[Asia Economy Reporter Lee Seon-ae] Automotive, Cosmetics, Energy, Machinery 'Clear' VS Chemicals, Steel, Display, Healthcare, Electronics 'Cloudy'

Movements to identify industries supported by second-half performance through export and trade balance indicators are gaining momentum. In a market flow with high uncertainty, sector differentiation based on performance is expected to become clearer, aiming to devise investment response strategies. Although not everything can be judged solely by exports and trade balance, experts believe these indicators have shown similar trends to industry (company) performance so far and can provide about a one-month advance view, making them useful for current investment strategy formulation.

According to the Korea Customs Service and the financial investment industry on the 22nd, Korea's export value from January to May increased by 17.8% compared to the same period last year, showing a favorable trend, but the provisional tally for June 1-20 shows a 3.4% decrease. The trade balance, which recorded deficits in April and May, is also expected to show a deficit this month (based on provisional tally up to the 20th). The Korea International Trade Association forecasts this year's export value to increase by 9.2% year-on-year to $703.9 billion, with a trade deficit of $14.7 billion. Accordingly, the fortunes of industries based on exports and trade balance are expected to diverge sharply. In particular, the decrease in export value of wireless communication devices and automotive parts based on the June provisional tally is expected to impact sector profitability.

Monthly export performance is announced on the 1st of the following month (item/type data on the 15th), and corporate earnings are announced in the next quarter (within 45 days). Exports tend to show a flow similar to corporate sales, and trade balance resembles corporate operating profit. Researcher Lim Hye-yoon of Hanwha Investment & Securities said, "Since various factors affect performance, it is impossible to judge everything solely by export data, but performance trend changes are similar to export trends, and if the flow can be grasped about a month earlier, it has value," adding, "If export data can be used to somewhat predict performance, faster investment decisions are possible."

Based on export data, sales in the automotive, energy, machinery, electrical products, and cosmetics sectors are likely to continue increasing. Conversely, the rapidly increasing sales in chemicals and steel may have passed their peak (peak-out). Sales in display, healthcare, and electronics sectors should be considered likely to decline.

The trade balance for automobiles, petroleum products, and machinery shows an upward trend. Cosmetics and automotive parts are rebounding after bottoming out. Chemicals, steel, and wireless communication devices have passed their peaks. Display and pharmaceuticals are on a declining trend. Accordingly, automotive, energy, machinery, and cosmetics sectors have a high possibility of performance improvement. Semiconductor rebound signals are weak. On the other hand, chemicals, steel, and electronics require lowered expectations for further performance improvement. Display and healthcare performance may be somewhat sluggish.

In conclusion, automotive, energy, machinery, and cosmetics can be classified as sectors expected to show favorable performance as both trade balance and exports are steadily increasing. These are also sectors that securities firms expect to see simultaneous profit and sales improvement in the fourth quarter. Semiconductor, automotive parts, and electrical products (batteries) are also expected to improve performance but have slightly weaker signals compared to the above sectors. Conversely, chemicals and steel should consider performance peaks, and a conservative approach is needed for display, healthcare, and electronics.

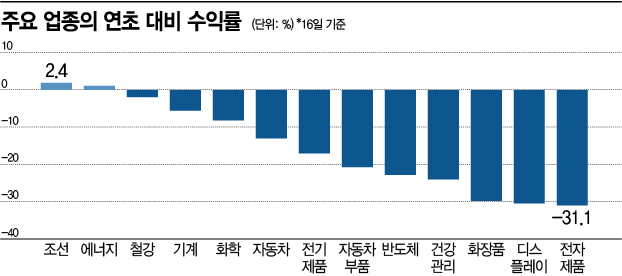

When aggregating the returns of major sectors compared to the beginning of the year, sectors that have fallen more than the KOSPI include automotive parts, semiconductors, healthcare, cosmetics, display, and electronics. Steel, machinery, chemicals, automobiles, and electrical products also show negative returns. Only shipbuilding and energy performed well. Researcher Lim said, "Considering the excessive price drops from a stock price perspective, automotive and cosmetics have high attractiveness," adding, "Energy and machinery also have a high possibility of further rebound supported by performance, while display, healthcare, and electronics have merit from an excessive drop perspective, but if performance is poor, rebounds will be limited."

However, since each industry is influenced by various factors such as price importance in some sectors and volume importance in others, variables related to these should also be considered. Researcher Kim Soo-yeon of Hanwha Investment & Securities said, "Looking at various indicators that can gauge the business environment will help decide how to compose a portfolio," adding, "In cyclical sectors like materials and energy, price is important, but margins in chemicals and steel excluding refining seem to be declining, and orders for industrial goods and shipping freight rates are also observed to have passed their peaks." She continued, "Growth sectors like healthcare and communication services value scalability, and especially domestic cultural service exports related to communication services are noteworthy as they continue to show trend growth."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}