2021 Started and Ended with Debt

Household Debt Increased by 117 Trillion Won in 9 Months This Year

Despite Successive High-Intensity Loan Regulations, Resulted in Balloon Effect and Interest Bomb

Frozen Money Flow Continues Next Year... Including Card Loans and Savings Banks

[Asia Economy Reporters Sunmi Park and Kiho Sung] It was a year that started and ended with debt. As the prolonged COVID-19 pandemic forced households and businesses to survive by borrowing money, household debt surged sharply this year, and financial authorities unleashed unprecedentedly stringent regulations to curb the snowballing household debt. With the lending window rapidly closing in the second half of the year due to regulatory orders, genuine borrowers faced a credit cliff, and vulnerable groups who could not cross the threshold of formal financial institutions turned to illegal private loans. To make matters worse, as the base interest rate hikes took full effect, not only the common people who borrowed to cover housing and living expenses but also borrowers who excessively took out loans amid last year's "Yeongkkeul" (pulling together all resources) and "Debt Investment" (borrowing to invest) frenzy began to face the reality of interest burdens. The counterattack of debt had begun.

Both Households and Businesses Survived by Borrowing

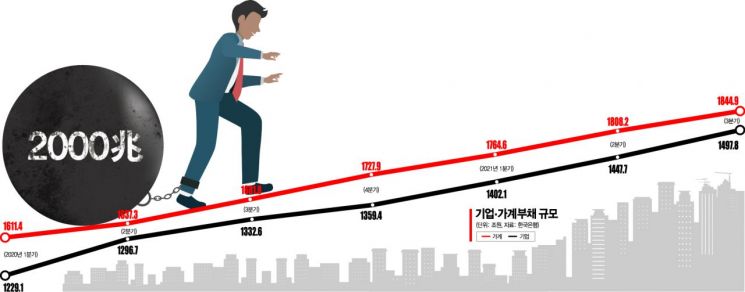

According to the Bank of Korea and financial authorities on the 29th, the outstanding household debt (household credit) from January to September this year was 1,844.9 trillion won, a 9.7% increase compared to the same period last year when COVID-19 broke out. The scale of household debt has surpassed last year's South Korea's real Gross Domestic Product (GDP) of 1,836 trillion won. The household debt increased by 117 trillion won in just nine months this year, a figure similar to last year's total increase of 127 trillion won.

Over the past two years of the COVID-19 pandemic, the accumulated increase in household debt reached 244 trillion won. The household debt-to-disposable income ratio rose to 174.1%, up 5 percentage points from 169.1% at the end of last year.

Last year, the net increase in household debt set record highs every month. This year, household loans also started with a sharp increase from January. The effects of COVID-19 and the Yeongkkeul and Debt Investment frenzy continued into early this year. The difference is that financial authorities introduced strong loan regulations one after another to curb Yeongkkeul and Debt Investment, which slowed the growth rate from the second half of the year, while housing-related loans surged sharply due to a rapid rise in housing costs. The year-on-year growth rates of mortgage loans were 8.5% in Q1, 8.6% in Q2, and 8.8% in Q3, maintaining an upward trend. On the other hand, other loans including credit loans saw their growth rate peak at 12.8% in Q2 and then decline in the second half as loans for Yeongkkeul and Debt Investment were blocked.

This year, corporate loans also increased to an all-time high, mainly in non-bank sectors such as mutual finance. As the COVID-19 crisis prolonged, loans to small and medium enterprises and individual business owners increased, pushing corporate loans to 1,497.8 trillion won by the end of Q3, a 12.4% increase compared to the same period last year. This is an increase of 138.4 trillion won compared to the end of last year.

In particular, corporate loans at deposit banks recorded 1,055.2 trillion won, showing an 8.2% growth rate, while non-bank financial institutions recorded 442.6 trillion won, showing a high growth rate of 24.0%, mainly driven by mutual finance (28.7%). This abnormal phenomenon was influenced by the shift of some household housing purchase funds demand from mortgage loans to rental business loans due to strengthened household loan regulations, causing a surge in non-bank corporate loans. The share of corporate loans in total non-bank loans soared from 28.1% at the end of 2015 to about 48.2% at the end of September this year.

"Sleepless Because of Debt"... Interest Bombs Amid Regulatory Blades

This year, despite the surge in household debt, high-intensity loan regulations were introduced one after another. The regulations became full-fledged when Financial Services Commission Chairman Seungbeom Ko, known as the "loan grim reaper," took office. Chairman Ko, who assumed office in August, issued a drastic total volume regulation (managing growth rate at around 6%) to curb household debt exceeding 1,800 trillion won.

