FKI to Release Business Community Opinions on IFRS Submission on 24th

① Difficult to Quantify Non-Financial Information Such as Carbon Neutrality

② Bearing Risks of Information Uncertainty

③ Considerable Costs in Deriving Information Using External Agencies

"Guidelines First Rather Than Excessive Disclosure System"

[Asia Economy Reporter Moon Chaeseok] The Federation of Korean Industries (FKI) announced on the 24th that it has compiled 44 clause-specific opinions from the Korean business community on the International ESG (Environmental, Social, and Governance) disclosure standards draft and submitted them to the Korean Accounting Standards Board.

The FKI stated that after collecting review opinions on the IFRS Sustainability Disclosure Standards draft from member companies of the 'K-ESG Alliance,' it will convey these through the Accounting Standards Board to the UK International Financial Reporting Standards (IFRS) Foundation. They provided seven comprehensive opinions and 44 detailed clause-specific comments.

In March, the FKI gathered opinions from member companies on two parts of the IFRS draft: general disclosure items and climate-related disclosure items. The members raised concerns about uncertainties arising from converting non-financial information such as carbon neutrality and climate change into financial information like sales and operating profit, as well as the cumulative cost burden when all disclosure standards are met.

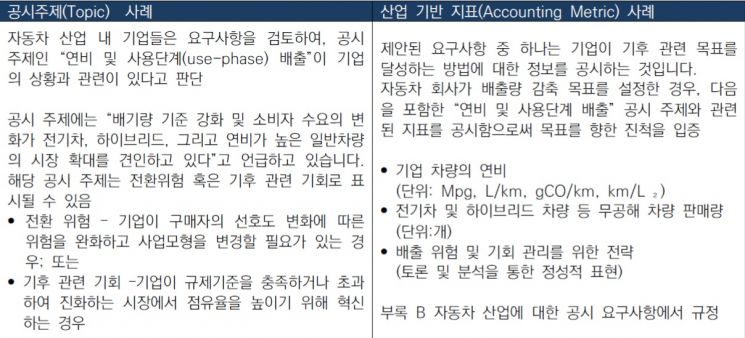

Examples of climate-related disclosures in the IFRS Sustainability Disclosure Standards draft. (Source=Federation of Korean Industries)

Examples of climate-related disclosures in the IFRS Sustainability Disclosure Standards draft. (Source=Federation of Korean Industries)

According to the IFRS draft, general disclosures require companies to disclose sustainability-related financial information focusing on four key elements: governance, strategy, risk management, and metrics and targets. Climate-related disclosures require companies to disclose information on opportunities and risk factors related to climate change and the transition to a low-carbon economy, according to industry explanations, disclosure topics, and detailed protocols.

Companies expressed concerns that it would be difficult and costly to disclose according to the IFRS draft, and if the information is incorrect, they could face criticism from shareholders and legal litigation risks. They also responded that disclosing exactly all variables arising in the process of achieving carbon neutrality according to the draft items is difficult. The draft requires clear provision of linked information between risk and opportunity information on sustainability and related financial information. Companies expressed reluctance, saying, "Qualitative descriptions are possible, but it is difficult to present quantitative figures."

As companies worry, inaccurate information disclosure could cause confusion among stakeholders. If carbon neutrality-related disclosure information calculated based on 'assumptions' is incorrect, investors will inevitably suffer losses, and companies must bear legal risks. If the disclosed items are directly linked to corporate strategy information, companies must also prepare for trade secret leaks.

Concerns were also raised about the high cost burden of producing information. Costs incurred in utilizing external institutions or building internal systems fall on the companies. There was also an opinion that requiring companies obligated to prepare consolidated financial statements to use consolidated standards for sustainability disclosure information is excessive. Especially, small subsidiaries and overseas affiliates find it difficult to prepare consolidated data, and it requires significant manpower and costs. Overseas subsidiaries may face differences in regulations by country, and disclosure errors may occur. The consensus is that applying the disclosure standards uniformly to overseas affiliates at the same time is unreasonable.

Typically, sustainability management reports disclose finalized results from the previous year in June. However, if sustainability information must be disclosed together with financial statements around the end of February, the workload due to timing differences is expected to increase. It is also difficult to provide accurate information for items not finalized at that time. There was also an opinion that if the IFRS sustainability disclosure standards are applied to the Korean market, existing ESG disclosure obligations such as the 'Sustainability Management Report' should be abolished or their functions merged. Disclosing financial statements and sustainability information simultaneously would be too burdensome.

Lee Sang-yoon, Head of Communications at the FKI, argued, "The timing of applying IFRS sustainability disclosure standards should be comprehensively considered along with Korea’s accounting standards, business conditions, and domestic disclosure systems." He emphasized, "Excessive sustainability information disclosure makes it difficult to guarantee reliability and may prevent information users from utilizing it effectively, so guidelines reflecting the opinions of business communities from various countries should be actively presented."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}