Strong Performance Driven by Price Increase and Sales Growth of Key Chemical Products Including PVC

Solar Power Faces Continued Losses Due to Rising Raw Material Prices and Soaring Logistics Costs

[Asia Economy Reporter Hwang Yoon-joo] Hanwha Solutions recorded an operating profit exceeding 200 billion KRW on a consolidated basis in the second quarter. While the chemical business drove the performance, the solar power business fell into a deficit for the third consecutive quarter due to rising prices of raw and subsidiary materials and increased logistics costs.

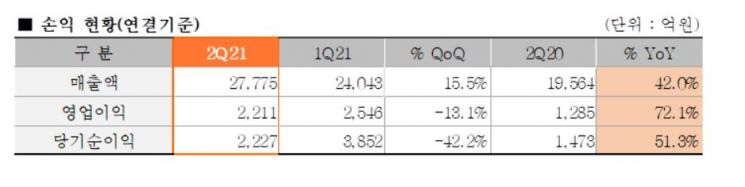

Hanwha Solutions announced on the 29th that its consolidated operating profit for the second quarter of this year was 221.134 billion KRW, a 71.09% increase compared to the same period last year. During the same period, sales rose 41.97% year-on-year to 2.7774 trillion KRW, and net profit jumped 51.26% to 222.78 billion KRW, according to preliminary estimates. Accordingly, the operating profit for the first half of the year was 475.71 billion KRW, up 60.90%, and sales increased 23.24% to 5.1817 trillion KRW.

By business segment, the Chemical division recorded sales of 1.3331 trillion KRW, up 70.7% year-on-year, and operating profit of 293 billion KRW, a 215.7% increase. This was due to the continued effect of using low-cost raw materials and increased demand for industrial materials amid domestic and international economic recovery, which kept prices of key products such as PVC (polyvinyl chloride) and caustic soda strong.

The Q CELLS division posted sales of 1.0065 trillion KRW, a 35.5% increase compared to the same period last year, but recorded an operating loss of 64.6 billion KRW. Although it earned 22 billion KRW in operating profit through the sale of renewable energy power generation assets, the solar module sales business failed to achieve profitability due to worsening external factors such as soaring prices of major raw and subsidiary materials (wafers, silver, aluminum) and logistics costs. In fact, the international price of polysilicon, a key raw material for solar cells, surged from around 7 USD per kg in June last year to about 28 USD per kg within a year, and international maritime freight rates also increased about fourfold during the same period.

The Advanced Materials division recorded sales of 224.3 billion KRW and an operating profit of 2.2 billion KRW. The Galleria division saw sales increase 15.3% year-on-year to 126.6 billion KRW, turning operating profit positive at 2.2 billion KRW.

Regarding the second half performance, Hanwha Solutions expects overall results to be not bad due to continued global economic recovery despite the reversal of the oil price uptrend.

Shin Yong-in, CFO and Vice President, said, "The solar power business is expected to face difficulties as the strong prices of raw and subsidiary materials are likely to continue for the time being," but added, "Since the renewable energy power generation business, which we are nurturing as a strategic business to become an 'energy solution provider,' has started to show results, we will do our best to improve performance in the second half."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

![Clutching a Stolen Dior Bag, Saying "I Hate Being Poor but Real"... The Grotesque Con of a "Human Knockoff" [Slate]](https://cwcontent.asiae.co.kr/asiaresize/183/2026021902243444107_1771435474.jpg)

{kind=link}