Q3 Earnings Show Quarterly Sales Decline for the First Time in 16 Years

New Drug Launch Momentum Expected to Reflect from 2022 to 2024

[Asia Economy Reporter Minji Lee] Hangzhou Pharmaceutical recorded sluggish performance in the third quarter, and it is expected to be difficult to see a recovery trend in the near term. This is because it is anticipated that a short-term rebound in performance will be challenging due to the government's bulk drug purchasing (price reduction) policy and increased research and development expenses.

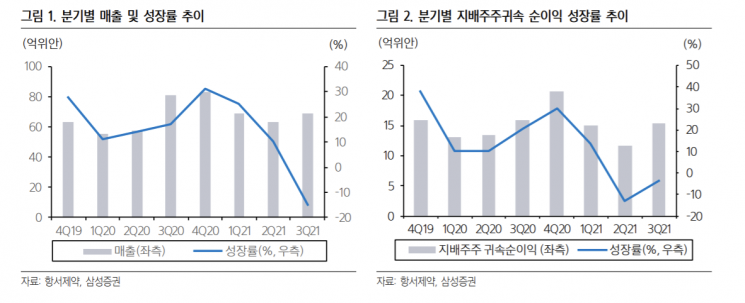

According to the financial investment industry on the 23rd, Hangzhou Pharmaceutical's stock price recorded 51.30 yuan as of the 22nd, down 53.87% since the beginning of the year. The stock price decline appears to have continued as concerns over the performance drop were reflected. Hangzhou Pharmaceutical posted third-quarter sales of 6.9 billion yuan and net profit attributable to controlling shareholders of 1.5 billion yuan, down 15% and 3.6%, respectively, compared to the same period last year. Considering that the market expects annual sales growth of 12% and net profit growth of 9% year-on-year, this is analyzed to be significantly below market expectations.

Looking at the company's quarterly sales growth rates, they were 25.4% in Q1, 10% in Q2, and -14.8% in Q3, while net profit growth attributable to controlling shareholders was 13.8%, -13.1%, and -3.6%, respectively, showing a visible slowdown in growth. Quarterly sales recorded negative growth for the first time in 16 years, which is analyzed to be due to the dual challenges of government drug price reductions, sales growth slowdown caused by new drug development promotion policies, and increased costs.

Seungmin Kim, a researcher at Mirae Asset Securities, said, “The application of government insurance coverage for Camrelizumab (PD-1), sales volume growth that did not meet expectations compared to the reduced price, slow penetration into new hospitals, and negative growth due to price reductions from the government's generic bulk purchasing policy are considered to have influenced the results.” He added, “We expected new drug sales growth of about 17%, but it fell short of expectations.”

As research and development expenses are expected to increase, the performance burden is likely to continue for the time being. The cumulative R&D expenses for the third quarter were 4.14 billion yuan, up 23.8% year-on-year, accounting for nearly 20% of total sales. Furthermore, since the impact of the drug price reduction policy will be fully reflected in the fourth quarter, it is predicted to be difficult to expect a recovery in performance growth for the time being.

Sunmyung Hwang, a researcher at Samsung Securities, predicted, “The late-stage clinical pipeline consists of 15 candidates, covering various areas such as anti-PD-L1 immuno-oncology drugs, AR inhibitors, JAK inhibitors for autoimmune diseases, anti-infectives, ophthalmology, and diabetes, but full-scale commercialization is expected to proceed between 2022 and 2024.”

In the securities industry, while the potential for development as a leader in new drug development is high from a mid- to long-term perspective, a conservative approach is advised for the time being. Researcher Hwang said, “Time is needed to absorb the dual challenges of margin decline in generic drugs and increased R&D expenses for new drug development,” adding, “Until a recovery in performance growth is confirmed, a conservative stance should be maintained.”

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}