Managing Unregistered Companies Is Not Easy

User Deposit Ratio Also a Problem

[Asia Economy Reporter Kiho Sung] As the ‘Merge Point controversy’ grows, calls for the passage of amendments to the Electronic Financial Transactions Act (EFTA) to protect consumers are emerging. However, there are concerns that the proposed amendments alone may not be sufficient to prevent a ‘second Merge Point incident.’ The current bill pending in the National Assembly focuses on managing and supervising registered electronic financial service providers. Therefore, it is pointed out that it would still be difficult to manage unregistered providers even if the bill passes. Additionally, the ratio of user deposits held externally remains controversial, highlighting the need for more meticulous legislative review.

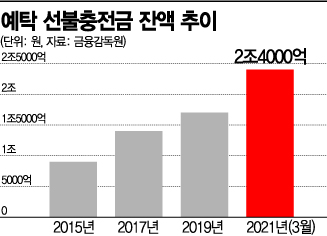

According to the Financial Supervisory Service as of the end of March this year, there are a total of 65 registered prepaid service providers, with the prepaid balances they issued reaching 2.4 trillion won. However, this figure only estimates registered companies. For unregistered providers, it is difficult to even ascertain details such as the amount issued and the number of companies. For this reason, some in the industry believe that amending the EFTA alone cannot be the solution. The amendment includes consumer protection measures such as requiring electronic financial service providers to separately store customers’ prepaid funds with external institutions, but there is no effective way to supervise ‘unregistered providers.’ In fact, Merge Plus, which operates Merge Point, conducted business for three years without registering as a ‘prepaid electronic payment instrument issuer and manager’ (prepaid provider) as stipulated under the current EFTA.

According to Article 49, Paragraph 5 of the current EFTA, unregistered operations can be punished with imprisonment of up to three years or a fine of up to 20 million won. However, this is only a penalty imposed by investigative authorities, and there are no administrative sanctions from financial regulators. A financial industry official pointed out, “Merge Point only gained attention recently because of the issue, but the problem is that it has been operating unregistered for three years already. Even if the EFTA is amended, it is practically impossible for financial authorities to monitor all the numerous companies, so cooperation with investigative authorities will likely be necessary to manage unregistered providers.”

Meanwhile, the ratio of user deposits stipulated in the EFTA amendment is also expected to come under scrutiny. Since prepaid funds entrusted by customers have the nature of deposits, they should be protected. However, the current EFTA does not require prepaid funds to be separately stored with external institutions. The amendment includes provisions to protect prepaid funds by segregating deposits from proprietary assets and entrusting them to external financial institutions such as banks. However, while fund transfer service providers are required to manage 100% of the deposits, payment settlement service providers are only required to deposit 50%.

Even if Merge Plus registers as a payment settlement service provider after the amendment, it would not need to deposit half of the prepaid funds. Therefore, if users simultaneously request refunds, a ‘second Merge Point incident’ could be repeated. This issue has been continuously pointed out even after the EFTA amendment was proposed. To prevent a ‘second Merge Point incident,’ there are calls not only to strengthen some consumer protection provisions in the EFTA amendment but also to relax the registration criteria for prepaid providers so that many telemarketing companies can be included under the supervision of financial authorities.

Jo Hyekyung, Senior Researcher at the Political Economy Research Institute Da-an, diagnosed, “Prepaid account customer deposits were excluded from the application of the Banking Act because they are not bank deposits. The EFTA amendment is further deepening the fragmented regulatory system concerning electronic payment services.”

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}