[Asia Economy Reporter Lee Seon-ae] Mando is attracting attention from the financial investment industry by presenting its mid- to long-term growth strategy at its Investor Day.

On the 4th, most securities firms analyzing (covering) Mando maintained a buy rating and target price for the company. This is because Mando's growth potential was confirmed at the Investor Day held on the 2nd.

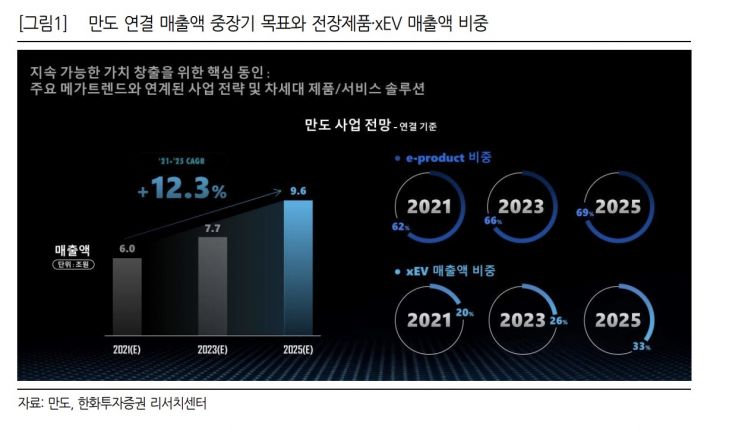

Mando presented its mid- to long-term vision for electric vehicles and autonomous driving. Mando's consolidated sales targets are set at 6 trillion KRW in 2021, 7 trillion KRW in 2023, and 9.6 trillion KRW in 2025. Among these, the proportion of electronic components is 62%, 66%, and 69%, respectively. The proportion of eco-friendly vehicles is 20%, 26%, and 33%. 80% of the 2025 sales target is already secured through orders, making achievement highly visible. The cumulative order backlog at the end of Q3 is 45 trillion KRW, of which 53% is from non-Hyundai-Kia companies and 20% from BEV manufacturers.

Detailed information was also shared regarding the business plan of HL Clemoove, which was newly launched in December. HL Clemoove is an autonomous driving and mobility specialized company (100% owned by Mando) formed by the physical division of Mando’s autonomous driving division and Mando’s affiliate (Mando Hella). HL Clemoove is responsible for the perception and decision-making parts of autonomous driving, while Mando handles the driving components. To this end, HL Clemoove plans to upgrade sensors, control systems, and software algorithms. HL Clemoove aims to increase sales by diversifying (increasing volume) and advancing (raising unit prices) autonomous driving products, with targets of 1.2 trillion KRW in 2021, 2.4 trillion KRW in 2026, and 4 trillion KRW in 2030.

The timeline to reach full and driverless autonomous driving levels 4 and 5 is taking longer than expected, leading to increased demand for level 2 to 3 autonomous driving. For parts suppliers to improve profitability, the only way is to sell new products to new customers. Mando plans to respond to level 2 to 3 autonomous driving by advancing Advanced Driver Assistance Systems (ADAS) through HL Clemoove. This will expand its customer base and improve profitability. Jinwoo Kim, a researcher at Korea Investment & Securities, emphasized, "Within the order backlog, products and customers have already diversified. As orders are recognized as sales, profitability, which has been trapped in a box range for the past 10 years, is expected to improve."

Mirae Asset Securities emphasized the need to focus on Mando’s mid- to long-term competitiveness enhancement. Yeonju Park, a researcher at Mirae Asset Securities, analyzed, "In the short term, Mando’s electric vehicle solution performance is important. As the semiconductor supply shortage gradually eases next year, recovery of customer volumes and expansion of electric vehicle proportions are expected to lead to gradual recovery. In the mid- to long-term, cost competitiveness in the market below level 2, clear positioning compared to other companies, and HL Clemoove’s autonomous driving competitiveness acquisition will be important from a valuation perspective."

Hanwha Investment & Securities noted that Mando’s blueprint, separating Chassis and ADAS/autonomous driving, has become more concrete, and that HL Clemoove’s ① global production bases, ② main target customer segments, ③ competitive advantages and sales strategies, and ④ CAPEX and R&D directions have been presented more clearly compared to June.

The physical division of the ADAS business has negatively affected investment sentiment so far. However, until factors that could dilute shares in HL Clemoove, such as an IPO, arise, the physical division will not impact consolidated performance, and funding activities are expected to begin no earlier than 2023. Therefore, if the Chassis business maintains solid performance and ADAS customer diversification?one of the key growth drivers shared this time?materializes meaningfully through supplying ADAS to North American electric truck companies, a re-rating is likely.

Junho Park, a researcher at Hanwha Investment & Securities, stated, "Even considering the possibility of long-term share dilution, if the ADAS business direction was a choice between ① low growth within Mando or ② funding and growth enhancement through physical division, the latter may be the better option. The key is to prove that the physical division was a rational choice for both the company and shareholder value enhancement."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}