US Department of Agriculture Raises Global Soybean New Crop Production Forecast

Wheat Supply Expected to Remain Tight Even in Ending Stocks

"Recommend DBA ETF Over JJG ETN"

"Also Recommend TIGER Agricultural Futures Enhanced (H)"

[Asia Economy Reporter Hwang Yoon-joo] Amid the global spread of the edible oil crisis, an analysis has emerged that the supply and demand of wheat (somak) is more concerning than that of corn and soybeans. Accordingly, it is evaluated that investing in broad agricultural products is more advantageous than investing in specific crops such as corn, soybeans, and wheat.

Hwang Byung-jin, a researcher at NH Investment & Securities, forecasted on the 15th, "ETNs investing only in grains like JJG (which invests in the three crops: corn, soybeans, and wheat) will perform less favorably compared to ETFs like DBA (which tracks the futures contract index of 10 agricultural products) and TIGER Agricultural Futures Enhanced (H), which are exposed to the agricultural sector as a whole."

According to the May World Agricultural Supply and Demand Estimates (WASDE) released by the U.S. Department of Agriculture (USDA), wheat prices surged about 6% due to lower-than-expected production estimates. The Russia-Ukraine conflict and last year's poor winter wheat crop in the U.S. influenced this.

Due to the spillover effect from the strong wheat prices (where a specific phenomenon affects another), corn and soybean prices also closed with firm gains.

However, despite delayed planting in April caused by rainfall in the U.S. Midwest, the outlook for new crop (harvested in the current year, 2022/23 marketing year) soybean production expansion outweighed the tight supply situation of old crop (harvested last year, 2021/22 marketing year). The USDA also expects short-term improvement in soybean supply and demand. In the May WASDE, both U.S. and global new crop soybean production forecasts were revised upward.

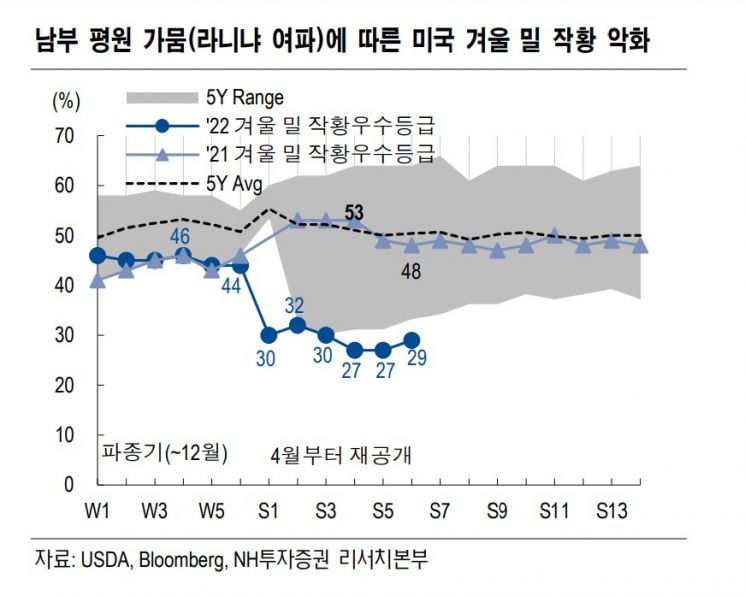

However, the wheat supply and demand outlook is not favorable. Researcher Hwang stated, "Despite the downward revision of the U.S. wheat ending stocks forecast due to poor winter crop conditions, the tight supply level is expected to persist through the 2022/23 marketing year, even with anticipated new crop production increases from expanded planting areas this year."

He pointed out, "The downward revision of global new crop production estimates due to the Russia-Ukraine conflict also signals a tight wheat supply situation in global ending stocks."

Previously, NH Investment & Securities upgraded its short-term (3 months) agricultural investment opinion to 'Overweight.' This is because if the weather issues in the U.S. Midwest that caused delayed planting in April ease as recently, concerns about accelerated planting in corn and soybeans are expected to emerge as variables that control further price increases.

Researcher Hwang diagnosed, "In the case of wheat, the proportion of U.S. winter wheat crop rated Good or Excellent, which is harvested in July-August, is significantly below the level of the same period last year, raising the possibility of downward revisions to production estimates in the June WASDE."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}