President-elect Yoon Suk-yeol has announced a pledge to supply 2.5 million housing units, with 1.5 million units allocated to the Seoul metropolitan area. It is expected that the next government will promptly establish a housing supply roadmap upon its inauguration. At the same time, real estate tax and financial regulations are also likely to be eased. The construction and real estate industries are buoyed by expectations of direct benefits. Stock prices of interior and building materials companies are also fluctuating. Asia Economy analyzed LX Hausys and Sammok S-Form, leading building materials companies.

[Asia Economy Reporter Park So-yeon] Ahead of the launch of the next government, which has pledged to ease reconstruction regulations and expand housing supply, LX Hausys, a building materials and interior company, is also gaining attention. LX Hausys was established in 2009 following the spin-off of LG Chem’s industrial materials division. The company produces and supplies building materials such as windows, flooring, and artificial marble, as well as automotive parts and fabrics, and surface materials for interiors and home appliances. It operates not only domestically but also in key markets including China, North America, and Europe.

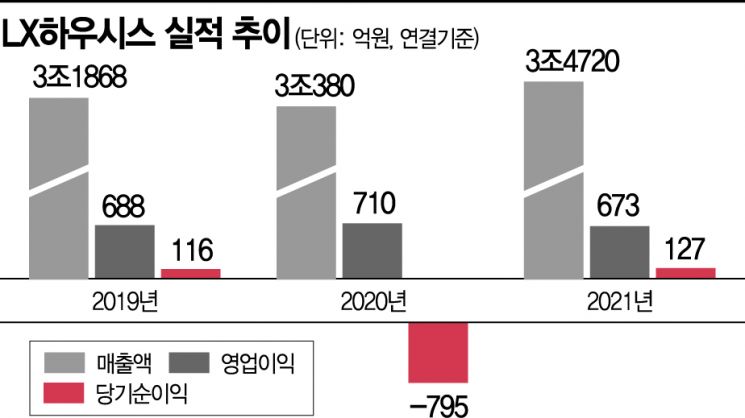

Last year, LX Hausys recorded its highest-ever consolidated sales of 3.472 trillion KRW. This growth was driven by an increase in housing move-in volumes due to rising housing sales and recent aggressive expansion of B2C (business-to-consumer) dealerships. In the case of artificial marble, a surface material, it accounts for 20% of the North American market demand, and sales continue to increase amid a surge in U.S. housing demand.

For decorative materials (flooring, sheets, wallpaper, flooring), sales growth is expected in LX Hausys’ core product, the high-margin insulation PF board (phenolic foam). This is due to the expansion of applicable buildings following the November 2019 revision of the Building Act, which strengthened standards for semi-noncombustible (fire-resistant) insulation materials.

The insulation plant No. 4, expanded through a 120 billion KRW facility investment by LX Hausys, was completed in March and is expected to see a significant increase in operating rates in the second half of the year. When fully operational, total production is estimated at around 300 billion KRW. Analyst Kim Se-ryeon of eBest Investment & Securities forecasted, "Profit growth is expected due to the expansion of high-margin products."

The building materials sector is expected to continue growing by strengthening its approach to the B2C interior remodeling market. LX Hausys established a kitchen and bathroom division in the second half of last year and is aiming to package products extending from its existing focus on windows and flooring to bathrooms and kitchens. The number of flagship stores, a concept of direct retail stores, is expected to double from 20 to about 40, and sales channels will be further strengthened. This improved accessibility to consumers is anticipated to drive performance growth.

Last year recorded highest-ever sales of 3.472 trillion KRW

Insulation Plant No. 4 to see increased operating rates in second half

Profit growth expected from expansion of high-margin products

However, recent sharp price increases in raw materials such as PVC (polyvinyl chloride) and MMA (methyl methacrylate) are acting as negative factors for profits. The average annual price of PVC rose about 60% compared to the previous year, and rapid price fluctuations of key raw materials are expected to be variables affecting future performance.

LX Hausys has consistently recorded consolidated sales exceeding 3 trillion KRW since 2017. Operating profit was around 140 billion KRW until 2017 but sharply declined to 60 to 70 billion KRW from 2018. This was due to sluggishness in upstream industries such as domestic construction and automobile sales, rising raw material prices, and exchange rate fluctuations. Interest-bearing debt peaked at about 1.2 trillion KRW at the end of 2018 but decreased to below 1 trillion KRW by the end of 2020.

Meanwhile, following the spin-off of LG Group and LX Group, LX Hausys, along with five affiliates including LX International, LX Semicon, LX MMA, and LX Pantos, established an independent management system under the new LX Group umbrella in May last year. In this process, a shareholding structure was created linking Chairman Koo Bon-joon of LX Group → LX Holdings → Hausys, International, Semicon, MMA → Pantos.

Since joining LX Group, the affiliates have focused on establishing efficient business structures to create new growth engines and synergies. Among them, stable glass procurement through LX International’s acquisition of a stake in Korea Glass Industry is expected to be a positive factor for LX Hausys.

Korea Glass Industry is the second-largest domestic flat glass manufacturer, widely known under the brand ‘Hanglas.’ If LX International completes the acquisition after thorough due diligence, LX Hausys will be able to counter its industry rival KCC. KCC competes with Hanglas in the flat glass market and with LX Hausys in building materials such as windows and flooring.

Due to this competitive structure, LX Hausys has not sourced flat glass from KCC. Industry insiders expect that the Hanglas acquisition led by LX International will play a significant role in strengthening LX Hausys’ competitiveness following the failed acquisition of Hanssem. Market interest also focuses on whether the company will reattempt to sell its automotive materials and industrial film division, which has recorded losses for several years.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}