Popularity of Agent Loans Amid Regulatory Restrictions and Interest Rate Hikes

"Apply 3 Months Before Balance Due Date" Solicitation

Agents Experience Unexpected Sales Boom as Contracts Increase

Bold Offer of '2% Fixed Rate Mortgage Loans'

Beware of Illegal and Fraudulent Activities Such as Registration Number Checks

Kim Ji-hyung (34, pseudonym), who lives in Mapo-gu, Seoul, was looking into jeonse loan financing for his move when he received advice from an acquaintance that it would be advantageous to go through a loan broker. He was told that if he only requested the broker to submit the approval document in advance, he would not be subject to future financial regulatory measures. Worried that his loan limit might be reduced, Kim consulted with the landlord and then met the broker to apply for the loan two months earlier than his planned moving date.

Ryu Sang-hyun (45, pseudonym), who works as a loan broker for a regional bank in Seoul, closed seven contracts in a single day on the 20th. This was because as interest rates rose and financial regulations tightened, more financial consumers sought alternative loan routes. Ryu explained, “Since the jeonse loan regulation issue broke out, it has been a boom period for business,” adding, “At the request of customers, I sometimes visit their homes at dawn to finalize loan contracts.”

[Asia Economy Reporter Song Seung-seop] Amid the tightening of household loans by financial authorities, which has already raised the loan thresholds at commercial banks, additional regulations have been announced, drawing attention to loans through brokers as a ‘niche market.’ This is because brokers exploit regulatory blind spots that ordinary people find hard to detect, attracting those in need of funds with relatively low interest rates and generous limits. The covert trend of circumventing loans by obtaining them before the desired time has even become popular.

According to financial circles and industry sources on the 21st, loan contracts through brokers have recently been noticeably increasing. This is because consumers seeking loan consultations are flocking due to financial authorities’ regulations and interest rate hikes. Many consumers had previously avoided brokers due to concerns about involvement in illegal operations. However, industry insiders commonly explain that contract performance in the past month has increased two to three times compared to usual.

A loan broker refers to counselors and recruiting corporations that perform loan-related tasks under a business consignment contract with financial companies. They handle applications, consultations, submission, and delivery, including online loans via the internet.

Brokers often reside in online financial and real estate communities and approach members who post loan-related consultation posts by providing messenger links. They mainly guide loans centered on some commercial banks or regional banks that still have remaining loan limits.

The target customers are high-credit clients with sufficient financial capacity but increased interest burdens due to rate hikes. This contrasts with past business methods that connected hard-to-loan middle- and low-credit borrowers to secondary and tertiary financial institutions. The target has shifted due to the large supply of policy financial products for low-income and low-credit borrowers and mid-interest loans, as well as the emergence of fintech companies comparing loan interest rates.

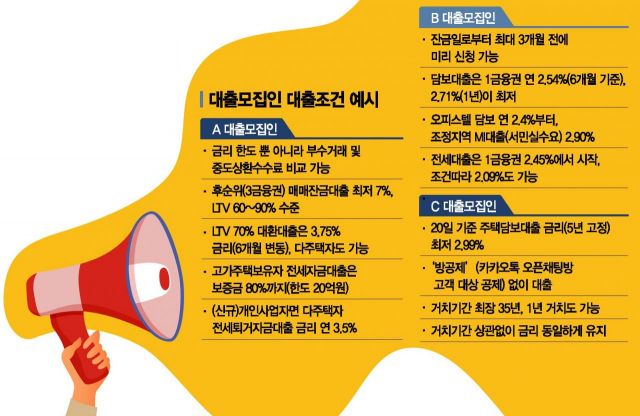

"We will allow loans up to 2 billion KRW regardless of DTI (Debt-to-Income ratio)," and "the minimum interest rate is 3.5% per annum (6-month variable basis), with up to 80% of the deposit available," was offered. Broker B promoted, "For mortgage loans, I will introduce products with a minimum fixed interest rate of 2.99% for 5 years," adding, "The grace period can be up to 35 years, and even with a 1-year grace period, the interest rate remains the same."

There were also cases of guiding what could be called a kind of loophole loan. It was explained that if a broker submits the approval document to the bank in advance, the loan execution after the new regulations are introduced will not be retroactively applied. Various communities are sharing methods of ‘applying for loans in advance.’ Broker C proposed, "The bank’s new loan judgment criterion is the application date, not the execution date," and "I can prepare the loan approval document up to 3 months in advance."

As broker-linked loans become popular, warnings have been issued to be especially cautious of illegal and private operators. According to current law, loan counselors can only receive commissions from banks and cannot charge customers fees. They cannot perform post-management tasks such as debt collection or loan interest collection. It is also prohibited to leak customer information externally.

To prevent damage, it is necessary to check the broker’s registration information in advance through the integrated loan broker inquiry system operated by the Korea Federation of Banks. Commission rate disclosure information of loan brokers can also be verified. Since the information might be stolen, it is also important to meet in person to confirm identity.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

{kind=link}

{kind=link}