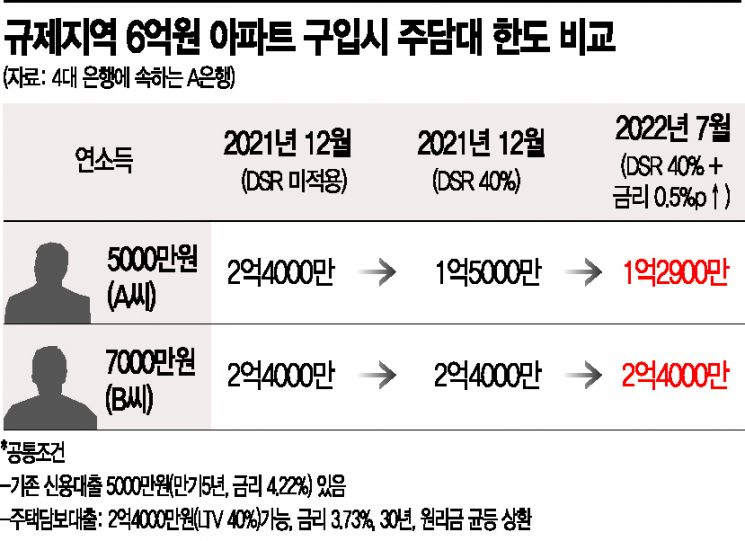

Mortgage Loan Limits When Buying a 600 Million KRW Apartment:

Comparison Between Employee A with an Annual Salary of 50 Million KRW and Employee B with an Annual Salary of 70 Million KRW

A: 240 million KRW → 129 million KRW

B: 240 million KRW unchanged

Loan regulations combined with rising interest rates

Lower income earners face greater disadvantages

Exacerbating polarization side effects

"Regulations should be reformed to allow more loans if there is income and repayment ability"

[Asia Economy Reporter Shim Nayoung] It has been revealed that employees with lower annual salaries suffer more from stringent loan regulations and soaring interest rates. Since January, financial authorities have tightened the Debt Service Ratio (DSR) regulations. The intention was to control household loans under the principle of "borrow only what you can repay." The problem is that combined with the current interest rate hike, these loan regulations may have the side effect of exacerbating polarization.

On the 10th, Asia Economy, together with a commercial bank, analyzed the mortgage loan amounts that employee A, earning 50 million KRW annually, and employee B, earning 70 million KRW annually, could receive when buying a 600 million KRW apartment at different times (see table). As a result, compared to December last year, A’s loan limit dropped by half by July this year. Meanwhile, B’s loan amount remained unchanged. Until the end of last year, their limits were the same, but only A, with the lower salary, moved further away from the dream of homeownership within six months.

The simulation reflected current borrowing behaviors of employees by assuming both had already taken out 50 million KRW in unsecured loans. The same mortgage loan conditions were applied. Based on this premise, the comparison periods for mortgage loan limits were set as December last year (no borrower-level DSR regulation applied) → January this year (DSR 40% for total loans exceeding 200 million KRW) → July (DSR 40% for loans exceeding 100 million KRW, with a 0.5 percentage point interest rate increase).

A’s loan limit fell from 240 million KRW → 150 million KRW → 129 million KRW. In contrast, B could borrow up to 240 million KRW throughout this period. The borrowing capacity of lower-income A significantly decreased. A commercial bank official explained, "A can only borrow within a 20 million KRW annual principal and interest repayment limit, and as interest rates rise, the loan limit decreases. B’s annual repayment amount is 28 million KRW, so he can absorb regulatory and interest shocks, making it much easier to buy a home."

If the housing price rise phase returns in the future, the asset gap between B, who could buy a house with a loan, and A, who could not, will inevitably widen. Professor Sung Tae-yoon of Yonsei University’s Department of Economics said, "If there is income and repayment ability, the DSR regulation should be reformed to allow increased borrowing."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}