Household Loans in Secondary Financial Sector Increase by 27.4 Trillion KRW from January to July

Mutual Finance Sector Rises by 12 Trillion KRW, Showing Steepest Growth

'Yeongkkeul Law' Trending in Investment and Office Worker Communities

Cases of Husbands Registering Wives as Tenants to Their Own Landlords

Experts Criticize "Market Distortion Due to Successive Regulations"

[Asia Economy Reporter Song Seung-seop] Due to the financial authorities' stringent loan regulations, commercial banks are raising the loan threshold by halting sales of certain products and restricting unsecured loans. Despite the authorities' efforts to contain the situation, the market is already showing signs of a balloon effect. Among real borrowers urgently needing loans, unconventional 'Youngkkeul-beop (borrowing to the soul)' practices are rampant. There are concerns that market distortions caused by government regulations are occurring.

According to the financial industry on the 28th, the five major commercial banks?KB Kookmin, Shinhan, Hana, Woori, and NH Nonghyup?have either limited or plan to reduce unsecured loan limits to the level of annual income. Internet-only bank KakaoBank will also reduce unsecured loan limits to the annual income level next month. K Bank is reportedly considering reducing unsecured loan limits as well.

This is in response to the financial authorities' recommendation to curb the rising trend of household loans. On the 13th, the Financial Supervisory Service held a meeting with loan officers from commercial banks and requested that personal unsecured loan limits, such as overdraft accounts, be restricted to annual income levels. This measure was also ordered to be applied equally to secondary financial sectors such as savings banks, mutual finance, and credit card companies.

The Financial Supervisory Service's strong loan regulation demands on secondary financial institutions stem from concerns about the balloon effect. From January to July this year, household loans in the secondary financial sector increased by 27.4 trillion won, contrasting with a decrease of 2.4 trillion won during the same period last year. This is analyzed as a consequence of commercial banks raising interest rates and reducing loan limits since the beginning of the year. In particular, the mutual finance sector saw a sharp increase of 12.4 trillion won.

Loan screening is also expected to become stricter. A secondary financial sector official explained, "To meet the household loan growth rate required by the financial authorities, it will be inevitable to strengthen screening and 'cut off' some borrowers." Methods such as reducing or eliminating preferential interest rates previously offered to prime customers are also being considered.

What to do when you urgently need money... Real borrowers sharing 'Youngkkeul-beop'

Under comprehensive loan regulations, real borrowers who need to secure housing funds immediately are seeking detours. Posts discussing and sharing Youngkkeul-beop methods are increasingly appearing in financial and office worker communities.

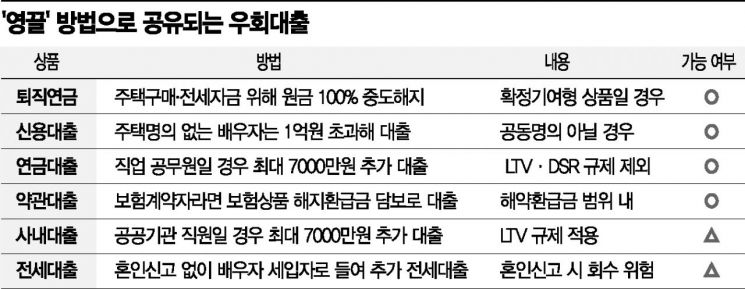

A representative method is securing funds through housing title and spouse's unsecured loans. Since the end of last year, if one receives an unsecured loan exceeding 100 million won and purchases a house in regulated areas such as Seoul within a year, the loan is recalled. However, a spouse who does not register the title can receive an unsecured loan exceeding 100 million won. The high-income spouse borrows over 100 million won, while the low-income spouse borrows within the 100 million won limit.

Early withdrawal from retirement pensions, a product guaranteeing citizens' old-age life, is also utilized. Generally, early withdrawal from retirement pensions is difficult, but defined contribution (DC) retirement pensions can be canceled if certain conditions are met. This applies when the subscriber is a non-homeowner and purchases a house under their name or bears the cost of a jeonse deposit or security deposit. According to the '2021 Housing Finance Research' published by the Korea Housing Finance Corporation, as of 2019, 72,830 people had already made early withdrawals totaling 2.7758 trillion won. Among early withdrawers, 52% cited housing purchase or residential lease as the reason for withdrawal.

In some cases, a method is secretly used to create a legal status of 'strangers' for a couple who are actually married. By not registering the marriage or divorcing, a spouse can be registered as a tenant. Legally, since they are not a married couple, the spouse can use a jeonse loan.

Insurance policyholders also sometimes use policy loans to cover the shortfall. A policy loan is a loan product where money is borrowed using the surrender value of an insurance product as collateral. Although it varies by insurance company and product, it is generally possible to borrow 50-95% of the surrender value.

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}

{kind=link}

{kind=link}