As a result, some banks had to stop lending or drastically reduce loan limits. Starting with NH Nonghyup Bank, which completely halted real estate secured loans in August, major commercial banks suspended some new loan services. However, as the household debt growth did not subside easily, the government announced in April an advanced household debt management plan including borrower-specific total debt service ratio (DSR) application, followed by early implementation of DSR stages 2 and 3 in October, strengthening DSR for the secondary financial sector, installment repayment, and stricter loan screening measures.

Originally, the April plan intended to gradually expand the DSR regulation target from loans exceeding 200 million won starting July next year, and loans exceeding 100 million won from July 2023. However, to curb the household debt increase, the implementation of stage 2 DSR was advanced by six months and stage 3 by one year.

With two base interest rate hikes overlapping with loan regulations, borrowers face the side effect of an interest bomb. Among new household loans, the proportion of variable interest rate loans reaches 80%. As of October, the weighted average interest rate on new household loans at deposit banks was 3.46% per annum, nearly 1 percentage point higher than 2.79% at the end of last year. Some banks' mortgage and credit loan rates have soared to 5-6% per annum.

The balloon effect, where loans in the secondary financial sector surged due to sudden tightening of loans by commercial banks, is also one of the loan increase risks closely watched by the financial sector this year. For household loans, while the loan growth rate at banks was 9.9% in Q3 compared to the same period last year, non-bank institutions recorded a higher 10.8%. Before the COVID-19 outbreak at the end of 2019, bank household loan growth was 7.7%, while non-bank was -0.7%, showing a clear difference.

Experts gave a failing grade to household debt management this year. Professor Junggeun Oh of Konkuk University's Department of Economics said, "This year, the policy framework was based on regulating the total volume to suppress household loans, but it failed to address the fundamental causes. Low-income people were driven to high-interest illegal private loans due to difficulties in securing living or business funds, and this trend will continue."

Frozen Funding Continues Next Year... Including Card Loans and Savings Banks

Since the second half of this year, the lending threshold has risen sharply due to strong regulations by financial authorities, blocking genuine borrowers' access to funds, and it is expected that fund circulation will remain difficult next year. This is because the strengthened total debt service ratio (DSR) system, introduced as a regulatory measure due to the surge in household debt caused by the COVID-19 impact and the Yeongkkeul and Debt Investment frenzy, will be fully implemented from next month. Loans from the secondary financial sector, such as card loans, which serve as quick cash channels, are also expected to be tightened by strengthened regulations, so the loan drought for vulnerable groups is expected to persist.

Major commercial banks will simultaneously resume loans that were closed from next month. NH Nonghyup Bank will increase credit loan and overdraft limits from next month. Woori Bank will raise preferential interest rates on four out of ten credit loan products and mortgage loans by up to 0.6 percentage points starting from the 3rd of next month. Toss Bank will resume credit loan products from the 1st of next month.

With the annual loan volume targets for each bank being reset from January 1 next year, and suspended loans resuming, some breathing room is expected. However, concerns arise that the actual perceived lending threshold may rise further as the DSR regulation will be implemented from next month. From next year, borrower-level DSR regulations will apply to borrowers with total loans exceeding 200 million won, and from July, to those exceeding 100 million won. According to data submitted by NICE Information Service to the Financial Services Commission as of the end of September, the total number of household loan borrowers is 19,990,686. According to data received by People Power Party lawmaker Minguk Kang from the Financial Services Commission, 2,639,635 borrowers with loans over 200 million won can only borrow up to a 40% DSR ratio at banks, and the number of regulated borrowers will increase to 5,953,694 from July.

With a 40% DSR applied, a borrower with an annual income of 50 million won can only borrow up to 20 million won in principal and interest annually from banks. Even considering the secondary financial sector, the limit is 25 million won. Borrowers who already have large loans will have even less capacity for additional borrowing. Professor Taeyoon Sung of Yonsei University's Department of Economics said, "Strengthening DSR is meaningful," but added, "If DSR becomes a wall for borrowers with sufficient actual income and creditworthiness just to curb the speed of household debt increase and prevent the simple increase in numbers, it is undesirable."

Loan volume targets for banks have also been lowered. Under government pressure to curb household loan growth, they will be managed at 4-5%, lower than this year's 5-6%. This means bank loan supply will decrease.

It is also expected to become more difficult for low-income people who cannot cross the bank threshold to borrow from the secondary financial sector. From next year, the average DSR standards by sector in the secondary financial sector will also be strengthened. In particular, card loans, a quick cash channel for low-income people, will be included in borrower-level DSR regulations, further reducing the borrowing limits for borrowers who already have loans.

Experts advised that more fundamental solutions are needed. Professor Sangbong Kim of Hansung University's Department of Economics said, "The current household debt increase situation cannot be suppressed by financial policy or financial regulation alone. Efforts to stabilize real estate prices to manage additional loan demand and fundamental restructuring of the self-employed market to correct conditions that force excessive reliance on debt must be carried out simultaneously."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}

{kind=link}