[Y-nomics Must-Know] ② Pension Reform

Experts Suggest "Expanding Mandatory Enrollment to Increase National Pension Participation" and Propose Singapore-Style Individual Account Savings Alternative

[Asia Economy Sejong=Reporter Kim Hyewon] The Yoon Seok-yeol administration is showing strong determination to reform the public pension system, which has repeatedly failed under previous administrations. The primary focus is whether they can start by addressing the National Pension, which has been fixed at a 9% contribution rate for 24 years. It is also crucial to see if discussions on integrating the four major public pensions?including the civil servant pension and military pension, which have been running deficits covered by taxpayers for decades?can take their first steps. Experts point out that structural and parametric reforms of public pensions must no longer be delayed to reduce the burden on future generations amid worsening low birth rates and aging population.

According to related ministries on the 11th, the new government plans to raise the contribution rate and adjust the payout rate and income replacement rate to establish a “proper burden-proper benefit” system for the National Pension. Currently, the National Pension contribution rate has been frozen at 9% since 1998, for 24 years. The income replacement rate stands at 40%.

The government is considering changing these rates because the National Pension’s financial status is deteriorating. Switching to a pension system where people “pay more and receive less” can delay the depletion of the fund.

According to an analysis by the National Assembly Budget Office on the National Pension finances from 2019 to 2060 under various scenarios, increasing the contribution rate by 1 percentage point delays the depletion of reserves by 2 to 4 years, while raising the income replacement rate by 5 percentage points accelerates the depletion by 1 to 2 years. There is now a consensus that it is time to raise the contribution rate to an appropriate level. Oh Geon-ho, policy committee chairman of the Welfare State We Make, proposed raising the contribution rate to 12% while maintaining the 40% income replacement rate, indicating an implicit agreement among experts to increase it into the 10% range.

The government and the National Assembly currently expect the National Pension fund to be depleted around 2055. The government conducts financial calculations every five years based on the National Pension Act to review pension finances, and the depletion date has been moving closer each time. The fifth financial calculation is scheduled to be released in 2023 but could be expedited depending on the Yoon administration’s pension reform will. The new government has already announced plans to gradually raise the basic pension from the current 300,000 won to 400,000 won to alleviate elderly poverty in the present generation alongside pension reform.

The government, led by Statistics Korea, has also launched the country’s first comprehensive pension statistics project. Until now, various pension statistics were scattered separately, and there was no integrated figure. This will be used to examine whether “Korean elderly are truly poor compared to other OECD countries” and serve as a basis for pension reform.

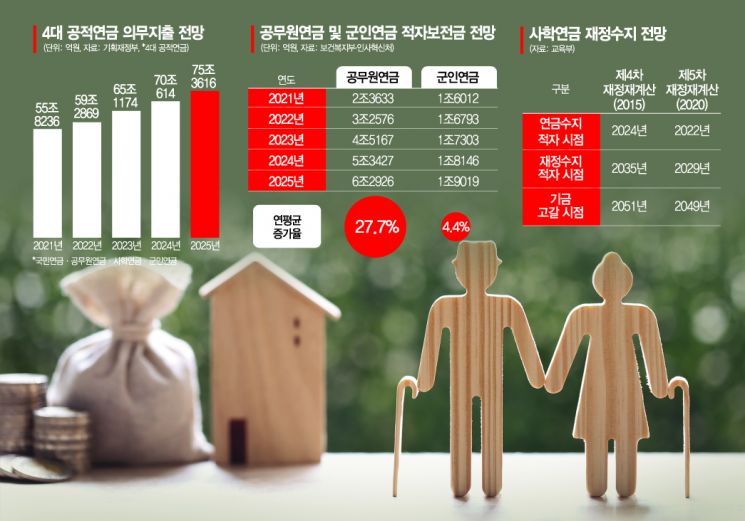

The National Pension is relatively better off. The finances of other public pensions such as the civil servant pension, military pension, and private school teachers’ pension, which are chronically in deficit or on the verge of deficit, are worse and rely heavily on the “government wallet.” Of the government’s mandatory expenditure budget of 301.1 trillion won this year, 140.1 trillion won (a 6.7% increase from the previous year) is allocated to welfare expenditures responding to low birth rates and aging society, with nearly 60 trillion won (42.3%) going to the four major public pensions. The Ministry of Economy and Finance projects that this expenditure will increase by an average of 7.8% annually and exceed 70 trillion won within two years.

As with previous administrations including the Moon Jae-in government, there is skepticism about the success of pension reform due to intense social conflicts among stakeholders. Nevertheless, experts say that the success or failure depends on the government’s decisiveness to maintain the current system framework in the short term while adjusting key variables such as the contribution rate, as well as laying the groundwork for structural reforms of pensions in the mid to long term.

Lee Taeseok, head of the Population Structure Response Research Team at the Korea Development Institute (KDI), said, “The first step in the difficult pension reform, like ‘putting a bell on a cat’s neck,’ must start by increasing the National Pension enrollment rate for all citizens.” He added, “The basic framework for retirement income using pensions should apply equally to both the National Pension and the Basic Pension, while job-specific characteristics (such as civil servants, teachers, and military personnel) should be covered by retirement pensions to allow diversity.” He argued that to increase National Pension enrollment, mandatory coverage should be expanded to include self-employed workers and others.

There are also opinions that instead of focusing solely on parametric reforms, it is necessary to actively review foreign models and change the system itself. Kim Jinyoung, professor of economics at Korea University, pointed out, “Discussions to solve the National Pension financial problem caused by population aging focus on raising contributions and reducing payouts, but economic research shows that countries with larger National Pension systems tend to have lower birth rates.” He explained, “Since pensions replace family support systems, the larger the pension, the fewer births there are, which can lead to a vicious cycle of worsening finances.” Professor Kim suggested a personal account accumulation system like Singapore’s as an alternative.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}