[Asia Economy Reporter Changhwan Lee] It has been revealed that the outstanding loan receivables of insurance companies significantly increased at the end of last year. This is analyzed to be due to the increase in insurance company loans, centered on insurance policy loans, as financial authorities tightened bank loans to reduce household debt.

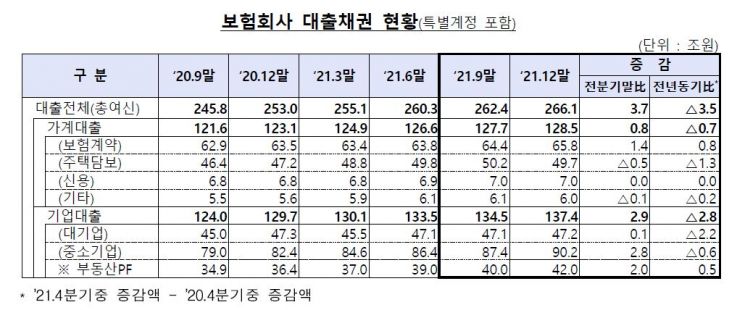

The Financial Supervisory Service announced on the 6th that as of the end of December last year, the outstanding loan receivables of insurance companies amounted to 266.1 trillion KRW, an increase of 3.7 trillion KRW compared to the previous quarter.

Among the total loan receivables, the balance of household loans was 128.5 trillion KRW, an increase of 800 billion KRW compared to the previous quarter. Compared to 123.1 trillion KRW at the end of 2020, it increased by about 5.4 trillion KRW.

Insurance policy loans increased by about 1.4 trillion KRW to 65.8 trillion KRW compared to the previous quarter. During the same period, mortgage loans decreased by about 500 billion KRW to 49.7 trillion KRW.

As financial authorities strengthened loan regulations mainly on banks to reduce household loans starting last year, it is analyzed that insurance companies’ contract-backed loans, which are relatively less regulated, increased.

As of the end of last year, corporate loan receivables amounted to 137.4 trillion KRW, an increase of 2.9 trillion KRW compared to the end of the previous quarter. Loans to small and medium-sized enterprises amounted to 90.2 trillion KRW, an increase of 2.8 trillion KRW compared to the previous quarter.

The delinquency rate was favorable. As of the end of last year, the delinquency rate on insurance companies’ loan receivables was 0.13%, down 0.01 percentage points from the end of the previous quarter. The delinquency rates for both household and corporate loans improved. The non-performing loan ratio rose by 0.01 percentage points to 0.13% compared to the end of the previous quarter.

A Financial Supervisory Service official said, "We will continuously monitor the loan soundness indicators such as the delinquency rate of insurance companies in preparation for increased volatility in market indicators such as interest rates and exchange rates," adding, "We will encourage strengthening loss absorption capacity through sufficient provisioning for loan losses (including reserves), considering the deterioration of borrowers’ principal and interest repayment ability when interest rates rise."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}