20s Residential Mortgage Loans Up 89%

Economic Agents' Profit-Seeking Expected to Ease

Lee Ju-yeol, BOK Governor: "One Rate Hike Won't Resolve Financial Imbalance"

[Asia Economy Reporter Jang Sehee] The amount of loans secured by young people in their 20s using housing, commercial buildings, and farmland as collateral has surged by 89% in one year. As asset prices soared due to prolonged low interest rates, not only are they engaging in 'debt investment' through unsecured loans, but young people with asset flexibility are also joining the loan trend by using real estate as collateral.

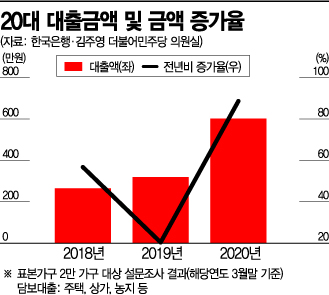

On the 21st, the Bank of Korea revealed in the results of the "Collateral Loans and Growth Rates by Age Group (Average per Household) excluding Residential Housing" survey submitted to the office of Kim Ju-young, a member of the National Assembly's Planning and Finance Committee from the Democratic Party, that the amount of asset-backed loans for those in their 20s last year was 6.02 million KRW, an 88.7% increase compared to the previous year. The loan amount for people in their 20s rose from 1.69 million KRW in 2017 to 3.19 million KRW in 2019, and last year's growth rate for this age group was 88.7%, significantly higher than that of those in their 50s (14.2%) and 40s (8.3%).

This survey was conducted on a sample of 20,000 households secured by the Bank of Korea, the Financial Supervisory Service, and Statistics Korea for the "Household Finance and Welfare Survey Statistics." It extracted the scale of collateral loans held by asset-owning households by distinguishing between resident and non-resident status, which cannot be identified at the time of obtaining collateral loans. Loans are taken out using commercial buildings or farmland registered under the borrower's name as collateral, and since loans increase according to the collateral value, this can be interpreted as 'gap investment.' The collateral loan amounts were mainly used for additional housing purchases or stock trading.

Collateral loan amounts excluding residential housing for all age groups, including those in their 20s, have also been increasing annually. It rose from 13.97 million KRW in 2018 to 14.02 million KRW in 2019, and recorded 15.3 million KRW last year. This is seen as a natural increase in loan amounts due to the rise in relatively less burdensome gap investments.

Such loans have a high possibility of leading to financial distress if asset prices fall. Especially as the policy to raise the base interest rate becomes firm, the asset market is fluctuating. Recently, the real estate market's price increase has slowed. According to the Korea Real Estate Board, in the second week of this month (as of the 11th), nationwide apartment sale prices rose by 0.27%, and jeonse (long-term lease) prices increased by 0.19%. Compared to the previous week's growth rates, both decreased by 0.01 percentage points, indicating a contraction in the rate of increase. This is interpreted as meaning that the number of people wanting to buy houses is decreasing while listings are increasing.

Assemblyman Kim said, "It seems necessary to analyze credit risk considering the income level and asset accumulation of young people," and emphasized, "The Bank of Korea and financial authorities should collaborate to solve the deepening polarization problem." Last year, the disposable income of those in their 20s was 30.38 million KRW, a 4.2% decrease compared to the previous year (31.71 million KRW).

Professor Ha Jun-kyung of Hanyang University's Department of Economics advised, "As debt borrowing decreases, some bubbles in the asset market may burst," adding, "Bubbles will eventually burst, and the longer the delay, the greater the shock will be." Researcher Cho Young-hyun of the Korea Insurance Research Institute said in a recent research report, "Due to future policies to alleviate financial imbalances, the phenomenon of economic agents seeking returns is expected to ease," and "There will be a slowdown in liquidity growth, easing of short-term funding phenomena, and an expansion of downside risks in risky assets."

Meanwhile, Lee Ju-yeol, Governor of the Bank of Korea, has indicated his intention to raise the base interest rate at the Monetary Policy Committee meeting next month. Governor Lee stated, "As the low interest rate situation has lasted for about a year and a half, side effects such as excessive profit-seeking behavior through borrowing have begun to appear," and added, "This measure (interest rate hike) will not resolve the issue with just one action."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}