Preview of a Groundbreaking New Deposit Product

Attention Focused on Early Success

[Asia Economy Reporter Kiho Sung] The third internet-only bank, Toss Bank, is set to launch this month. The industry is showing great interest in Toss Bank's initial moves. It has announced an aggressive marketing strategy with groundbreaking deposit and loan products right from the start. In particular, amid tightening household loan regulations by financial authorities, the credit loan with a maximum limit of 270 million KRW is attracting even more attention. However, the industry expects that, due to the nature of internet banks, there will be no sudden concentration of loans. Additionally, the number of users utilizing Toss Bank is pointed out as a key factor for its future success.

According to the financial sector on the 2nd, Toss Bank partially revealed its loan product lineup on its website on the 26th of last month. There are two types: Saetdol loans and credit loans, with the credit loan limit set at a maximum of 270 million KRW and an interest rate ranging from 2.76% to 15.00% per annum.

What draws the most attention is that Toss Bank's credit loan conditions are truly groundbreaking. According to the Korea Federation of Banks, the average interest rates of the five major commercial banks?KB Kookmin, Shinhan, Hana, Woori, and NH Nonghyup?in August ranged from 3.07% to 3.62% per annum. Internet banks KakaoBank and K Bank offer rates of 4.95% and 4.27% per annum, respectively. Especially in an environment where all financial institutions are drastically reducing credit loan balances, a loan limit exceeding 100 million KRW is considered highly attractive. This is why it is predicted that borrowers in urgent need of loans will flock to Toss Bank. Moreover, since this is Toss Bank's first year of operation, it is expected to avoid the financial authorities' total household loan volume management.

The key issue is the number of users. A banking industry official explained, "The maximum credit loan limit is 270 million KRW, but not all customers can receive the maximum limit. Ultimately, the limit varies depending on the credit rating." He added, "Due to the nature of internet banks, the performance of deposits and loans depends not only on conditions but also on the growth rate of users, so Toss Bank is expected to follow the same path."

A representative example is K Bank. K Bank currently offers credit loans up to 250 million KRW for salaried workers. The interest rate is at a minimum level of 2.89% per annum, and salaried employees who have been employed at the same company for more than six months and have an annualized income of over 30 million KRW can receive loans depending on their personal credit status. Additionally, K Bank operates a salaried worker overdraft loan product with a maximum limit of 150 million KRW. The interest rate is also at a minimum level of 3.39% per annum.

K Bank attracted the highest number of users in April this year, with a cumulative user count of 5.37 million, up from 3.91 million the previous month. Consequently, deposits and loans increased by 3.42 trillion KRW and 850 billion KRW, respectively. However, in August, when the user increase was lower than in April?from 6.28 million (July) to 6.45 million?the deposits increased by only 830 billion KRW and loans by 210 billion KRW. Although a balloon effect was expected toward K Bank, which has high loan limits, due to financial authorities' loan regulations at the time, the increase in deposits and loans ultimately followed the user growth.

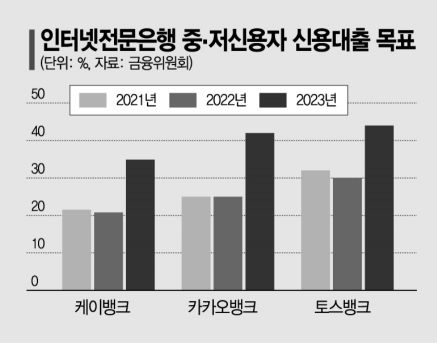

Another banking industry official stated, "Since Toss Bank announced it would maintain a 34.9% share of mid-interest loans by the end of this year, it cannot increase credit loans indefinitely," adding, "In fact, the launch of Toss Bank will disperse loan demand, which could be beneficial for other banks."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}