[Asia Economy Reporter Ji Yeon-jin] The Financial Supervisory Service (FSS) will closely examine the status of ESG (Environmental, Social, Governance) bonds and stock option grants in the business reports of domestic listed companies submitted by the end of next month.

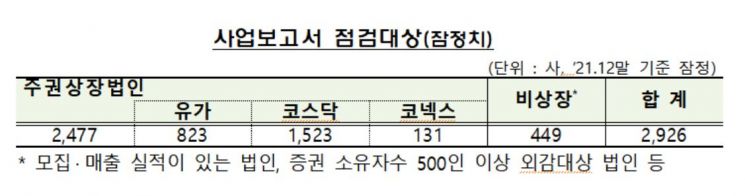

On the 17th, the FSS announced in advance the key inspection items for business reports to be reviewed this year. The FSS plans to verify these inspection items for a total of 2,926 companies subject to business report submission, including those with December fiscal year-end.

First, as corporate social responsibility management has recently been emphasized, investor interest in ESG bonds has increased. Therefore, the FSS will inspect the issuance status of ESG bonds, detailed usage of raised funds, reasons for any discrepancies between the initial purpose of fund use and actual usage, among other aspects. Additionally, the grant and exercise details of stock options, the current status of unexercised stock options, and compliance with preparation standards will also be reviewed.

Regarding financial matters, the FSS will focus on 11 items, including four key points such as ▲the format of summarized financial information, ▲whether notes on mergers, splits, and restatement of financial statements are included, ▲disclosure of inventory status, and ▲disclosure of allowance for doubtful accounts.

In particular, since there have been many cases of misrecording auditor names in the main text of business reports or omitting key audit matters, the FSS will check ▲whether the name of the accounting auditor and audit opinion are recorded, ▲disclosure of audit fees and hours, ▲whether discussions between internal audit bodies and auditors are documented, ▲disclosure of discrepancies between current and previous financial statements and contents of adjustment meetings, and ▲for listed companies, the number of key audit matters selected and whether they are recorded in the main text.

The FSS will also focus on whether external audit and review opinions on internal accounting control systems are recorded, and whether review, operation, and audit reports on internal accounting control systems are submitted.

Furthermore, regarding mergers, the FSS will inspect whether details such as counterparties and contract contents for each case, as well as comparisons between forecasted and actual major financial items before and after mergers, are disclosed. It will also examine compliance with preparation standards for employee status and remuneration, the completeness of disclosures on employees with remuneration exceeding 500 million KRW, and compliance with standards for reporting acquisition and disposal of treasury stock, including whether reasons for non-fulfillment are stated if acquisition/disposal execution rates are below 50%.

The FSS will also review disclosures related to special listing status, comparisons of forecasted and actual financial figures for the past three fiscal years, management of unused funds among direct financing, and whether exemptions from designation as a management item are noted.

To help investors easily understand business reports, the FSS will check whether the revised formats have been followed as the form layout has been improved. This includes whether summary information is provided at the introduction when describing business content, whether summary tables are used for voluminous tables such as affiliate status, and whether mandatory table preparation items are recorded.

The FSS stated, "If any deficiencies in disclosures are found during the inspection, individual notifications will be sent to companies and auditors by May to guide voluntary corrections. If important deficiencies such as repeated failure to comply with corporate disclosure form preparation standards occur, strict warnings will be issued, and if necessary, this will be considered when selecting financial statements for review."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}