Toss Bank to Launch Next Month, Signaling Fierce Competition in the Mid-Interest Loan Market

Major Banks Also Expanding Their Share of Mid-Interest Loans

[Asia Economy Reporter Kim Jin-ho] In the second half of this year, competition over 'mid-interest rate loans' is expected to intensify across all banks, including commercial banks and internet-only banks. This is attributed to the fact that mid-interest rate loans are relatively free from the government's strong pressure on household loans. In particular, Toss Bank, which is launching early next month, is preparing to release mid-interest rate loan products with unprecedented limits and interest rates, making the mid-interest rate loan market a new battleground for banks.

According to the financial sector on the 26th, the interest rates for unsecured loans announced on Toss Bank's website range from 2.76% to 15% per annum, with limits from a minimum of 1 million KRW to a maximum of 270 million KRW.

Although it varies depending on an individual's credit and repayment ability, the industry expects Toss Bank's unsecured loan product to have a minimum interest rate in the high 2% range and a maximum limit of 270 million KRW. Considering that recent unsecured loan interest rates at commercial banks are around 4-5% with limits of about 50 million KRW, this is truly unprecedented.

Toss Bank has declared that it will expand the proportion of mid-interest rate loans to 34.9% of total unsecured loans by the end of this year. This is much higher than the 20% target set by other internet-only banks.

K Bank and Kakao Bank are also focusing on expanding mid-interest rate loans. They are conducting aggressive marketing, including subsidizing loan interest to attract medium- and low-credit customers. Since June, Kakao Bank has applied an advanced credit evaluation model to increase the loan limit for medium- and low-credit customers up to 100 million KRW.

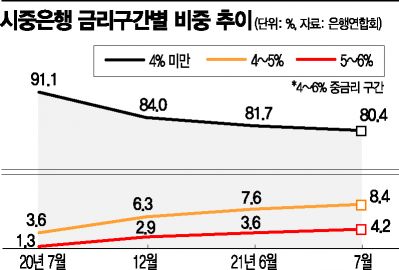

Commercial banks, which have traditionally focused on high-credit customers, are also actively handling mid-interest rate loans. According to the Korea Federation of Banks, the proportion of mid-interest rate unsecured loans (4-6%) at the four major commercial banks?KB Kookmin, Shinhan, Hana, and Woori?rose to 12.7% last month, up 1.5 percentage points from 11.2% the previous month. A year ago, the proportion was only 5.2%.

The banking sector's efforts to expand mid-interest rate loans are influenced by the financial authorities' demand to 'activate mid-interest rate loans' and the relative freedom from household loan volume regulations. In particular, the financial authorities recently received plans from internet banks to increase the proportion of medium- and low-credit loans over the next three years.

However, as the mid-interest rate loan market emerges as a battleground across all banks, concerns have been raised that it could become a target of financial authorities' regulations. While expanding mid-interest rate loans for real demand and low-income households is a good intention, there is criticism that excessive competition among banks could turn mid-interest rate loans into a new flashpoint for household debt.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}