Out-of-Stock Marketing Surge... Beware of Incomplete Sales

[Asia Economy Reporter Oh Hyung-gil] "The 10% no-surrender refund type children's insurance products will disappear after August 13. If you are preparing to subscribe to a no-surrender product, you should sign up quickly."

Since mid-this month, sales of some no-surrender refund type products have been suspended, leading to aggressive clearance marketing. Consumers are advised to be cautious of incomplete sales tactics urging them to hurry and subscribe by claiming that premiums will increase after sales stop.

According to the insurance industry on the 2nd, the Financial Supervisory Service delivered guidelines last month to all insurers regarding compliance when developing no (low) surrender refund type products. The guidelines included a ban on selling 10% refund type products among refund products.

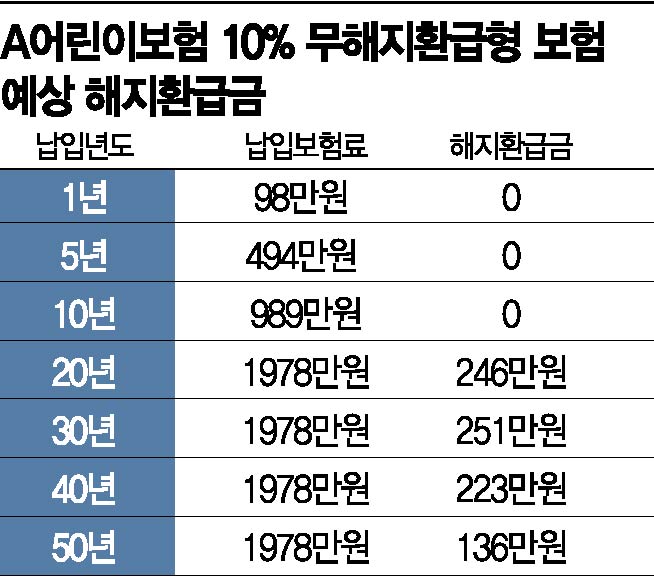

The no-surrender refund type is a product where no money (surrender refund) is returned if the contract is canceled during the premium payment period, but the premium is on average about 30% cheaper than the standard type. In particular, if the full payment period is completed, a refund is given, and since the refund rate is higher than the standard type, it can be mistaken for a savings-type insurance. Therefore, the financial authorities revised the insurance supervision regulations last November to prevent the refund rate from exceeding the standard type.

In response, insurers introduced 10% and 50% refund type products with significantly lowered refund rates after payment to reduce premiums. While there is no refund during the premium payment period, these products return 10% or 50% of the paid premiums after full payment in exchange for lower premiums.

The financial authorities view this method as potentially causing consumer damage since the refund amount is less than the paid premium and may impose financial burdens on insurers. Therefore, they have restricted sales of the 10% type. They have also announced product improvement measures for the 50% refund type products next month.

The no-surrender type is designed considering the lapse rate, which is how many customers cancel their insurance at a certain point after subscription. If more customers maintain their policies rather than lapse, the loss ratio increases, and the financial burden of preparing reserves for insurance payments also grows, potentially causing long-term problems.

The authorities also communicated that if sales of no-surrender type products surge during the remaining period, insurers must submit explanatory materials, establishing measures to prevent the use of clearance marketing. However, concerns arise as some corporate agencies (GA) are promoting sales to increase volume, which could lead to consumer harm.

An official from a non-life insurance company said, "We have warned GAs to prevent overheating of promotional activities ahead of the sales suspension, but some companies are trying to meet their targets," adding, "It is better to carefully consider whether the insurance is truly necessary before deciding to subscribe."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}