Allowed Within DSR Regulations... "Loans May Still Be Difficult Even with Special Circumstances"

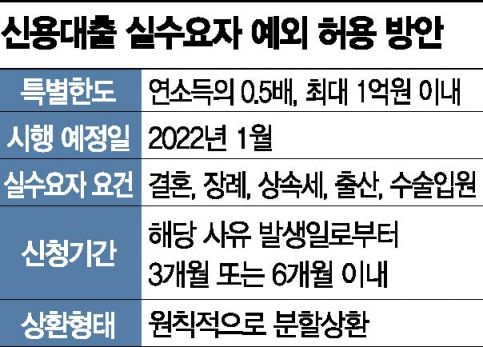

[Asia Economy Reporters Jin-ho Kim and Sun-mi Park] The credit loan limit, which has been restricted to within the annual income, will be additionally increased from January next year only for urgent real needs such as marriage, funeral, childbirth, and surgery. Even if the credit loan limit has already been reached, additional loans can be obtained within 0.5 times the annual income and up to 100 million KRW through the granted special limit. However, since the total debt service ratio (DSR) regulation will also be strengthened, there are concerns that borrowers with many existing loans will find it difficult to get additional loans even if exceptions apply.

According to the financial sector on the 8th, the Korea Federation of Banks has finalized the exception allowance plan for credit loan real demand borrowers through consultations with banks and is awaiting approval from the Financial Services Commission. The core content of this plan is to grant a special limit of 0.5 times the annual income and up to 100 million KRW to the credit loan limit restricted to within the annual income, upon application within 3 or 6 months from the occurrence of urgent fund needs due to marriage, funeral, inheritance tax, childbirth, or surgery hospitalization.

For marriage, an application can be made within 3 months from the marriage registration date with a certificate of marriage relationship. For funeral and inheritance tax, a closed family relation certificate or death confirmation must be submitted within 6 months from the date of death. For childbirth, an application can be made within 3 months before or after the childbirth (expected) date with a pregnancy diagnosis or confirmation document. For surgery hospitalization, proof such as a surgery confirmation or admission/discharge certificate is required, and the application must be made within 3 months from the surgery or discharge date.

For example, an office worker with an annual income of 50 million KRW who has already received a 50 million KRW credit loan from a bank can receive an additional 25 million KRW loan by submitting the relevant supporting documents. However, even though this special limit is given to urgent real demand borrowers, under the Stage 2 DSR regulation applied from January next year, borrowers with total loans exceeding 200 million KRW cannot get a loan if their annual principal and interest repayment amount exceeds 40% of their annual income.

The loan period can be autonomously set by the bank, but repayment must be made in installments. Borrowers currently using lump-sum repayment credit loans must use a new product different from the existing credit loan product to receive the special limit loan with installment repayment. Although the scope of operation has been broadened to allow banks to operate special limits through approval from the bank’s credit review committee if there is a need to recognize a borrower as a real demand borrower even if they do not meet the criteria, conversely, additional loans may be rejected depending on the review even if the criteria are met.

The Korea Federation of Banks initially aimed to implement this in November and continued discussions with the banking sector, but it was confirmed that the implementation was delayed due to the need for detailed coordination on the reasons for granting special credit loan limits and supporting documents.

Since the Financial Services Commission announced on October 26 a plan to strengthen household debt management and stated that it is reviewing the ‘exception application of credit loan limit within one times annual income’ for protecting low-income and real demand borrowers with a goal of implementation in November, immediate approval of this plan is anticipated. The Democratic Party and the government also plan to focus discussions on next year’s household loan total volume management plan and protection measures for low-income and real demand borrowers at the party-government meeting scheduled for the 10th.

A senior official from the Financial Services Commission said, "We have already set the direction to allow exceptions to the credit loan limit within one times annual income only for urgent real demand borrowers, and the detailed contents will follow the method agreed upon by the Korea Federation of Banks and the banking sector," adding, "Although there are concerns about side effects from granting special credit loan limits, since related documents must be submitted to receive exceptions, there is little chance of abuse."

Since banks bear the responsibility for screening additional loans for urgent real demand borrowers, it is widely expected that applications will not be possible through non-face-to-face channels. Non-face-to-face applications tend to simplify screening, making loan approval relatively easy. Previously, when excluding jeonse (long-term rental deposit) loans from household loan total volume management to protect real demand borrowers, non-face-to-face jeonse loan applications by one-homeowners were suspended to prevent jeonse loans from flowing into asset investment rather than real demand.

A bank official explained, "Specific details have not yet been notified to banks, so the system operation plan has not been decided. However, since supporting documents must be received and it would be difficult to verify authenticity non-face-to-face, it is highly likely that restrictions such as requiring visits to branches for application will be imposed."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}