Controversy Over Unregulated Reverse Discrimination Rekindled

Big Tech Targeted Amid Tilted Playing Field Debate

Big Tech Industry Anxious... Management Skills Put to the Test

[Asia Economy Reporters Kwangho Lee, Kiho Sung, Jinho Kim] As the year-end and New Year holidays approach, taxi calls have surged, intensifying competition among related applications (apps) such as Kakao, Wooty, and Tada. Among them, Tada was acquired by Viva Republica, the operator of the financial service app Toss, last October. This was possible because Viva Republica is an 'electronic financial business operator' but not a 'financial institution' subject to the Financial Industry Structural Improvement Act (FISA). In contrast, domestic banks cannot acquire apps like Tada because the acquisition of non-financial company shares is limited to within 15% under FISA.

The controversy over reverse discrimination against big tech (large information technology companies) and fintech (finance + technology), which have shown unstoppable progress in the financial market by emphasizing innovation, has reignited. This is due to strong backlash over unfair competition with big tech and fintech companies that are not regulated, following the aftershocks of card company merchant fee reductions.

In the market, there have been continuous criticisms that the financial authorities opened the gate to let big tech play the role of a 'catalyst' for innovation, but it turned into an abuse of monopoly power, reversing roles. This is the background behind the newly appointed financial authorities emphasizing correcting the 'tilted playing field' immediately upon taking office. However, there are also voices of concern that sudden and excessive regulations could hinder financial innovation.

According to the financial sector on the 28th, the Card Company Labor Union Council, composed of unions from seven card companies (Shinhan, KB Kookmin, Hyundai, Lotte, Hana, Woori, BC), held a press conference on the previous day regarding the reduction of merchant fees and announced a postponement of the general strike. One of the conditions for the postponement was the 'elimination of regulatory arbitrage with big tech.'

Big tech simple payment services such as Naver Pay and Kakao Pay charge higher fees than card companies but are not regulated at all. According to the office of Kim Han-jung, a member of the Democratic Party of Korea, the merchant fee rate for card companies until this year is 0.8%. Naver Pay and Kakao Pay charge merchants fees of 2.2% and 2.0%, respectively.

The regulatory arbitrage is also reflected in performance. Naver Pay's payment amount in the third quarter of this year was 9.8 trillion KRW, a 39% increase compared to the previous year. Meanwhile, card companies suffered a fee loss of about 130 billion KRW last year.

Data sharing is also cited by financial companies as an example of reverse discrimination. It is argued that big tech can provide services tailored to their preferences to customers locked into specific platforms.

A financial sector official said, "Fair rules are necessary for a fair game," emphasizing, "Rather than benefiting certain companies through 'regulatory arbitrage,' the principle of 'same function, same regulation' must be upheld."

Some voices express concern over big tech and fintech regulations, pointing out that sudden regulations could infringe on consumer benefits and cause setbacks in financial innovation.

Stronger Regulations from Next Year... Targeting the 'Tilted Playing Field'

"The entry of big tech (large information technology companies) into finance must be carried out under the principle of same function, same regulation." (Ko Seung-beom, Financial Services Commission Chairman, December 15 Big Tech Meeting Opening Remarks)

Financial authorities' regulations on big tech such as Naver and Kakao are expected to become more active starting this year and intensifying next year. This is because the financial authorities' stance on big tech has shifted from a favoritism mode after the replacement of two heads to a 'strict regulation mode.' The new stance of the financial authorities is that fair competition must take place on a broader and higher playing field in the digital transformation of finance.

The financial authorities have decided to revert the various conveniences given to big tech through 'regulatory relaxation' back to the starting point. This is interpreted as meaning that the principle of 'same function, same regulation' will be applied to eliminate favoritism controversies toward big tech.

Big tech has received much lower levels of regulation than traditional financial companies such as banks under the name of financial innovation. Riding on these privileges, big tech has rapidly grown in recent years, changing the landscape of the financial market. Currently, Naver's market capitalization is about 62 trillion KRW, comparable to the combined market capitalization of the four major financial holding companies. Recently listed Kakao Bank and Kakao Pay have also far surpassed the value of financial holding companies.

However, this rapid growth of big tech has caused many controversies. A representative example is 'MyData,' considered the future growth engine of financial companies. Financial companies provided most personal credit information related to financial transactions to big tech as MyData operators, but big tech refused to provide core e-commerce information such as 'order details,' claiming it is not personal credit information.

The 'Debt Consolidation Loan Platform,' a key project promoted by the financial authorities this year, also failed due to a structure excessively favorable to big tech. Existing financial companies hesitated to participate, citing that big tech holds the leadership of the platform. This is because offering high fees could reduce them to merely providing product procurement functions. A banking sector official said, "If it had been introduced, it would have been a situation where the bear (banks) does the tricks, and the landlord (big tech) takes the money."

Accordingly, after the replacement of the head, the financial authorities have significantly strengthened regulations on big tech. Chairman Ko Seung-beom's firm stance is that the 'tilted playing field' will no longer be tolerated.

Shortly after Chairman Ko's inauguration, the financial authorities defined big tech's customized financial product recommendations as violations of the 'Financial Consumer Protection Act.' As a result, some big tech companies such as Kakao Pay had to suspend their services. Additionally, through amendments to the Electronic Financial Transactions Act, regulations on big tech's data monopoly and biased service provision will be strengthened. The proposed amendment to the Electronic Financial Transactions Act submitted to the National Assembly prohibits abuse of superior status such as shifting losses to financial platforms, forcing economic benefits, and interfering in management activities.

