Leading Liquor Companies in Bu-Ul-Gyeong

Dividends and Share Buybacks Despite Losses

Efforts to Enhance Shareholder Value

Increase in Alcohol Price Boosts Expectations

Domestic liquor companies are struggling amid the saturation caused by COVID-19. Recently, the burden of costs has increased due to rising prices. They have no choice but to raise product prices even if it means accepting a decrease in sales volume. HiteJinro has decided to raise the wholesale price of soju products by 7.9% starting from the 23rd. This is the first price increase in about three years, reflecting the rise in raw material costs, logistics fees, and bottle handling fees. Other soju companies are expected to follow suit with price hikes. Makgeolli prices have already risen more sharply than soju. Kooksoondang raised product prices by between 9.9% and 25% at the end of last year. Can liquor companies catch the two rabbits of sales and profitability through price increases? Asia Economy reviews the business and financial status of Muhak and Kooksoondang and examines their future growth potential.

[Asia Economy Reporter Jang Hyowon] Muhak, a leading soju manufacturer in the Gyeongnam region, purchased treasury shares last year to enhance shareholder value amid the COVID-19 downturn and has decided to pay dividends despite posting a loss. The poor performance last year is expected to recover this year if soju prices are raised following an increase in the price of ethanol.

Expectations for Soju Price Increase ‘Rising’

Muhak is a representative liquor manufacturer in Busan, Gyeongnam, and Ulsan. Its main products include diluted soju such as ‘Ttak! Joheundei’ and ‘White Soju.’ Through regionally focused management, it maintains a high market share in the southeastern region and also exports to countries like the United States and Japan.

Muhak recorded somewhat sluggish performance last year. According to the Financial Supervisory Service’s electronic disclosure, Muhak’s consolidated sales for last year were tentatively estimated at 126.9 billion KRW, down 8.9% from the previous year. Operating profit turned to a loss of 890 million KRW compared to the previous year.

The company stated that social distancing measures due to COVID-19 led to a decrease in liquor sales, and combined with rising cost ratios, resulted in operating losses. In fact, as of the end of the third quarter last year, sales decreased by about 12% compared to the same period the previous year, while cost of sales only decreased by 3%.

Additionally, the price of ethanol, the raw material for soju, was slightly increased in June last year. 99.3% of the raw materials Muhak purchases are ethanol. Ethanol is mostly purchased from Daehan Ethanol Sales, a dedicated sales company established by ten domestic ethanol manufacturers with equity participation. Daehan Ethanol Sales raised the price of both fermented and refined ethanol by 0.3% in June last year.

Although raw material prices rose, the price of soju remained the same at 974.37 KRW per unit for ‘Ttak! Joheundei’ in 2020. This is because prices cannot be freely raised in the fiercely competitive soju market. However, price increases are expected this year. On the 7th, Daehan Ethanol Sales raised ethanol prices by 7.6%, making a soju price increase inevitable. In fact, HiteJinro, the number one soju company, announced a 7.9% increase in soju product wholesale prices.

Muhak also recorded a net loss of 16.5 billion KRW last year, turning from a net profit of 13.2 billion KRW in 2020. The net loss was larger than the operating loss due to equity-linked securities (ELS) invested by Muhak. As of the end of the third quarter last year, Muhak had invested 291 billion KRW in ELS products, with an evaluation loss of 28.3 billion KRW.

A Muhak official explained, "At the time of settlement, the stock market was depressed, lowering the ELS evaluation amount. However, since the invested ELS has not entered the knock-in barrier (principal loss zone), no disposal loss has been reflected, so if the stock market recovers, it will turn into an evaluation gain." He added, "It is not an actual cash outflow loss."

Treasury Share Buybacks Reduce Circulating Shares

Despite the difficult situation last year, Muhak decided to pay dividends. On the 11th, Muhak announced a cash dividend of 230 KRW per share. The dividend yield is 2.74%, with a total dividend amount of about 6.1 billion KRW. This is the first dividend in three years since 2018.

The reason dividends could be decided despite losses is analyzed to be due to the company’s large retained earnings. As of the end of the third quarter last year, Muhak’s retained earnings were 486.4 billion KRW. These are surplus funds accumulated from past annual net profits in the hundreds of billions of KRW. In 2018, dividends were also paid despite net losses due to shareholder demands.

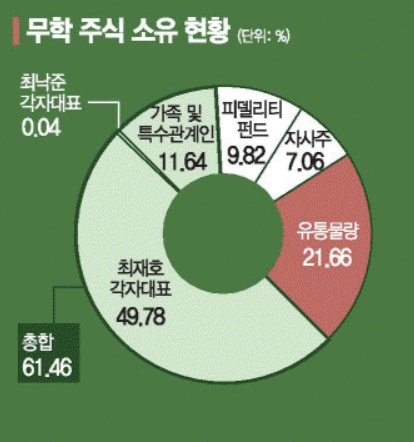

Additionally, Muhak continues to buy back treasury shares. At the end of last year, it acquired an additional 700,000 treasury shares, currently holding 2,013,132 shares (7.06%) as treasury stock. Muhak has conducted treasury share buybacks every year except from 2015 to 2018.

Continuous treasury share buybacks have also reduced circulating shares. As of the end of the third quarter last year, Chairman Choi Jae-ho, the largest shareholder of Muhak, and related parties held 61.46% of shares. Long-term investor Fidelity Fund holds 9.82%. Excluding treasury shares, circulating shares are about 21.66%.

A Muhak official said, "We decided on dividends this year to enhance shareholder value. We are steadily acquiring treasury shares, but the specific method of disposal has not been determined yet."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}