[Super-Aged Society and Private Pensions - Part 2]

Korean Private Pension Enrollment Rate 16.9% · Tax Support Rate 20%

Up to 3.5 Times Difference Compared to Germany, USA, Japan

Germany and New Zealand Expand Private Pension Base Through Subsidies

[Asia Economy Reporter Ki Ha-young] As the population aged 65 and over is expected to exceed 20% by 2025, entering a super-aged society, Korea’s pension income replacement rate is revealed to be less than half of the average pre-retirement income. In contrast, advanced countries overseas have been promoting private pensions early on through tax incentives and other measures to prepare for aging and elderly poverty issues.

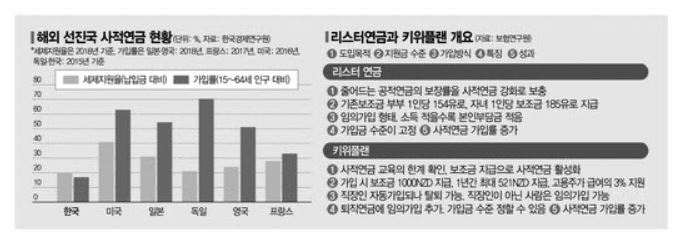

According to the Korea Economic Research Institute on the 28th, Korea’s public and private pension income replacement rate (as of 2018) was recorded at 43.4%, while the G5 countries including the United States, Japan, Germany, the United Kingdom, and France averaged 69.6%. Experts interpret this gap as stemming from the activation of private pensions. In particular, Germany and New Zealand encourage private pension enrollment by providing government subsidies.

Subsidies + Tax Benefits, Germany’s 'Riester Pension'

Germany introduced the 'Riester Pension,' a private pension consisting of government subsidies and tax support, through pension reform in 2001, reducing the level of public pension payments in exchange. What differentiates the Riester Pension from existing private pensions is that subsidies are the main benefit rather than tax deductions. If tax benefits exceed subsidies, the difference is provided as a tax benefit.

Riester Pension subscribers contribute 4% of their annual total income (up to 2,100 euros) to the pension. At this time, they receive a government basic subsidy of 154 euros (308 euros for couples) and a fixed amount of 185 euros per child (300 euros for children born after 2008). Subscribers pay the amount corresponding to 4% of their total income minus the subsidy as their own contribution. The system is designed to favor low-income groups by requiring lower personal contributions for those with lower incomes.

With the introduction of the Riester Pension, Germany’s private pension enrollment rate nearly doubled in seven years. In 2002, the proportion of households with one or more private pensions besides the public pension was only 26%, but it rose to 55% by 2009. Looking at enrollment by income level, although the absolute enrollment rate was higher for higher income levels, the enrollment rate for the lowest income quintile also increased from 5% to 25% during the same period. The number of Riester Pension subscribers grew from about 1.4 million at its introduction in 2001 to 16.5 million in 2016.

Retirement + Personal Pension, New Zealand’s 'KiwiPlan'

New Zealand’s 'KiwiPlan,' introduced in 2007, is also characterized by government subsidies. KiwiPlan, a voluntary retirement pension, automatically enrolls all employees aged 18 to 65 upon employment. Those who do not wish to join must express their refusal within eight weeks of employment. Those under 18 or unemployed can join voluntarily if they wish. Thus, KiwiPlan has the characteristics of both a retirement pension and a personal pension.

Employees can choose a contribution rate of 3%, 4%, or 8% of their total salary. Employers must contribute at least 3% of the annual salary of employees enrolled in KiwiPlan. Withdrawals are allowed after age 65 or five years after enrollment, whichever is later. To encourage enrollment, KiwiPlan provides an initial subsidy and annual subsidies. New enrollees receive an initial government subsidy of 1,000 NZD (New Zealand dollars), and those who meet the minimum contribution (3% of total salary) receive up to 521.43 NZD annually from the government. Additionally, employees enrolled in KiwiPlan receive employer contributions of at least 3% of their salary into their KiwiPlan account.

KiwiPlan is credited with significantly expanding the base of private pensions in New Zealand. The number of subscribers in the first year of KiwiPlan’s introduction was about 710,000, increasing to 2.14 million by 2013. The private pension enrollment rate, which was about 20% before KiwiPlan, grew to exceed 65% by 2013.

Korea’s Private Pension Tax Support Rate 20% 'Failing Grade'

While overseas countries have encouraged private pension enrollment through tax benefits, Korea’s private pension enrollment rate and tax support rate remain low. According to the Korea Economic Research Institute, Korea’s private pension tax support rate was only 20% as of 2018. This is less than half compared to overseas countries such as the United States (41%), Japan (31%), and France (28%). The private pension enrollment rate among the working-age population (15-64 years) was also 16.9%, showing a large gap compared to Germany (70.4%), the United States (62.9%), and Japan (54.3%). An insurance industry official said, “Policy support is necessary to systematically support retirement preparation over the medium to long term,” and pointed out that “raising the limits on pension tax support across all age groups is needed.”

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}

{kind=link}