Experts positively evaluate the financial authorities' 'same function, same regulation' principle as it can block controversies over preferential treatment that have arisen so far. Professor Minhwan Lee of Inha University's Department of Global Finance said, "The problem started because big tech's business was no different from financial business but was not regulated. The principle of same function, same regulation will be an important principle to minimize consumer protection issues and conflicts between companies."

Big Tech on Edge... Test of Management Capability

Financial authorities' regulations on big tech will be further strengthened next year. The Financial Services Commission recently announced plans to introduce a supervisory system targeting big tech groups and to check potential risks arising from big tech as part of next year's work plan.

There is a strong possibility of applying the 'Financial Conglomerate Supervision Act,' which applies to financial groups rather than holding companies like Samsung and Hanwha, to big tech. If big tech companies become subject to the Financial Conglomerate Supervision Act, their aggressive business expansion based on platforms will inevitably be restrained. Capital burdens will increase, and internal transactions among affiliates will be restricted. This is interpreted as an effort to correct the 'tilted playing field' between big tech and existing financial companies.

Researcher Sunho Lee of the Korea Institute of Finance argued, "To block financial system risks from big tech, it is necessary to review whether to designate them as complex financial groups under the 'Financial Group Supervision Act' and prepare preemptive management measures to prevent risk transfer between financial and non-financial sectors."

The Financial Supervisory Service plans to strengthen consumer protection measures for prepaid recharge funds of big tech, which are not covered by deposit insurance. This is intended to prevent incidents similar to the recent so-called 'Merge Point incident.'

Meanwhile, the big tech industry is anxious about the financial authorities' 'strict regulation mode.' Especially, there are strong concerns about the fact that regulations are being strengthened despite calls for financial innovation. A big tech official said, "The principle of same function, same regulation is emphasized, but the fact that the business environments of existing financial companies and big tech are completely different is not considered. Excessive regulation is worrisome as it could infringe on consumer benefits."

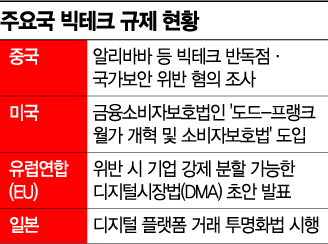

Strong Sanctions in the US, China, Japan, and EU... 'Preventing Monopoly'

Regulations on big tech (large information technology companies) and fintech (finance + technology) in the financial industry are not limited to South Korea. Global big tech companies in the US, China, Japan, and the European Union (EU) also face strong sanctions after entering the financial sector. Especially in China, combined with internal political issues, the government exerts tremendous pressure, reflecting a global consensus on the need to prevent monopolies by big tech companies.

China, once regarded as the most advanced country in the financial industry, has shifted to strict regulation of technology companies, including fintech. As a result, in October last year, Ant Group, Alibaba's financial group, had its initial public offering (IPO) halted, causing the listing to fail. At that time, Chinese financial authorities went further by ordering Ant Group's loan credit data to be transferred to a state-owned company, effectively nationalizing it. The pressure that started with Alibaba later affected other big tech companies such as Tencent and Baidu.

The United States, a pillar of the global economy, regulates fintech companies under the 'Dodd-Frank Wall Street Reform and Consumer Protection Act' enacted after 2008. This law was established during the Barack Obama administration to address problems arising from the global financial crisis. It is considered the strongest financial regulation since the Glass-Steagall Act (which separated commercial and investment banking after the Great Depression). This is why big tech companies like Amazon hesitate to enter financial businesses. In fact, Amazon, which operates simple payment, lending, and investment services, uses its own big data for loan screening, unlike traditional banks.

Policies that strengthen regulations on big tech themselves to discourage their entry into financial businesses are also being implemented. In June, the Biden administration appointed Lina Khan, a Columbia University professor known as the 'Amazon hunter,' as chair of the Federal Trade Commission (FTC). Chair Khan is known for her 2017 paper 'The Amazon Antitrust Paradox,' advocating active regulation of platform companies. The House Democrats and Republicans jointly introduced an antitrust package bill targeting big tech companies such as Amazon, Apple, Facebook, and Google.

The EU is also pressuring big tech companies with regulations. In December last year, the EU announced drafts of the Digital Markets Act (DMA) and Digital Services Act (DSA). These prohibit platform companies from favoring their own services through algorithms or deleting pre-installed applications on smartphones. Violations may result in fines of up to 10% of revenue or forced corporate breakups.

Japan is also tightening regulations on big tech through the Digital Platform Transaction Transparency Act. Enacted in February, this law designates five companies operating online malls?Amazon, Rakuten Group, Yahoo, Google, and Apple?as specific digital platform providers. It mandates prior notice of changes in transaction conditions and the establishment of systems for handling complaints. These companies must submit reports once a year.

Among economic experts, opinions differ between 'efforts to prevent market collapse' and 'enhancing consumer choice.' Professor Sangbong Kim of Hansung University's Department of Economics said, "Major countries are strengthening financial regulations on fintech companies because the market could collapse. Financial authorities should listen to diverse opinions and manage carefully." On the other hand, Professor Taeyoon Sung of Yonsei University's Department of Economics emphasized, "Platforms should be viewed from the consumer's perspective. Strengthening regulations will stifle innovation, so consumers should be able to utilize and choose new services."

Jung Eun-bo, Governor of the Financial Supervisory Service, stated at the recent '2021 Seoul International Finance Conference,' "The Financial Supervisory Service will listen to global discussions on fair competition issues between financial companies and big tech," and "We will continue to promote financial innovation and regulatory improvements for financial companies and fintech firms."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}

{kind=link}

{kind=link}