Last Year, Interest Rates Raised to Suppress Loan Demand

Structural Phenomena During Interest Rate Hikes Also a Cause

[Asia Economy Reporter Sim Nayoung] The representative profitability indicator for banks, NIM (Net Interest Margin), is most significantly influenced by the loan-deposit interest rate spread (loan interest rate - deposit interest rate).

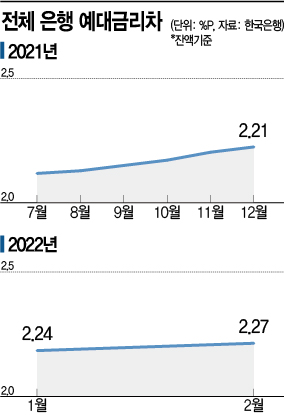

According to the Bank of Korea's Economic Statistics System on the 6th, the domestic banks' loan-deposit interest rate spread based on balances (as of the end of February) was 2.27 percentage points. Since the Bank of Korea began raising the base interest rate in July last year (2.11 percentage points), the loan-deposit interest rate spread has been increasing every month. This is also why banks' NIM is expected to be high through the first quarter of this year.

According to Korea Investment & Securities, the banks' NIM in the first quarter is estimated to have risen by 4 basis points (1bp = 0.01 percentage points) compared to the previous quarter. This follows a 5bp increase in the fourth quarter of last year, indicating further improvement. Net interest margin is a figure that represents the profitability of financial institutions, calculated by dividing the difference between income generated from asset management and funding costs by the total amount of managed assets.

The financial sector cites government policies and the characteristics of lending and deposit activities during periods of rising interest rates as reasons for the widening loan-deposit interest rate spread. Last year, the Financial Services Commission limited banks to increasing household loans by only 4-5% compared to the previous year, which forced banks to reluctantly raise loan interest rates. To comply with the household loan volume regulation, banks had to turn away borrowers by raising interest rates.

Another reason for the expansion of the loan-deposit interest rate spread is that those who took out loans with variable interest rates during the rising rate period now face significantly higher rates. A representative from a commercial bank explained, "Mortgage loans are long-term loans spanning decades, and the benchmark interest rate indicators have been rising, so this year's rates are higher than last year's. In the case of unsecured loans, when extended, higher rates than before are applied, causing the overall loan interest rates in the banking sector to rise quickly."

Regarding deposit interest rates, it was said, "During periods of rising interest rates, people tend to flock to short-term deposits expecting rates to rise further. Since short-term interest rates are lower than long-term rates, deposit interest rates are rising relatively slowly." A Financial Services Commission official also stated, "The recent widening of the loan-deposit interest rate spread is structurally influenced by the rising interest rate environment."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)