit margins. Contrary to early-year expectations, as the war prolongs and high raw material prices persist, the KOSPI's operating profit margin is being revised downward. Researcher Na Jeong-hwan of Cape Investment & Securities stated, "If KOSPI earnings are revised downward around the Q2 earnings announcement, operating profit margins will also be further revised downward."

The reason for the slowdown in operating profit is not only high raw material prices and supply chain disruptions but fundamentally the slowdown in consumption in the final consumer country, the United States. The Michigan Consumer Sentiment Index in June was recorded at 50 points, marking an all-time low.

Korea's export growth rate is also continuing to slow. A concerning point is that the US ISM Manufacturing Index, which has a leading relationship with Korea's export indicators, is also showing a downward trend. This reflects the sluggishness of Korea's exports to China due to the Shanghai port lockdown measures in April and May.

Accordingly, caution is required in response strategies. There is abundant advice to thoroughly consider fundamentals. This is based on the judgment that sectors and stocks without earnings have strong downward pressure.

As the possibility of an economic recession by year-end increases, downward pressure on earnings forecasts is high, making the effectiveness of valuation assessments based on current earnings forecasts also lower. This means that the possibility of increased volatility (further decline) still exists.

Choi Jae-won, a researcher at Kiwoom Securities, said, "With the start of the Q2 earnings season, sectoral differentiation is expected due to companies' earnings forecast adjustments, so it is necessary to check changes in companies' earnings forecasts from mid-July and respond accordingly," adding, "Until additional changes in profit forecasts are reflected, it is necessary to adopt a defensive strategy to cope with persistent inflationary pressures and increased stock market volatility."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}

{kind=link}