New Delinquencies Remain Steady, but Delinquent Bonds Significantly Cleared

[Asia Economy Reporter Minwoo Lee] As of the end of last year, the delinquency rate on won-denominated loans at domestic banks recorded the lowest level ever. Analysts predict that the record-breaking performance streak will continue this year as the burden of provisions is not significant.

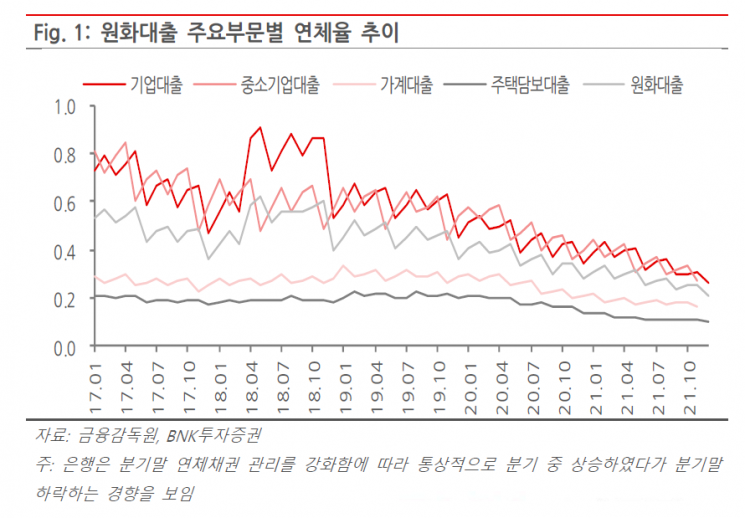

According to the "Status of Won-Denominated Loan Delinquency Rates at Domestic Banks as of December 2021 (Preliminary)" announced by the Financial Supervisory Service on the 24th, the delinquency rate on won-denominated loans (based on principal and interest overdue for more than one month) at domestic banks was 0.21% at the end of last year, down 0.04 percentage points (p) from the previous month and 0.06 p from the same month last year. This corresponds to the lowest level ever recorded.

Specifically, the delinquency rate for corporate loans was 0.26%, down 0.05 p from the previous month and 0.08 p from the same month last year. The delinquency rate for large corporate loans was 0.24%, similar to the previous month, but down 0.03 p compared to the same month last year. The delinquency rate for small and medium-sized enterprise (SME) loans was 0.27%, down 0.06 p from the previous month and 0.09 p from the same month last year. The delinquency rate for individual business owner loans was 0.16%, down 0.04 p during the same period, also at the lowest level.

The decline in delinquency rates is attributed to the fact that new delinquencies amounted to 900 billion KRW, similar to the previous month, while the amount of delinquent loans resolved was 1.7 trillion KRW. As a result, the balance of delinquent loans decreased by about 800 billion KRW to 4.4 trillion KRW compared to the previous month.

Following the record-breaking performance last year, the banking sector is expected to continue its strong performance this year. Kim In, a researcher at BNK Investment & Securities, said, "Despite market concerns, most of the principal and interest repayment deferrals for SMEs and self-employed individuals are government-guaranteed or collateralized loans. Considering that conservative provisions related to COVID-19 amounting to 2 trillion KRW were set aside in 2020 and another 1 trillion KRW last year, the additional burden of provisions is expected to be minimal." He added, "Historically strong asset soundness also suggests that, following last year, the burden of loan loss provisions will not be significant this year, and with a sharp increase in interest income, listed banks are expected to continue achieving record-high performance."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}