[Asia Economy Reporter Junho Hwang] The monetary policies of major global economies such as the United States and Europe have turned hawkish. As their tightening stance strengthens, long-term bond yields in each country are expected to face downward pressure until the beginning of the year.

Shinhan Investment Corp. summarized the recent tendencies of central banks' monetary policies in a bond strategy report on the 18th.

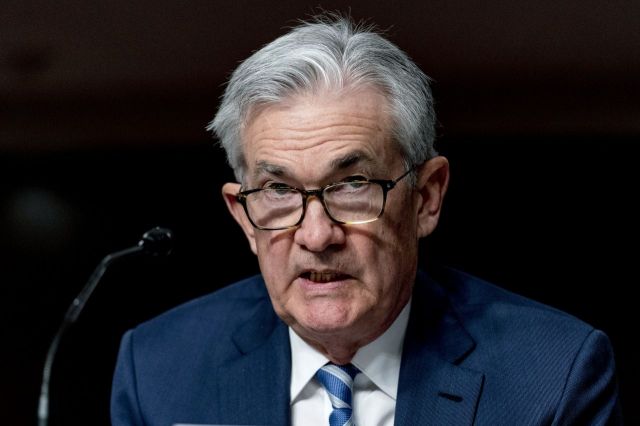

First, the U.S. Federal Open Market Committee (FOMC) has become the most hawkish this year. Discussions covered all aspects of monetary policy normalization, including tapering acceleration, interest rate hikes, and balance sheet reduction. However, the impact on the bond market on the day was limited, interpreted as largely priced in following Chairman Powell's responses at congressional hearings earlier this month.

The European Central Bank (ECB) also adopted a hawkish stance. Market attention focused on changes to asset purchase policies. The ECB decided to end the PEPP in March next year but increase the APP to mitigate market shocks. Minyoung Park, a researcher at Shinhan Investment Corp., analyzed, "Considering that the worsening COVID-19 situation in Germany since October raised the possibility of extending the PEPP, this can be seen as a somewhat hawkish decision. Although German government bond yields showed limited movement due to distant expectations of rate hikes, the euro's strength confirmed the market's hawkish perception of the ECB's policy decision."

The Bank of England (BoE) raised its benchmark interest rate by 15 basis points, contrary to market expectations of a rate freeze, increasing rate volatility. The decision was made to respond to future inflation following confirmation of employment data recovery.

Researcher Park forecasted, "Short-term yields on U.S. and German government bonds are expected to decouple further due to differences in the speed of monetary policy normalization. Long-term yields are likely to see limited increases until early next year despite Fed and ECB decisions to reduce asset purchases."

This is because uncertainties around Omicron and excessive inflation concerns are weakening growth forecasts, increasing downward pressure on long-term yields. However, Park cautioned that if these two issues are resolved in the first quarter of next year, the yield curve could reverse to steepening due to economic activity normalization, monetary policy normalization, and reduced demand for government bonds.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}