Household Loans in Secondary Financial Sector Increase by 27.4 Trillion KRW from Jan to Jul

Mutual Finance Sector Rises by 12 Trillion KRW, Steepest Growth

Financial Authorities "Limit Credit Loans Within Annual Salary in Secondary Finance"

Experts Warn "Beware of Another Balloon Effect"

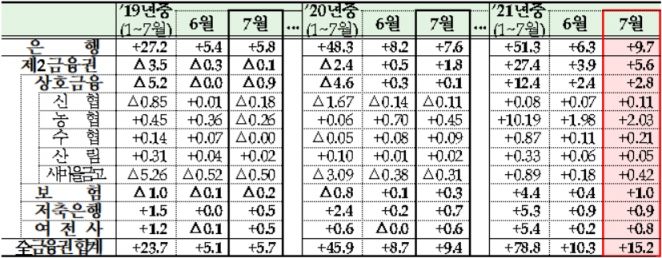

Trends in Household Loan Increase and Decrease in the Financial Sector (Based on Financial Supervisory Service Preliminary Data). Photo by Financial Services Commission.

Trends in Household Loan Increase and Decrease in the Financial Sector (Based on Financial Supervisory Service Preliminary Data). Photo by Financial Services Commission.

[Asia Economy Reporters Sunmi Park, Seungseop Song] "Appropriate levels of household loans will continue to be supplied steadily. We will carefully manage the process of facilitating a soft landing for household debt in the future to ensure that actual borrowers and the general public do not face difficulties."

Financial authorities made this statement to address concerns about a balloon effect caused by loan restrictions at commercial banks, but the market is already reacting as if the balloon effect has begun. Financial institutions that have reached the threshold for household loan growth targets continue to emerge, raising concerns that if commercial banks tighten loans further, it will lead to increased lending by other financial institutions, which in turn could trigger additional loan restrictions for those institutions that have reached their loan limit thresholds.

According to the financial industry on the 24th, due to interest rate hikes and loan limit reductions by commercial banks since the beginning of the year, household loans in the secondary financial sector increased by 27.4 trillion KRW from January to July this year. Considering that there was a decrease of 2.4 trillion KRW during the same period last year, this is a significant increase. In particular, the mutual finance sector saw the steepest growth with an increase of 12.4 trillion KRW. Credit card companies and savings banks also increased by 5.4 trillion KRW and 5.3 trillion KRW, respectively.

Although financial authorities are monitoring household loan growth rates on a weekly basis to manage them at a certain level, the pace of loan growth has already accelerated. Currently, commercial banks manage total household loans at 5-7%, while savings banks manage at 21%. For the savings bank sector, excluding policy financial products such as mid-interest loans and the Sunshine Loan, the household loan growth rate must be managed within 5.4%.

Secondary Financial Sector Also Regulated Like Commercial Banks... "Concerns Over Another Balloon Effect"

There are also management loopholes. Internet-only banks like KakaoBank, under the government's policy to strengthen inclusive finance, are tasked with expanding mid-interest and mid-to-low credit loans. As a result, their household loan growth rate exceeded 13% in the first half of the year, the highest in the industry, but management of this has inevitably been lax. An industry insider said, "The mid-interest loan portion is somewhat relaxed within the household loan growth target, while other credit loans or overdraft accounts are included in the total household loan management. Internet banks are still in a growth phase and are smaller in scale compared to commercial banks, so there is a tendency to give them some leeway."

Financial authorities plan to apply the same regulations to the secondary financial sector as to commercial banks to block the balloon effect, but there are significant concerns that this could cause side effects such as a loan cliff. Authorities have currently requested that the secondary financial sector also limit credit loan amounts to within annual income. Since this measure has been implemented for commercial banks, it aims to prevent borrowers seeking additional loans from moving to the secondary financial sector. However, many in the industry believe that this measure will not be impactful enough to prevent the balloon effect. Although savings banks can provide loans up to 1.2 to 1.8 times the borrower's annual income, cases where such amounts are actually granted are extremely rare.

Nonetheless, under pressure from financial authorities, savings banks appear to be considering their own household loan management measures. While none are considering unilateral suspension of loan products, typical measures include reducing loan limits or applying stricter cut-off criteria during screening. In such cases, financially vulnerable groups may be driven to loan companies or P2P platforms. This is why there are criticisms that policies implemented to prevent the balloon effect may actually create another balloon effect.

Professor Tae-yoon Sung of Yonsei University's Department of Economics advised, "Primary and secondary financial sectors should basically be regulated to a similar extent. Apart from the current measures, since there are concerns about a balloon effect causing illegal private loans to grow, financial authorities should consider countermeasures." He added, "At this stage, it seems necessary to adjust various conditions such as interest rates."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}